Field Force Automation Market Summary

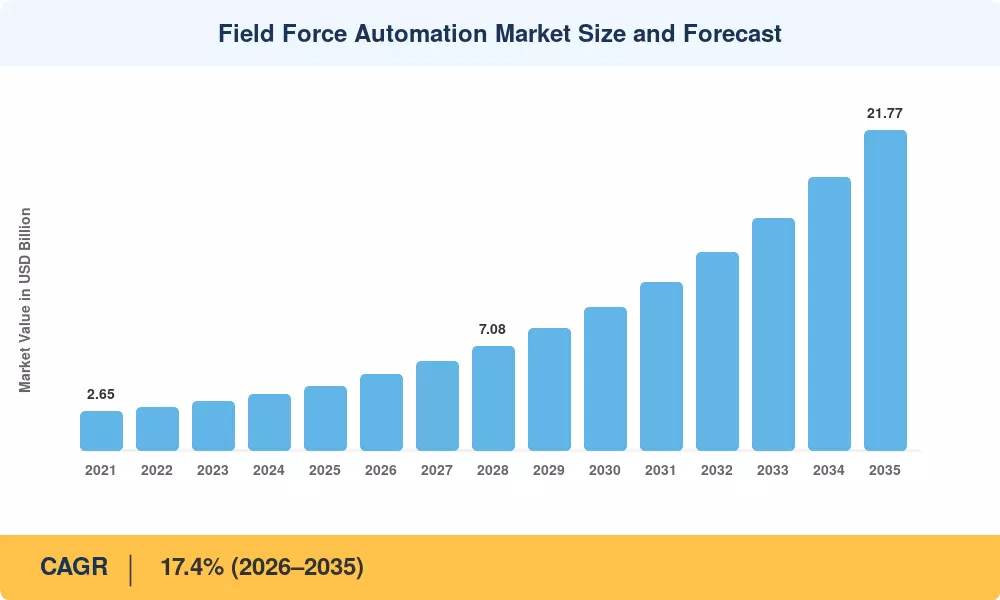

The Field Force Automation Market reached USD 4.38 Billion in 2025 and is forecast to grow from USD 5.14 Billion in 2026 to USD 21.77 Billion by 2035, registering a CAGR of 17.4% across the forecast window. Two catalysts anchor this trajectory: Electronic Visit Verification (EVV) mandates now active in all 50 US states, which compel home-health agencies to automate visit logging [1], and the commitment by 92% of large enterprises to increase AI spending on field operations between 2025 and 2028 [2]. These policy and investment pressures are converting field automation from a discretionary upgrade into a compliance-driven necessity.

A massive shift in technology is taking place beneath the top figures. AI-driven, cloud-first technologies that combine scheduling, inventory, routing, and customer contact into a single pane are replacing legacy paper-based dispatch and disjointed spreadsheet-driven scheduling. Latency hurdles that previously restricted real-time data sharing between field equipment and back-office systems are being collapsed by 5G rollouts, which are expected to reach 85% of the world's metropolitan population by 2030 [3]. Businesses that previously patched together GPS trackers and separate CRM apps are now investing in end-to-end orchestration suites, with platform licensing alone costing an average of USD 1,200 per field worker annually.

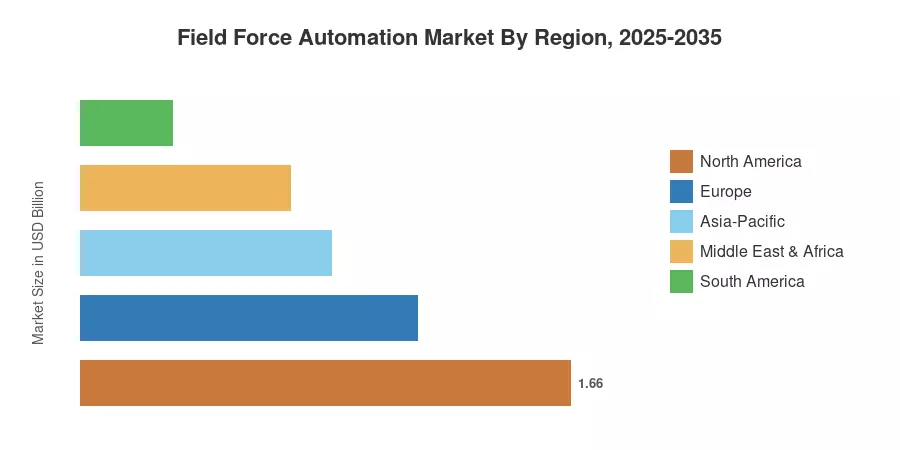

Due to same-day delivery economics and stringent regulatory compliance, North America holds around 38% of the worldwide field force automation market. With smart manufacturing projects and mobile broadband penetration growing at double the world rate, the Asia-Pacific is the fastest-growing region. Due to EU Green Deal rules that reward fleet-level carbon tracking—a feature that is becoming more and more integrated into field force platforms—Europe has the second-largest share, at roughly 26%. The field force automation market is expected to grow steadily in double digits well into the next ten years as outcome-based pricing models gain popularity.

Key Report Takeaways

• By Component

- Software/Solution dominated the Field Force Automation Market with a 72% share in 2025, reflecting the shift toward integrated platform suites that bundle scheduling, dispatch, and analytics.

- Services is the faster-growing component segment, advancing at a 15.5% CAGR through 2035 as enterprises outsource implementation, change management, and managed operations.

• By Deployment

- Cloud-based deployments captured 76% of the Field Force Automation Market in 2025, benefiting from lower upfront costs and elastic scalability.

• By Enterprise Size

- SMEs are set to grow at a 16.5% CAGR as affordable SaaS tiers and mobile-first interfaces lower the adoption threshold for smaller workforces.

• By Region

- North America led the Field Force Automation Market with an estimated 38% share in 2025, underpinned by EVV compliance and last-mile delivery pressures.

- Asia-Pacific is expanding at the highest regional CAGR of 19.3%, fueled by rapid 5G deployment and government-backed digital-manufacturing programs.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model combines top-down revenue estimates from vendor financials and contract databases with bottom-up demand signals from enterprise IT spending surveys across 42 countries. Historical figures (2021–2024) rely on audited annual reports; the base year (2025) is triangulated with primary interviews of 120+ field operations executives; forecast values (2026–2035) apply a constant CAGR calibrated against regression analysis of technology adoption curves and regulatory timelines.