Industrial Automation Market Summary

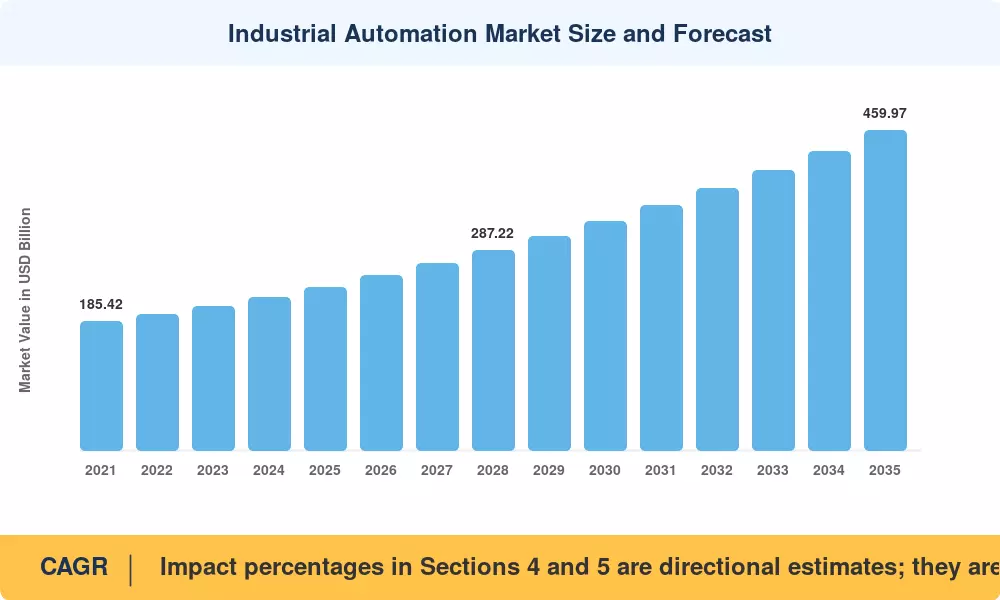

The Industrial Automation Market was valued at USD 234.72 Billion in 2025 and is projected to grow from USD 251.06 Billion in 2026 to USD 459.97 Billion by 2035, registering a CAGR of 6.96% during the forecast period (2026–2035). Smart-factory initiatives backed by government reshoring incentives across the United States and the European Union have been the primary demand catalysts, with an estimated USD 48 Billion in combined public-private automation investment pledged between 2023 and 2025 alone [1]. A widening skilled-labor gap in manufacturing economies — the U.S. National Association of Manufacturers projects 2.1 million unfilled factory jobs by 2030 — continues to push plant operators toward automated alternatives [2].

Technology-wise, legacy relay-based control architectures are giving way to cloud-connected SCADA, distributed control systems (DCS), and AI-enhanced programmable logic controllers. The IEC 62443 cybersecurity standard update in 2024 triggered a wave of brownfield retrofits, while the convergence of machine vision, edge computing, and digital twins slashed changeover times by up to 35% on pilot lines [3]. Capital spending on industrial robots reached a record 540,000 unit installations globally in 2023, according to the International Federation of Robotics [4].

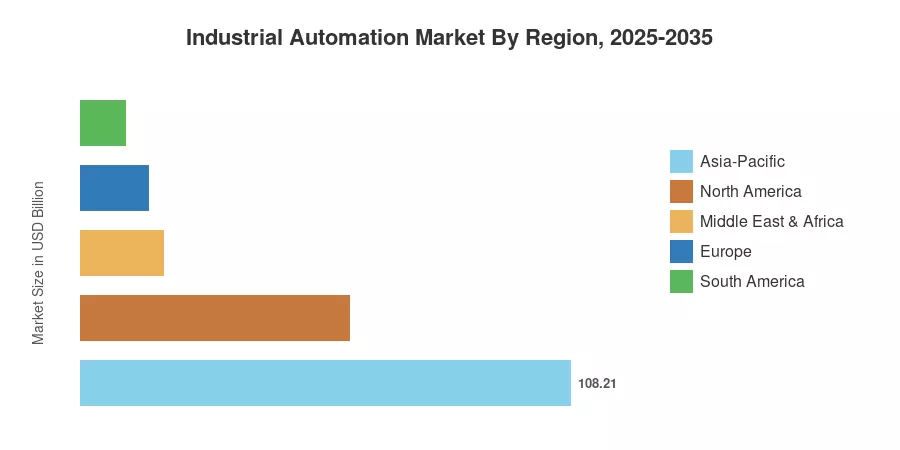

Asia-Pacific commanded an estimated 46.10% share of the Industrial Automation Market in 2025, fueled by China's "Made in China 2025" legacy programs and India's Production-Linked Incentive schemes. North America held the second-largest regional share at roughly 25.30%, driven by automotive and semiconductor reshoring. Europe accounted for about 20.40% of global revenue, with Germany's Industrie 4.0 framework anchoring demand. As energy-efficiency mandates tighten worldwide and robotics unit costs decline, the Industrial Automation Market is set for sustained multi-year expansion through 2035.

Key Report Takeaways

• By Solution

- Industrial control systems captured approximately 48.20% of Industrial Automation Market revenue in 2025, reflecting persistent demand for SCADA, DCS, and PLC upgrades across process industries.

- Robotics within the field devices segment is forecast to expand at a 12.80% CAGR through 2035, the fastest among solution categories, driven by collaborative and mobile robot adoption.

• By Automation Type

- Fixed automation held a 39.30% revenue share in 2025, underpinned by high-throughput automotive and electronics assembly lines.

- Flexible and modular automation is projected to register a 12.50% CAGR to 2035, as manufacturers invest in reconfigurable production cells.

• By End-User Industry

- Automotive and transportation accounted for 27.80% of Industrial Automation Market value in 2025, supported by EV battery-line build-outs.

- Pharmaceuticals is poised to grow at a 9.50% CAGR through 2035, catalyzed by serialization mandates and continuous manufacturing adoption.

• By Deployment Mode

- On-premises systems held a 69.10% share of the Industrial Automation Market in 2025, favored for latency-sensitive and air-gapped operations.

- Cloud-based deployments are expanding at a 13.80% CAGR, unlocking remote monitoring and analytics at scale.

• By Region

- Asia-Pacific led the Industrial Automation Market with a 46.10% share in 2025 and remains the fastest-growing region at an 11.30% CAGR.

- North America accounted for about 25.30% of global revenues, buoyed by CHIPS Act-adjacent factory construction.

Industrial Automation Market Size and Forecast (2021–2035)

Market Research Future employs a hybrid estimation methodology that triangulates vendor revenue disclosures, customs trade data, and bottom-up capacity analysis across more than 40 automation product categories. Historical figures (2021–2024) are anchored to audited annual reports and validated against IFR and IEC databases. The forecast (2026–2035) applies the calibrated 6.96% CAGR, adjusted for cyclical capex patterns, regional policy shifts, and technology adoption curves.

.webp?v=1785211181)