Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

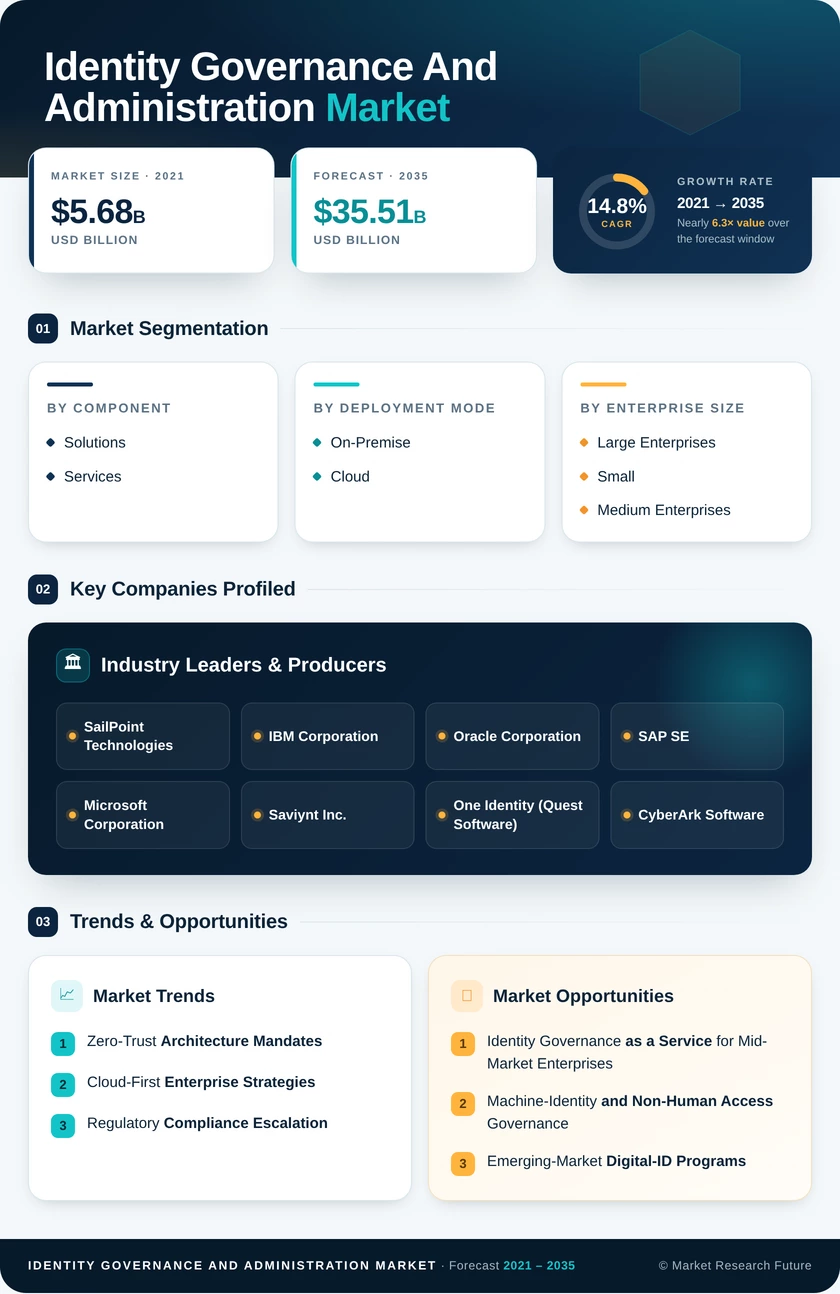

| Component | Solutions, Services | Solutions | Services |

| Deployment Mode | On-Premise, Cloud | Cloud | Cloud |

| Enterprise Size | Large Enterprises, Small and Medium Enterprises | Large Enterprises | Small and Medium Enterprises |

| End-User Vertical | BFSI, IT and Telecom, Energy and Utilities, Retail and E-Commerce, Identity Governance and Administration Market, Government | BFSI | Retail and E-Commerce |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Component

| Sub-Segment | Key Trend |

| Solutions | AI-embedded governance suites replacing rule-based policy engines; platform consolidation driving larger average deal sizes |

| Services | Managed governance services gaining traction as enterprises outsource certification administration and connector maintenance |

Solutions represent the largest revenue contributor, encompassing identity-analytics platforms, access-certification engines, and integration connector frameworks. Services are growing faster as implementation complexity and talent shortages push organizations toward managed and professional-service engagements.

By Deployment Mode

| Sub-Segment | Key Trend |

| On-Premise | Retained by defense, intelligence, and select healthcare organizations with sovereign-data or air-gapped-network requirements |

| Cloud | SaaS delivery accelerating time-to-value; multi-tenant architecture enabling AI-model improvement via aggregated telemetry |

Cloud deployment dominates due to lower infrastructure overhead and continuous-update delivery models. On-premise retains a structural niche where regulatory or classification requirements preclude cloud migration.

By Enterprise Size

| Sub-Segment | Key Trend |

| Large Enterprises | Complex multi-application environments requiring enterprise-grade governance with deep connector ecosystems |

| Small and Medium Enterprises | Subscription SaaS pricing removing capital-expenditure barriers; pre-configured policy templates accelerating adoption |

Large enterprises drive majority spending, while SMEs represent the fastest-growing segment as SaaS models democratize access to governance capabilities previously reserved for Fortune 500 organizations.

By End-User Vertical

| Sub-Segment | Key Trend |

| Banking, Financial Services, and Insurance | Regulatory mandates (DORA, SOX, PCI DSS) making governance a non-negotiable compliance expenditure |

| IT and Telecom | Distributed DevOps and multi-cloud environments increasing identity-sprawl complexity |

| Energy and Utilities | OT-IT convergence and NERC CIP compliance driving IGA adoption in critical infrastructure |

| Retail and E-Commerce | Consumer-data regulations and partner-ecosystem sprawl creating new governance requirements |

| Identity Governance and Administration Market | HIPAA audit intensity and EHR interoperability mandates sustaining steady governance demand |

| Government | Zero-trust mandates and digital-citizen-service platforms expanding governance scope |

BFSI leads as the dominant vertical, with retail and e-commerce exhibiting the highest growth trajectory as digital-commerce identity volumes scale.

By Geography

| Sub-Segment | Key Trend |

| North America | Federal zero-trust mandates and mature vendor ecosystem sustaining market leadership |

| Europe | DORA and NIS2 enforcement converting discretionary governance spending into mandatory budget items |

| Asia-Pacific | Digital-ID programs and banking modernization across India, Japan, and South Korea fueling rapid adoption |

| South America | LGPD enforcement and fintech growth driving governance demand, primarily in Brazil |

| Middle East & Africa | Sovereign-cloud mandates and Vision 2030 IT programs creating nascent but growing demand |

North America retains the dominant share, while Asia-Pacific is positioned as the fastest-growing region through 2035.