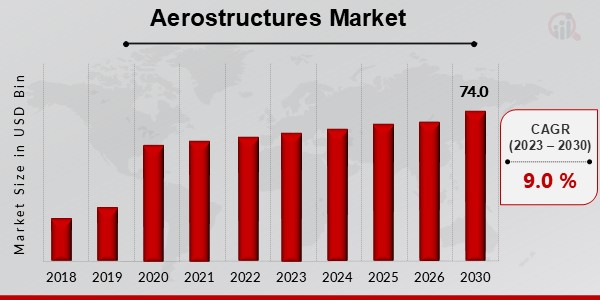

What is the projected market valuation of the Aerostructures Market by 2035?

The Aerostructures Market is projected to reach a valuation of 4500.0 USD Million by 2035.

What was the market valuation of the Aerostructures Market in 2024?

In 2024, the Aerostructures Market was valued at 1900.0 USD Million.

What is the expected CAGR for the Aerostructures Market during the forecast period 2025 - 2035?

The expected CAGR for the Aerostructures Market during the forecast period 2025 - 2035 is 8.45%.

Which companies are considered key players in the Aerostructures Market?

Key players in the Aerostructures Market include Boeing, Airbus, Lockheed Martin, Northrop Grumman, Raytheon Technologies, Safran, Leonardo, Thales, and Mitsubishi Heavy Industries.

What are the main segments of the Aerostructures Market by application?

The main segments by application include Commercial Aviation, Military Aviation, Space Exploration, Unmanned Aerial Vehicles, and Helicopters.

What is the valuation range for the Commercial Aviation segment in the Aerostructures Market?

The valuation range for the Commercial Aviation segment is between 800.0 and 2000.0 USD Million.

How does the valuation of Composite Materials compare to Aluminum in the Aerostructures Market?

Composite Materials have a valuation range of 700.0 to 1800.0 USD Million, whereas Aluminum ranges from 600.0 to 1400.0 USD Million.

What manufacturing processes are included in the Aerostructures Market segments?

Manufacturing processes include Additive Manufacturing, Subtractive Manufacturing, Forming, Machining, and Assembly.

What is the projected valuation for the Machining segment by 2035?

The projected valuation for the Machining segment is expected to be between 570.0 and 1350.0 USD Million by 2035.

Which end-use segments are included in the Aerostructures Market?

End-use segments include Airframes, Wings, Fuselages, Empennages, and Control Surfaces.