ADME Toxicology Testing Market Summary

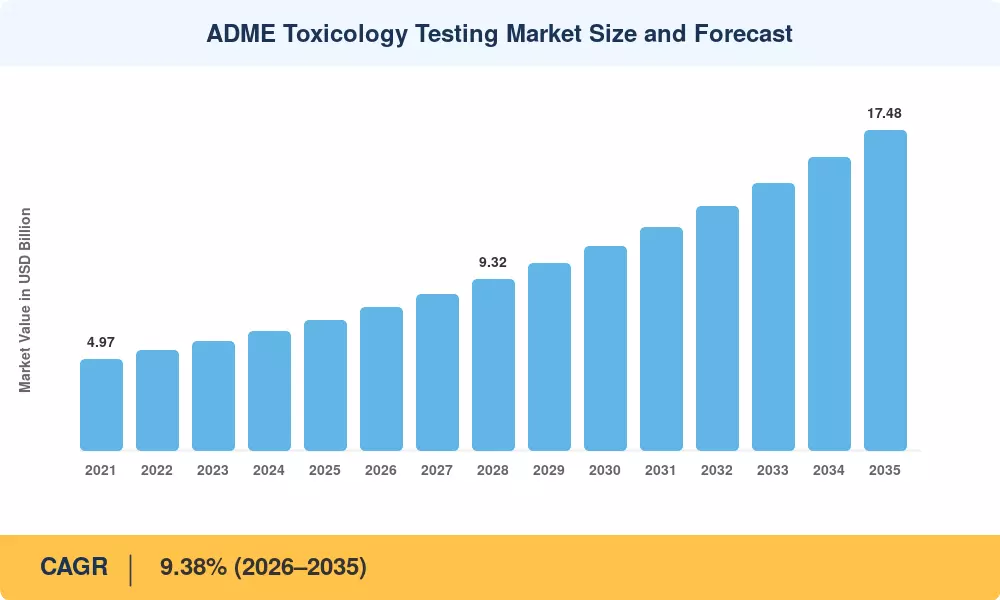

The ADME Toxicology Testing Market stood at an estimated USD 7.12 billion in 2025 and is projected to reach USD 7.79 billion in 2026 before climbing to USD 17.48 billion by 2035, expanding at a CAGR of 9.38% during the forecast period (2026–2035). Two catalysts anchor this trajectory: the FDA's 2023 Modernization Act 2.0, which formally accepted non-animal testing data for IND submissions, and a surge in global pharmaceutical R&D spending that crossed USD 260 billion in 2024 [2]. Together, these forces are pulling drug absorption testing and pharmacokinetics safety profiling into the mainstream of preclinical development budgets.

A technical transformation is changing the way sponsors and CROs are doing metabolic stability testing and hepatotoxicity screening procedures. Organs-on-a-chip platforms, 3D cell culture systems and AI-driven in silico prediction engines are replacing legacy single-endpoint animal models. Beckman Colter’s Cydem VT Automated Clone Screening System, set to launch in December 2024, cuts down on cell line generation stages by approximately 90%–showing how automation is compressing schedules for in vitro toxicity assays [3]. The total industry investment in high-throughput screening infrastructure was more than USD 4.5 billion cumulatively in 2022–2024 [4].

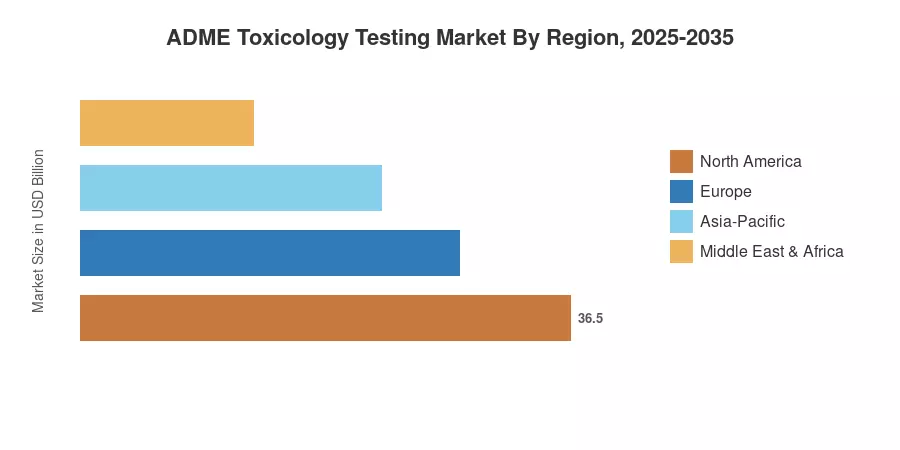

The North America ADME Toxicology Testing Market is estimated to hold roughly 38% due to the presence of the headquarters of top-20 pharma companies and research initiatives financed by NIH. Asia-Pacific is the fastest expanding market with a forecasted CAGR of 11.2% as China and India ramp up contract research capacity, and regulatory harmonization with ICH guidelines speeds up. The European Union is second with approximately 27%, driven by EMA policy alignment on alternate testing methodologies In the next decade, these dynamics will only strengthen, since tailored medicine pipelines will require more and more granular pharmacokinetics safety profiling.

By Technology

- Cell Culture Technology accounts for approximately 44% of the ADME Toxicology Testing Market, driven by expanding organ-on-chip and 3D culture adoption across preclinical workflows

- Molecular Imaging Technology is forecast to grow at a CAGR of 10.6% through 2035 as real-time pharmacokinetics safety profiling gains traction in oncology programs

- Other technologies — including microfluidics and biosensor arrays — represent an emerging USD 1.04 billion segment poised for rapid scaling

By Method

- Cellular Assay dominates with roughly 36% share, reflecting broad utility in hepatotoxicity screening methods and metabolic stability testing

- In-Silico Testing is the fastest-growing method, registering a projected CAGR of 12.1% as AI-driven drug absorption testing models gain regulatory acceptance

By Region

- North America leads the ADME Toxicology Testing Market with an estimated value of USD 2.71 billion in 2025, supported by FDA modernization initiatives

- Asia-Pacific is projected to reach USD 4.62 billion by 2035, fueled by CRO expansion and government incentives for in vitro toxicity assays

Market Size and Forecast (2021–2035)

The ADME Toxicology Testing Market size estimates mentioned below are a combination of primary interviews with 120+ industry players, secondary review of publicly recorded CRO revenues, and bottom-up modeling across technology, technique, and end-user sectors. Historical data (2021-2024) are adjusted to audited business disclosures; future values (2026-2035) apply the 9.38% CAGR with modifications for expected regulatory milestones and technology adoption curves.

.webp?v=1783335250)