クラウドコンピューティング市場 概要

MRFR分析によると、クラウドコンピューティング市場規模は2024年に7兆91兆1,740億米ドルと推定されています。クラウドコンピューティング市場産業は、2025年の9兆28兆8,645億米ドルから2035年までに49兆55兆9,816億米ドルに成長すると予測されており、予測期間中は18.2%の年平均成長率(CAGR)を示しています。期間 (2025 ~ 2035 年)。

主要な市場動向とハイライト

クラウド コンピューティング市場は、技術革新、消費者の健康の優先事項、個別化されたウェルネスの需要によって推進される変革的な変化を目の当たりにしています。

- 現在、人工知能はクラウドにおける最も明らかな成長促進剤です。 AI および生成 AI ワークロードには、はるかに多くのコンピューティング、ストレージ、ネットワーキングが必要です。

- 多くの企業にとって、ハイブリッド クラウドはもはや移行段階ではありません。これはますます好まれる運用モデルとなっています。組織は、機密性の高いワークロードをオンプレミスまたはプライベート環境に保持したいと考えています。

- 企業はロックインを軽減し、回復力を向上させ、より有利な商業条件を交渉したいと考えているため、マルチクラウドの導入は増え続けています。

- クラウド支出の増加により、コストの最適化が取締役会レベルの課題となっています。企業はもはやクラウドを単なるエンジニアリング費用として扱っていません。彼らはユニットエコノミクス、ワークロード効率、クラウド投資収益率を積極的に測定しています。

市場規模と予測

| 2024年の市場規模 | 7,91,174.00 (USD Billion) |

| 2035年の市場規模 | 49,55,981.67 (USD Billion) |

| CAGR (2025 - 2035) | 18.2% |

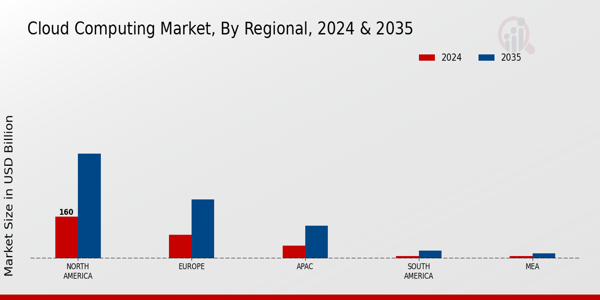

| 2024 年に最大の地域市場シェアを獲得 | 北米 |

主要なプレーヤー

主要選手などアマゾン ウェブ サービス(AWS)、Microsoft Azure、Google Cloud Platform(GCP)、VMware(Broadcom)、Oracle Cloud、Rackspace Technology、Digital Ocean、Salesforce Cloud、Tencent Cloud、Alibaba Cloud、IBM Cloud、SAP SE、ServiceNow は、統合された AI 機能を備えたクラウド エコシステムを進化させています。これらの企業は、自動化、機械学習、インテリジェントなリソース管理をクラウド プラットフォームに組み込んでいます。市場は、自己最適化と AI 主導のインフラストラクチャに移行しています。この進化により企業規模のデジタル変革が加速します

.webp?v=1784719986)