Wine Market Summary

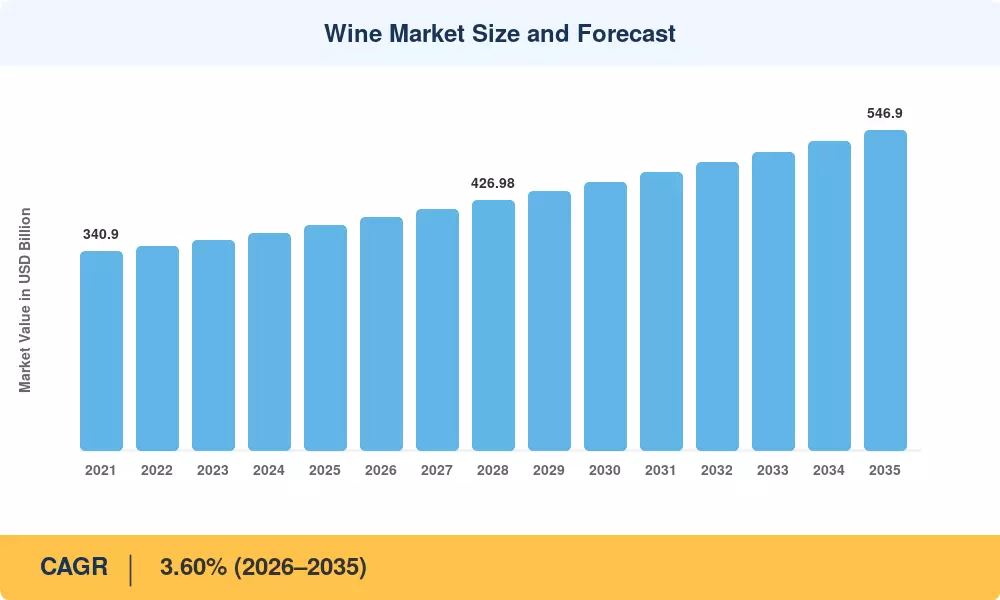

The global Wine Market reached an estimated USD 384.00 billion in 2025 and is projected to grow from USD 397.80 billion in 2026 to USD 546.90 billion by 2035, registering a CAGR of 3.60% during the forecast period. This trajectory reflects a clear shift in how consumers engage with wine — value growth now outpaces volume growth as buyers gravitate toward premium labels, estate-bottled selections, and region-specific appellations. Policy support from the European Commission's Common Agricultural Policy, which allocated over EUR 1.1 billion annually to vineyard restructuring and promotion programs through 2027, continues to anchor production quality across legacy wine production regions [1].

A quiet transformation is reshaping the Wine Market from the vineyard floor to the retail shelf. Legacy distribution networks built around brick-and-mortar retail are giving way to direct-to-consumer (DTC) e-commerce platforms and subscription models. The USDA estimates that online wine sales across major consuming nations surpassed USD 28 billion in 2024, roughly double pre-pandemic levels [5]. Precision viticulture — leveraging drone imagery, IoT soil sensors, and AI-driven harvest timing — now influences roughly 18% of global hectarage under vine, reducing yield volatility and labor costs [13].

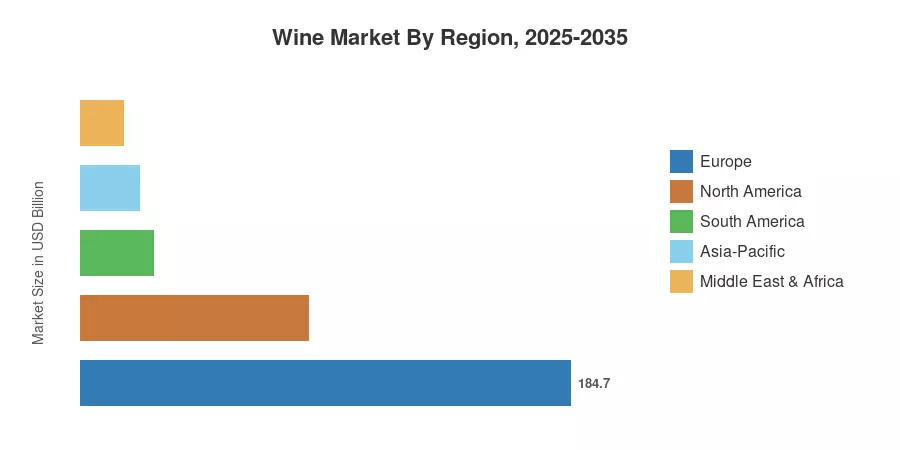

Europe commands roughly 48.1% of the Wine Market by value, anchored by France, Italy, and Spain — three nations that together account for nearly half of global production volume [3]. Asia-Pacific is the fastest-growing region, advancing at a 5.8% CAGR as urbanization and rising disposable incomes in China and India reshape consumption habits. North America holds the second-largest share, driven by the United States' position as the world's top wine-consuming country by value. The decade ahead will hinge on how producers balance premiumization ambitions against climate-induced supply constraints and shifting generational preferences.

Key Report Takeaways

• By Product Type

- Still wine accounted for 76.2% of the total Wine Market value in 2025, sustained by everyday table wine consumption and growing interest in single-vineyard bottlings.

- Sparkling wine is projected to expand at a 4.3% CAGR through 2035, fueled by year-round consumption patterns beyond traditional celebrations.

• By Color

- Red wine captured 51.6% of the Wine Market in 2025, supported by strong demand in Southern Europe and established New World appellations.

- Rosé wine is forecast to grow at a 4.4% CAGR, reflecting lifestyle-driven demand among younger demographics.

• By Region

- Europe held a 48.1% share of the Wine Market in 2025, leveraging protected designations of origin and centuries-old production infrastructure.

- Asia-Pacific is set to register the fastest growth through 2035 at a 5.8% CAGR, with China, India, and ASEAN markets leading adoption.

Market Size and Forecast (2021–2035)

Market Research Future derives historical Wine Market estimates from customs trade data, producer revenue filings, and OIV harvest statistics. Forecast projections integrate proprietary demand modeling with macroeconomic overlays, adjusting for population growth, disposable income trends, and excise-tax trajectories across 45 key consuming nations [1][2].

.webp?v=1783938003)