Direct Carrier Billing Market Summary

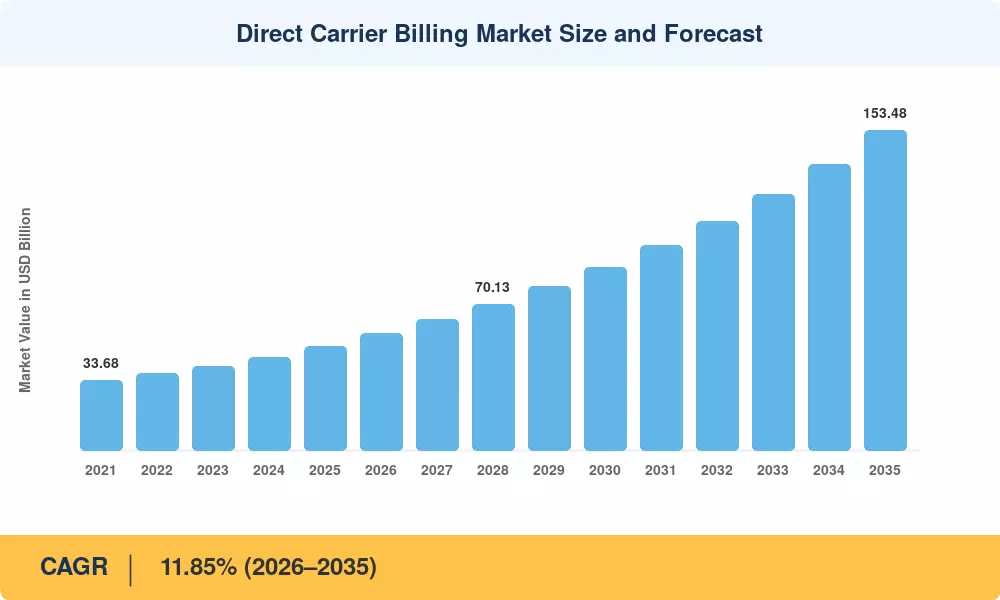

The Direct Carrier Billing Market reached a valuation of USD 50.12 Billion in 2025, entering its forecast phase at USD 56.06 Billion in 2026 and projecting toward USD 153.48 Billion by 2035, registering a CAGR of 11.85% across the 2026–2035 window. Two catalysts are accelerating this trajectory: the regulatory push toward open payment frameworks in Europe and Southeast Asia, and the explosion of micro-transaction monetization across gaming and streaming platforms. Operators and content publishers are moving aggressively to capitalize on a checkout flow that bypasses traditional banking rails entirely [1].

A structural shift is underway in how digital content gets monetized. Legacy credit-card-dependent checkout funnels — historically plagued by cart abandonment rates above 65% for mobile purchases — are giving ground to billing integrations embedded directly into the operator stack. Global mobile operator investment in billing APIs exceeded USD 4.8 Billion in 2024, a signal that the infrastructure layer is maturing fast enough to support enterprise-grade throughput. Regulatory mandates such as the EU's PSD3 framework and India's TRAI billing transparency rules are tightening compliance standards while simultaneously legitimizing the channel for higher-value transactions.

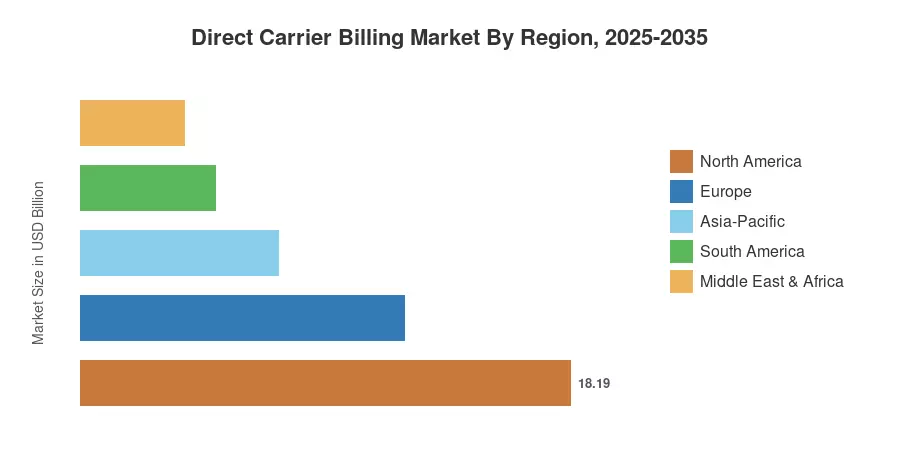

North America commanded a 36.30% share of the Direct Carrier Billing Market in 2025, anchored by high smartphone penetration and deep integration with app-store ecosystems. Asia-Pacific emerged as the fastest-growing region at a 14.68% CAGR, driven by unbanked population density and aggressive operator partnerships. Europe held the second-largest share at roughly 24.00%, supported by harmonized digital-payment regulations and mature OTT ecosystems. As 5G densification and connected-device proliferation accelerate through the decade, the Direct Carrier Billing Market is positioned to absorb payment volumes that traditional rails cannot efficiently serve.

Key Report Takeaways

• By Content Type

- Gaming captured 44.20% of Direct Carrier Billing Market revenue in 2025, reflecting strong micro-transaction volumes across mobile and cloud-based titles.

- Cloud & utility software is advancing at a 14.20% CAGR through 2035, fueled by SaaS subscription bundling with operator plans.

• By Device Platform

- Android smartphones accounted for 76.10% of the Direct Carrier Billing Market share in 2025, benefiting from Google Play's native billing integrations.

- Connected TVs are growing at a 13.10% CAGR, opening new premium-content billing channels beyond the handset.

• By Payment Flow

- One-off transactions represented 55.10% of the Direct Carrier Billing Market in 2025, driven by impulse digital-content purchases.

- Subscription-based billing is expanding at a 13.75% CAGR as recurring OTT and cloud bundles gain traction.

• By Operator Type

- Mobile network operators held an 87.85% share in 2025, leveraging their subscriber bases for seamless charge-to-bill flows.

- MVNOs are posting a 14.05% CAGR, attracted by white-label billing platforms that lower integration barriers.

• By End-User Segment

- Unbanked and under-banked consumers constituted 52.80% of Direct Carrier Billing Market usage in 2025.

• By Region

- North America led with 36.30% of global share in 2025.

- Asia-Pacific is the fastest-growing region at a 14.68% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on operator billing disclosures, app-store transaction data, regulatory filings, and proprietary primary research across 32 countries. Historical figures (2021–2024) reflect audited carrier revenue splits; forecast values (2026–2035) apply an 11.85% compound annual growth rate anchored to the 2025 base year.