Virtualization Security Market Summary

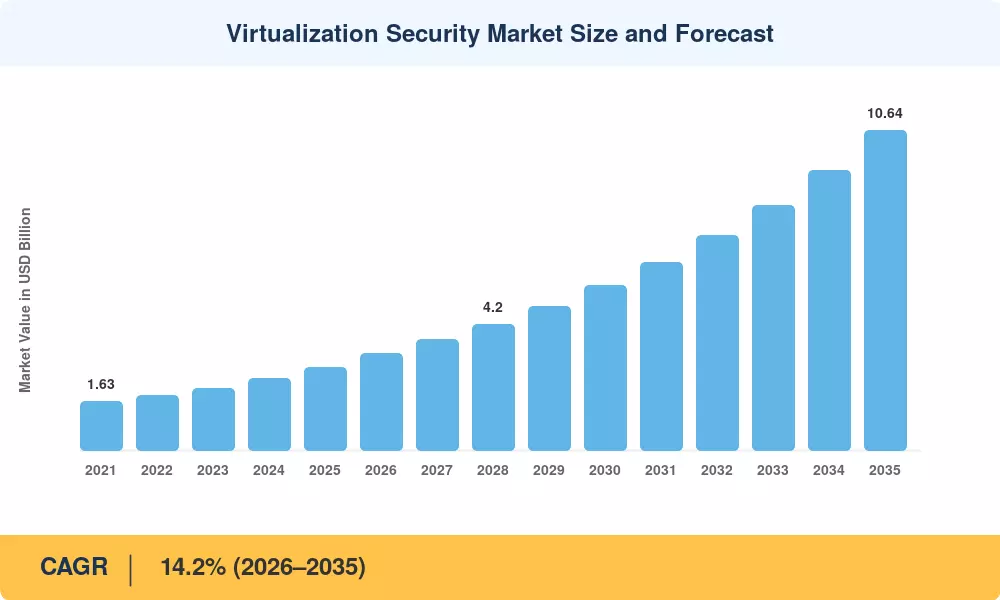

The Virtualization Security Market reached a valuation of USD 2.76 billion in 2025 and is projected to expand from USD 3.22 billion in 2026 to USD 10.64 billion by 2035, registering a CAGR of 14.2% across the forecast period. Accelerating hybrid cloud adoption — driven by enterprise mandates to reduce on-premise capital expenditure by 20–30% over three years — and tightening data-sovereignty regulations across the EU, India, and Brazil are two primary catalysts sustaining double-digit growth [1][2]. Broadcom's USD 69 billion acquisition and subsequent integration of VMware into a subscription-first private-cloud platform underscores how platform consolidation is reshaping both competitive dynamics and buyer expectations in this space [3].

A deeper structural shift is underway as legacy perimeter-based firewalls give way to hypervisor-embedded micro-segmentation, workload-level encryption, and AI-powered anomaly detection. The U.S. Cybersecurity and Infrastructure Security Agency (CISA) published binding directives in 2024 requiring federal agencies to implement zero-trust architectures across all virtualized workloads by FY 2027 — a mandate expected to mobilize over USD 1.8 billion in federal procurement spending [4]. Enterprises outside government are following suit, with estimating that 60% of organizations will have adopted at least one form of embedded hypervisor security by 2028 [5].

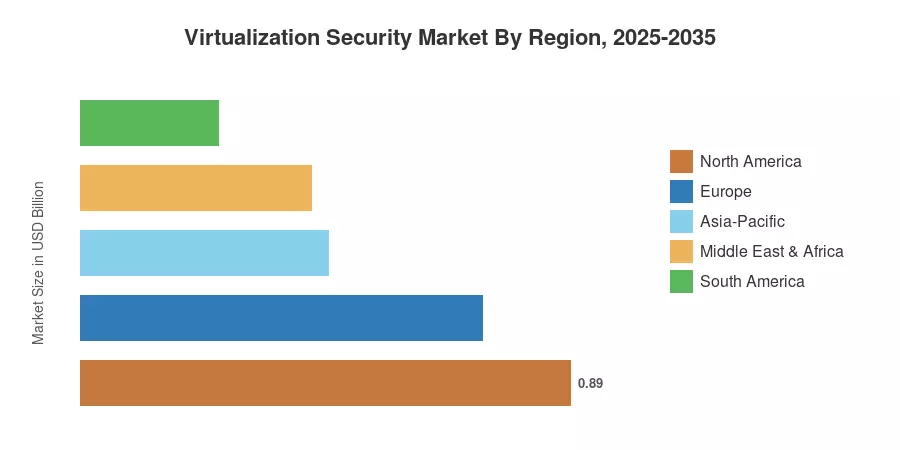

North America commands approximately 32.1% of the Virtualization Security Market, anchored by the high density of hyperscale data-center operators and federally mandated zero-trust frameworks. Asia-Pacific is the fastest-growing region at a 16.4% CAGR, propelled by digital-infrastructure investments from India's Digital India initiative and China's "East Data West Computing" program [6]. Europe holds the second-largest share at roughly 26.5%, where NIS2 Directive compliance is compelling financial-services and healthcare organizations to upgrade virtualized infrastructure controls. The market's trajectory through 2035 will increasingly depend on the convergence of confidential computing, AI-driven threat detection, and sovereign-cloud mandates.

Key Report Takeaways

• By Component

- Solutions captured 58.5% of the Virtualization Security Market in 2025, reflecting enterprise preference for integrated platform suites over piecemeal tools.

- The Services segment is expected to grow at a 17.3% CAGR through 2035, driven by rising demand for managed detection and response engagements.

• By Virtualization Layer

- Hardware/Server Virtualization accounted for 42.2% of the Virtualization Security Market in 2025.

- Network and SD-WAN Virtualization is advancing at a 16.6% CAGR, fueled by enterprise SD-WAN rollouts.

• By Deployment Mode

- Public Cloud held a 30.6% share in 2025 as organizations maintained multi-cloud strategies.

- Hybrid Cloud shows the fastest growth at a 16.1% CAGR through 2035, supported by data-residency regulations.

• By End-User Industry

- IT and Telecom commanded a 25.2% revenue share of the Virtualization Security Market in 2025.

- Healthcare and Life Sciences are expanding at a 15.6% CAGR, reflecting the sector's growing attack surface from connected medical devices.

• By Organization Size

- Large Enterprises represented 60.3% of the Virtualization Security Market in 2025.

- SMEs are the fastest-growing segment at a 16.9% CAGR, aided by affordable cloud-delivered security offerings.

• By Region

- North America maintained a 32.1% share in 2025, led by U.S. federal and hyperscale demand.

- Asia-Pacific is the fastest-growing region at a 16.4% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's estimation framework combines primary interviews with over 120 CISOs and procurement leads, vendor financial disclosures, and secondary validation against government IT spending databases. Historical values (2021–2024) rely on audited revenue from publicly traded vendors and cross-checked / tracker data, while forecast values (2026–2035) incorporate regression models calibrated to enterprise IT capital-expenditure cycles and regulatory compliance timelines [7].