Electric Car Rental Market Summary

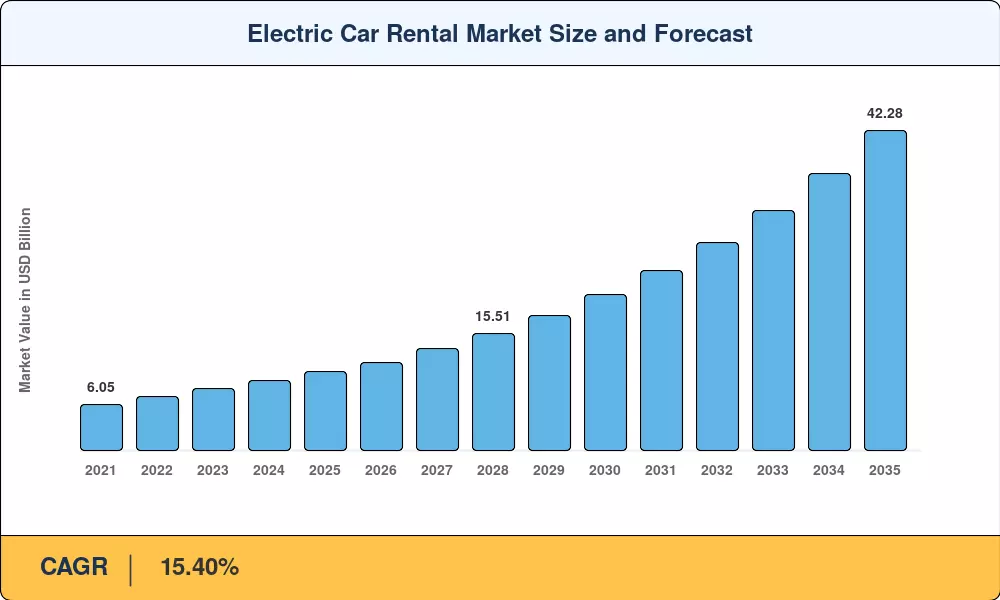

The Electric Car Rental Market was valued at USD 10.40 billion in 2025 and is projected to reach USD 11.65 billion in 2026 before climbing to USD 42.28 billion by 2035, registering a compound annual growth rate of 15.40% during the 2026–2035 forecast window. This trajectory is anchored by accelerating government mandates — the European Union's CO₂ fleet emission standards, California's Advanced Clean Fleets regulation, and China's dual-credit NEV policy — that collectively push rental operators toward battery-electric procurement at scale [1][2]. Corporate travel managers now specify zero-emission vehicle options in managed-travel RFPs, creating contractual demand that legacy operators cannot ignore.

A fundamental shift in the economics of the vehicle life cycle is driving this revolution. Automakers, including Tesla, Hyundai and Stellantis, are offering rental firms residual-value guarantees and buy-back schemes, lowering the depreciation risk that has historically prevented high-volume electric purchases [3]. By 2027, global sales of passenger EVs are expected to top 20 million units a year, and rental operators are positioning themselves to take a rising slice of that manufacturing pipeline [4]. Peer-to-peer platforms have also disrupted the value chain, allowing private EV owners to monetize their idle vehicles and increasing pricing competition for existing providers.

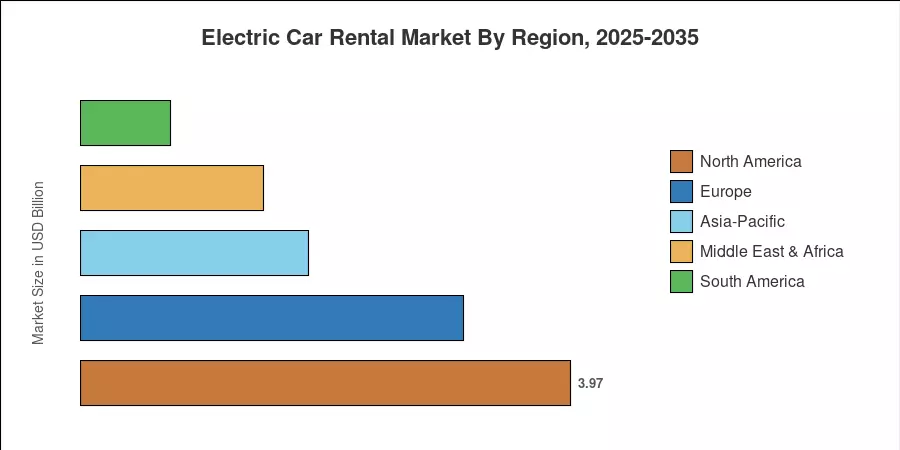

North America holds the highest regional share of 38.2% in the Electric Car Rental Market. This is due to the bulk Tesla purchase by Hertz and the growing EV fleet by Enterprise across 40+ airports in the U.S. [5]. The Asia-Pacific area is experiencing the highest growth, with a projected CAGR of 17.80%. This is attributed to China’s dominance in EV manufacturing and India’s FAME III subsidy scheme. Europe holds the second-highest stake with close to 29.8%, and Europcar and Sixt promise to electrify 50% of their fleets by 2030 [6]. How fast the charging infrastructure can scale to meet fleet deployment objectives will determine the next decade.

Key Report Takeaways

• By Vehicle Type

- Battery-electric models held a 69.8% share of the Electric Car Rental Market in 2025, reflecting automaker incentive programs and total-cost-of-ownership advantages over plug-in hybrids.

• By Customer Type

- Leisure and tourism clients accounted for 54.4% of rentals in 2025, with destination tourism boards partnering with rental firms to promote green mobility packages.

- Ride-hailing driver subscriptions are forecast to grow at a significant CAGR between 2026 and 2031.

• By Geography

- North America generated approximately USD 3.97 billion in Electric Car Rental Market revenue during 2025, with the United States accounting for over 72% of that total

- Asia-Pacific is forecast to grow at a 17.80% CAGR, with China's ride-hailing electrification mandates pulling commercial subscriptions into the rental ecosystem

Market Size and Forecast (2021–2035)

Historical estimates are obtained by Market Research Future (MRFR) using a triangulation of car registration databases, operator financial disclosures and third-party mobility analytics platforms. Forecast projections include published fleet electrification pledges, charging infrastructure implementation roadmaps and macroeconomic travel-demand models calibrated against IATA and UNWTO passenger forecasts [7][8].