Gas Turbine Market Summary

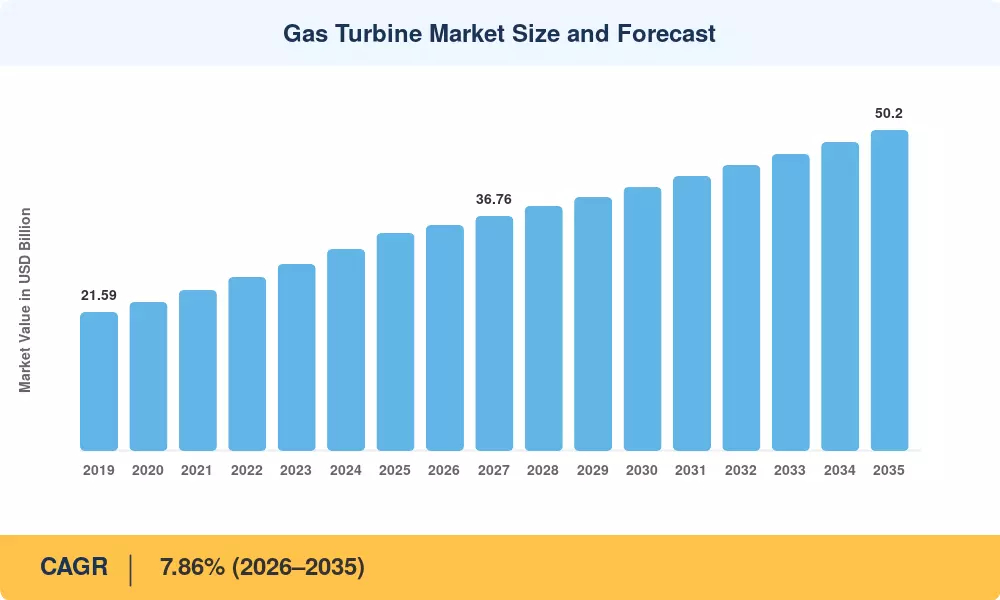

The global gas turbine market was valued at USD 34.010 billion in 2025 and is projected to reach approximately USD 35.897 billion by 2026, growing to USD 50.200 billion by 2035 at a compound annual growth rate of 3.80% during the 2026–2035 forecast period. Growth is fundamentally anchored by the increasing demand for reliable and efficient power generation solutions across both industrialized and emerging economies. The expanding global electricity demand—driven by urbanization, data-center proliferation, and electrification of transport—continues to reinforce the central role of gas turbines in baseload and peaking power infrastructure. Simultaneously, the growing emphasis on cleaner energy sources has accelerated the replacement of coal-fired assets with natural-gas-fired combined-cycle plants, which offer roughly half the carbon intensity per unit of electricity generated. Siemens Energy's USD 1 billion investment announced in November 2025 to expand gas turbine and grid equipment manufacturing in the United States underscores the scale of capital flowing into the sector [1].

With a 2025 valuation of USD 24,596.05 million, which reflects the installed base of big utility-scale plants worldwide, the heavy-duty turbine category leads the market in terms of both product and technology. However, because of its quick start-up time, small size, and suitability for dispersed generation and LNG applications, the aeroderivative segment—valued at USD 7,263.08 million in 2025—is the turbine type with the quickest rate of growth, with a CAGR of 5.24%. With a CAGR of 3.87%, combined-cycle technology accounts for USD 24,798.00 million of the 2025 market, demonstrating the industry's structural shift toward more efficient plant architectures. Next-generation fuel flexibility is becoming a competitive differentiator, as evidenced by significant developments like Mitsubishi Heavy Industries' June 2024 Memorandum of Understanding with the Electricity Generating Authority of Thailand to test 20% hydrogen co-firing in large gas turbines and Baker Hughes' contract to supply hydrogen-capable NovaLT12 turbocompressors to Italy's Snam [2][3].

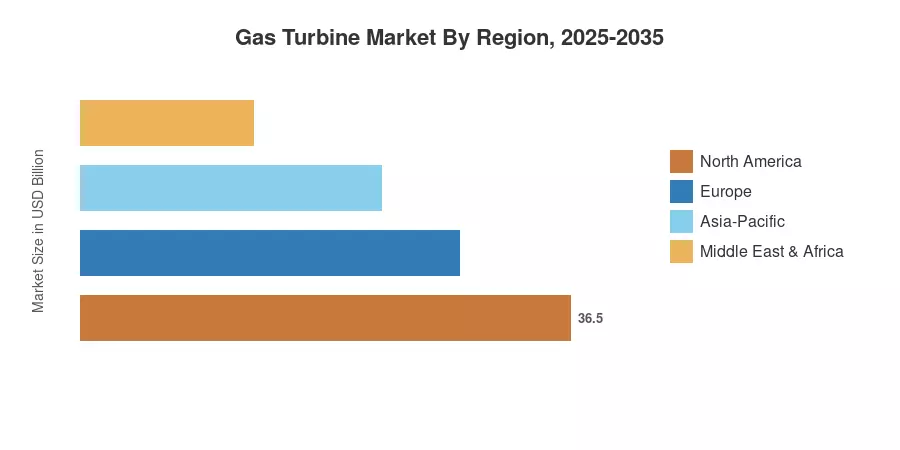

With a 2025 market value of USD 11,155.18 million, Asia Pacific leads the world in demand due to extensive capacity additions throughout China, India, and Southeast Asia. North America comes in second at USD 9,747.18 million, supported by robust legislative support for gas-to-power transitions and an established replacement and upgrade cycle. With a projected CAGR of 7.86%, the Middle East and Africa area is expected to grow at the fastest rate due to sub-Saharan electrification initiatives and infrastructure investments in Gulf Cooperation Council nations. Gas turbines function as a bridge fuel within the EU's taxonomic framework as Europe, the third-largest region with a GDP of USD 7,237.27 million, navigates a challenging energy transition. Through 2035, regional competitive dynamics will be increasingly defined by the convergence of grid-balancing requirements, digitization, and hydrogen readiness [4].

Key Report Takeaways

| Segment Dimension | Key Metric | Notes |

| By Type — Dominant | Heavy Duty: USD 24,596.05 Mn (2025) | Accounts for ~72% of the global market; driven by utility-scale baseload demand |

| By Type — Fastest Growing | Aeroderivative: CAGR 5.24% | Compact, fast-start capability suits distributed generation and LNG applications |

| By Rating Capacity — Dominant | Above 300 MW: USD 12,486.46 Mn (2025) | Large combined-cycle installations in the Asia Pacific and North America |

| By Rating Capacity — Fastest Growing | Less Than 40 MW: CAGR 4.85% | Growth in industrial cogeneration and remote/island power |

| By End-User — Dominant | Power Generation: USD 23,151.66 Mn (2025) | ~68% market share; core demand driver across all regions |

| By End-User — Fastest Growing | Marine: CAGR 5.01% | LNG-fueled marine propulsion and offshore FPSO demand |

| By Technology — Dominant | Combined Cycle: USD 24,798.00 Mn (2025) | Higher efficiency (>60% HHV) is favored in new-build power plants |

| By Technology — Fastest Growing | Combined Cycle: CAGR 3.87% | Regulatory push for fuel efficiency over open-cycle configurations |

| By Region — Dominant | Asia Pacific: USD 11,155.18 Mn (2025) | China, India, and Southeast Asia capacity additions |

| By Region — Fastest Growing | Middle East & Africa: CAGR 7.86% | GCC diversification, sub-Saharan electrification programs |

Market Size and Forecast (2019–2035)

Market Research Future employs a rigorous bottom-up and top-down methodology that triangulates supply-side revenue data from OEM financial disclosures, order-book announcements, and trade databases with demand-side indicators including power-plant commissioning schedules, government energy-sector capital expenditure plans, and utility procurement pipelines. The historical period (2019–2024) is validated against public financial filings and industry association reports, while the forecast period (2026–2035) incorporates regression analysis, expert interviews, and scenario modeling to project market trajectories under varying macroeconomic and policy conditions.