Europe Beer Market Summary

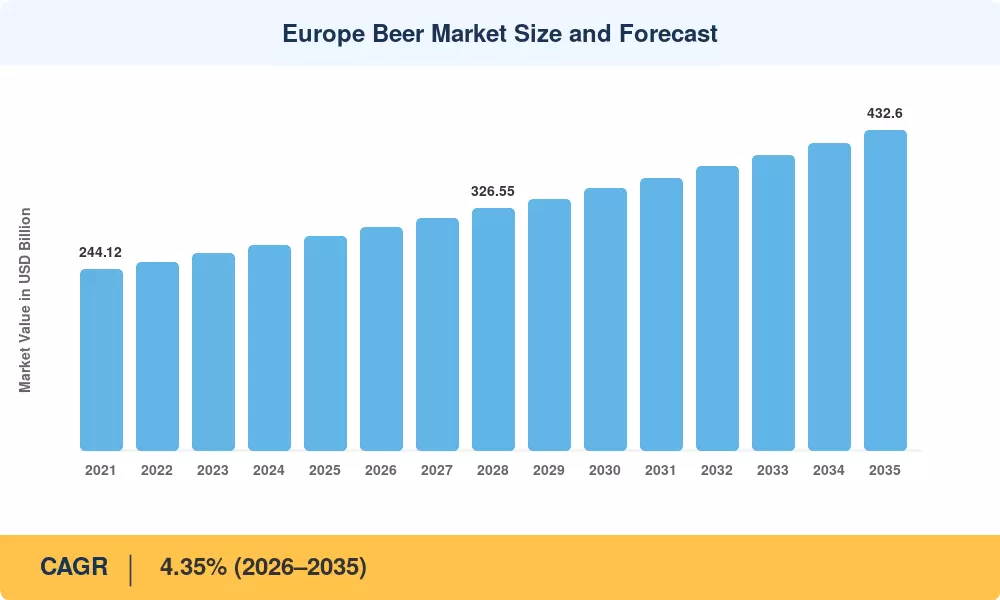

The Europe Beer Market reached an estimated USD 289.47 billion in 2025, positioning the continent as one of the world's most mature and culturally embedded brewing regions. From a 2026 base of USD 327.05 billion, the Europe Beer Market is projected to climb to USD 432.60 billion by 2035, expanding at a CAGR of 4.35% across the forecast window. This trajectory is anchored by two forces: the EU's ongoing revision of excise duty structures under Directive 92/83/EEC, which has incentivized craft beer production in lower-duty brackets [2], and a wave of premium beer investment that saw European brewers collectively commit over EUR 4.8 billion in capacity upgrades between 2022 and 2024 [3].

A silent revolution is changing how Europeans brew and drink beer. Legacy mass production lager lines are being replaced with modular craft brewing equipment that has IoT-enabled fermentation controls and AI-driven recipe optimization. Low- and no-alcohol beer options have gone from fringe novelty to mainstream shelf space in line with Europe’s Beating Cancer Plan, which is in line with international objectives to achieve a 10% relative decrease in harmful alcohol use. More than 68% of the total volume in the Europe Beer Market is now recyclable packaging, reflecting the consumer’s environmental consciousness as well as the EU Single-Use Plastics Directive [5].

Germany is the greatest producer and source of income on the continent and is the anchor of the regional market, contributing to over 28% of the total volume. The UK accounts for around 21% of the total Europe Beer Market income, driven by a vibrant craft ale pub culture and a solid on-trade rebound post-pandemic. France is the fastest-growing country with a forecast CAGR of 5.02%, powered by rising premium beer consumption among younger consumers, as Germany stays the anchor of European brewing traditions but embraces craft innovation

Key Report Takeaways

• By Product Type

- Lager accounted for approximately 83.6% of the Europe Beer Market share in 2025, reflecting deep-rooted consumer preferences across Germany, Spain, and Central Europe

- Ale is forecast to register a 6.12% CAGR through 2035, propelled by the UK craft ale pub trend and expanding Belgian-style specialty offerings

- Non/low-alcohol beer is on pace to reach USD 28.4 billion by 2035 as European premium beer consumption shifts toward health-conscious options

• By Category

- The standard segment represented the dominant share of the Europe Beer Market in 2025, reflecting price-sensitive purchasing across Southern and Eastern Europe

- Premium beer is projected to expand at a 5.10% CAGR through 2035, outpacing the overall Europe Beer Market growth rate

• By Region

- The United Kingdom led the Europe Beer Market with 22.8% of 2025 revenue, driven by on-trade channel recovery and craft ale pub trend expansion

- France is anticipated to post the strongest CAGR of 5.02% through 2035, benefiting from rising European craft beer growth among millennial consumers

Market Size and Forecast (2021–2035)

MRFR’s market sizing is based on the top-down revenue modeling using national excise tax filings, trade data from Eurostat, and bottom-up volumetric estimates from brewery organizations across 28 European nations. Historical data are cross-checked with Brewers of Europe annual reports. Simultaneously, projected forecasts use proprietary demand elasticity models calibrated to GDP growth, demographic changes and regulatory changes in the Europe Beer Market.