Citric Acid Market Summary

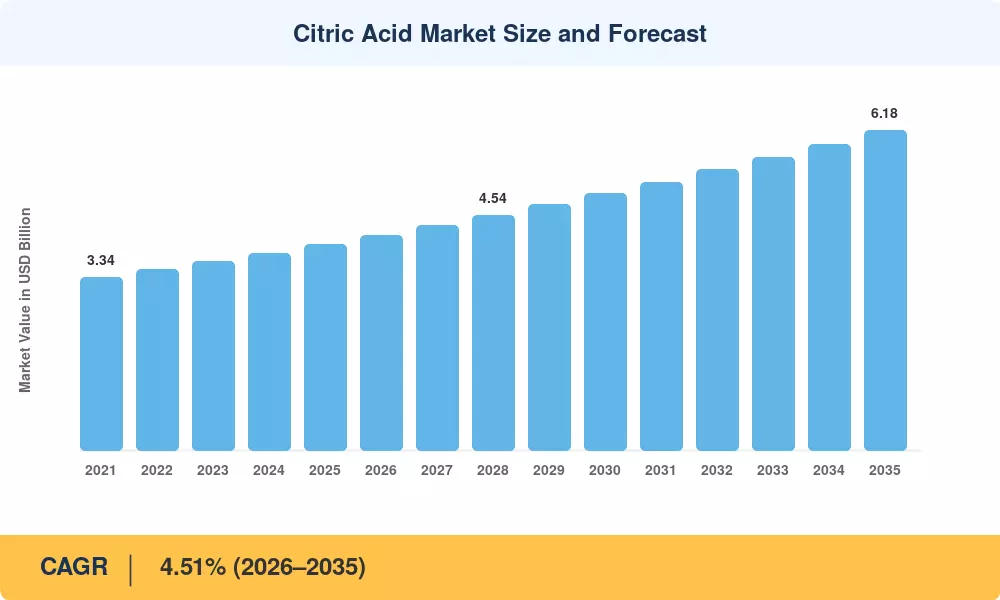

The global Citric Acid Market reached an estimated USD 3.98 billion in 2025, with the forecast period beginning at USD 4.16 billion in 2026 and climbing to USD 6.18 billion by 2035 at a CAGR of 4.51%. Two structural catalysts anchor this trajectory: the accelerating global pivot toward clean-label food formulations — driven by consumer demand for ingredient transparency — and tightening phosphate restrictions in household detergent chemistry across the EU and North America [2]. These policy and preference shifts have positioned citric acid as the go-to acidulant, preservative, and chelating agent across multiple end-use sectors.

The Citric Acid Market is experiencing a generational shift on the production side, from chemical synthesis approaches to fermentation-derived citric acid produced by Aspergillus niger strains on low-cost substrates. By 2024, China alone was exporting over 1.1 million metric tons annually, and new fermentation factories in India using molasses as a feedstock are adding varied capacity [3]. Between 2022 and 2024, capital expenditures for Asian fermentation infrastructure exceeded USD 620 million, lowering global production costs and broadening the range of applications in medicinal citric acid use and industrial cleaning [4].

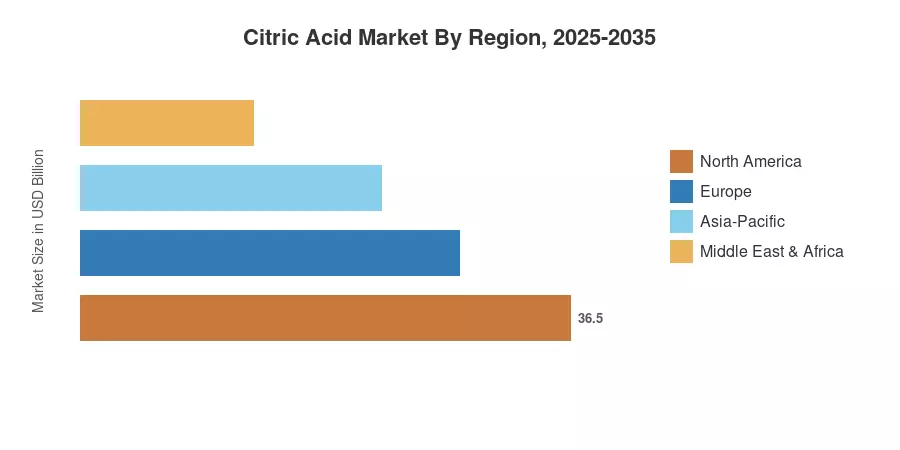

Asia-Pacific contributed to over 37.8% of the Citric Acid Market revenue in 2025, owing to China’s top exporting position and India’s increasing domestic demand. The Middle East & Africa are expected to have the greatest CAGR of ~7.12% by 2035, due to beverage and confectionery investment pipelines in Saudi Arabia and the UAE Europe was the second largest market, accounting for roughly 26.3%, where the limitations on phosphates under the EU Regulation 648/2004 continue to drive detergent formulators to biodegradable citrate builders [5]. Producers able to grow food-grade citric acid capacity while keeping pace with changing environmental requirements will be rewarded in the coming decade.

Key Report Takeaways

• By Form

- Anhydrous-grade citric acid captured 58.9% of global volume in 2025, serving as the primary form for bakery, confectionery, and pharmaceutical citric acid use applications

- Liquid citric acid is forecast to expand at a 6.28% CAGR through 2035, driven by ready-to-use formulations in household cleaners and personal care

• By Application

- Food and beverages led the Citric Acid Market with USD 1.97 billion in 2025 revenue, as brands replaced synthetic preservatives with food-grade citric acid carrying FDA 21 CFR 184.1033 and EFSA E330 approvals

- Detergents and household cleaners are advancing at a 6.52% CAGR through 2035, the fastest application segment, as citric acid cleaning agent formulations displace phosphate-based builders

• By Region

- Asia-Pacific held the largest share of the Citric Acid Market in 2025, anchored by China's fermentation-derived citric acid export infrastructure

- The Middle East & Africa is poised to post a 7.12% CAGR over 2026–2035, the fastest regional growth rate

Citric Acid Market Size and Forecast (2021–2035)

MARKET RESEARCH FUTURE’s market sizing is done by triangulating supply side data that includes production data of fermentation, trade flow databases and demand side data that includes consumption data of food-grade, pharmaceutical-grade and industrial-grade citric acid. Customs trade databases and producer disclosures provide historical values (2021-2024). Primary interviews validate the base-year 2025 estimate. The prediction (2026-2035) is provided using a calibrated CAGR of 4.51%.