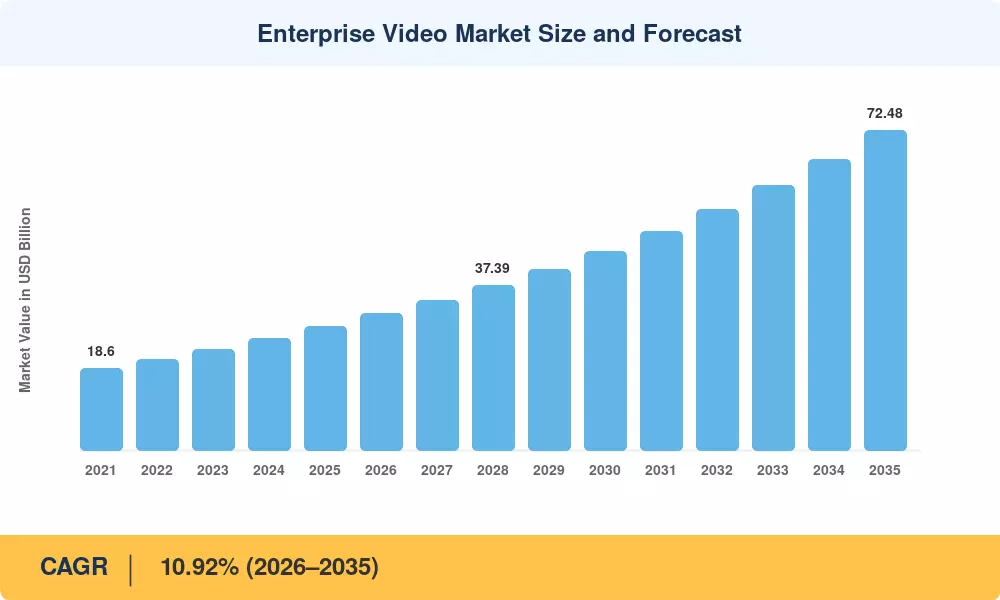

Enterprise Video Market Summary

The Enterprise Video Market reached USD 28.15 billion in 2025 and is projected to grow from USD 31.02 billion in 2026 to USD 72.48 billion by 2035, registering a CAGR of 10.92% during the forecast period (2026–2035). This expansion is fueled by accelerating hybrid-work mandates across Fortune 500 companies and government digital-workplace directives such as the U.S. Federal Workplace Modernization Act, which earmarked USD 2.3 billion for secure enterprise video communication platforms and collaboration infrastructure through 2028. Enterprise video has evolved from a simple meeting tool into mission-critical infrastructure supporting AI-powered video search and transcription, compliance recording, and asynchronous knowledge sharing.

Legacy on-premises video hardware is being replaced by cloud-native, API-first platforms that embed video analytics for enterprise meetings directly into workflow automation layers. Cisco's USD 1.7 billion annual investment in Webex AI capabilities exemplifies the vendor arms race underway, while private 5G rollouts are enabling sub-25 ms latency for internal video streaming for corporate training across manufacturing floors and hospital campuses [1]. The Enterprise Video Market is also being reshaped by vendor consolidation — the Brightcove acquisition signals a platform race toward full-stack enterprise video content management solutions.

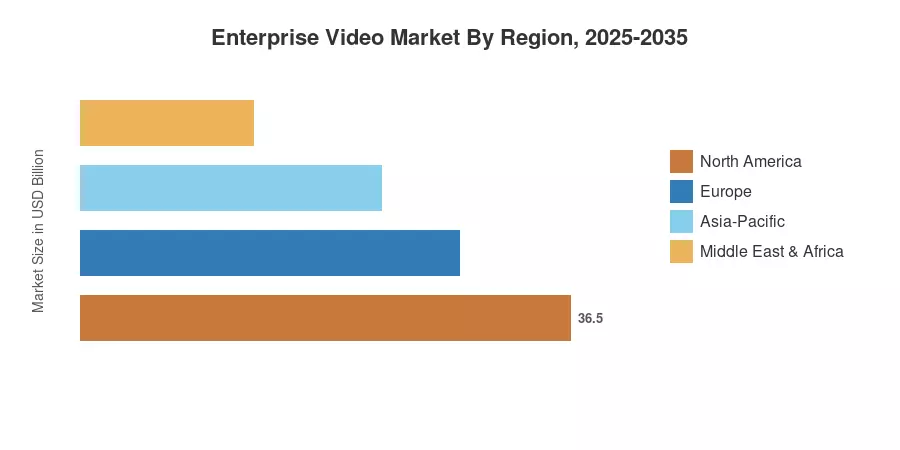

North America commands roughly 36.4% of the Enterprise Video Market, anchored by hyperscaler cloud investments and mature SaaS adoption. Asia-Pacific is the fastest-growing region at a 13.5% CAGR, propelled by India's Digital India programme and China's enterprise digitalization push. Europe holds the second-largest share at approximately 27.1%, driven by GDPR-compliant video archiving requirements and the EU's Digital Decade targets [3]. By 2035, the Enterprise Video Market will be shaped as much by AI governance frameworks as by bandwidth economics.

Key Report Takeaways

• By Type

- Video Conferencing accounted for 44.2% of Enterprise Video Market share in 2025, reflecting entrenched adoption across hybrid workplaces

- Video Analytics is set to register a 19.5% CAGR through 2035, driven by demand for AI-powered video search and transcription in compliance-heavy sectors

- Enterprise video content management solutions in the Webcasting and Live Streaming segment are projected to reach USD 9.8 billion by 2035

• By Component

- Software represented 54.3% of the Enterprise Video Market size in 2025, as organizations prioritize platform licensing over hardware refresh cycles

- Services is advancing at a 15.1% CAGR, reflecting growing demand for managed secure enterprise video communication platforms and deployment consulting

• By Deployment Mode

- On-Premises held 59.8% of the Enterprise Video Market in 2025, particularly among defense and financial institutions

- Cloud deployment is expanding at a 13.8% CAGR as organizations migrate internal video streaming for corporate training to SaaS architectures

• By End-User Industry

- IT and Telecommunications captured 27.6% revenue share of the Enterprise Video Market in 2025

- Healthcare is forecast to grow at a 17.1% CAGR, fueled by telehealth regulations and surgical video archiving

• By Region

- North America held 36.4% of Enterprise Video Market share in 2025

- Asia-Pacific is the fastest-growing region with a 13.5% CAGR, driven by 5G infrastructure build-outs

MRFR's proprietary estimation framework combines bottom-up vendor revenue analysis with top-down macroeconomic indicators, validated against primary interviews with 200+ enterprise IT decision-makers across 14 countries. Historical figures (2021–2024) are based on audited company filings and government ICT expenditure data, while the forecast trajectory (2026–2035) applies a calibrated compound growth model accounting for technology diffusion curves and regulatory catalysts.