Lubricant Additives Market Summary

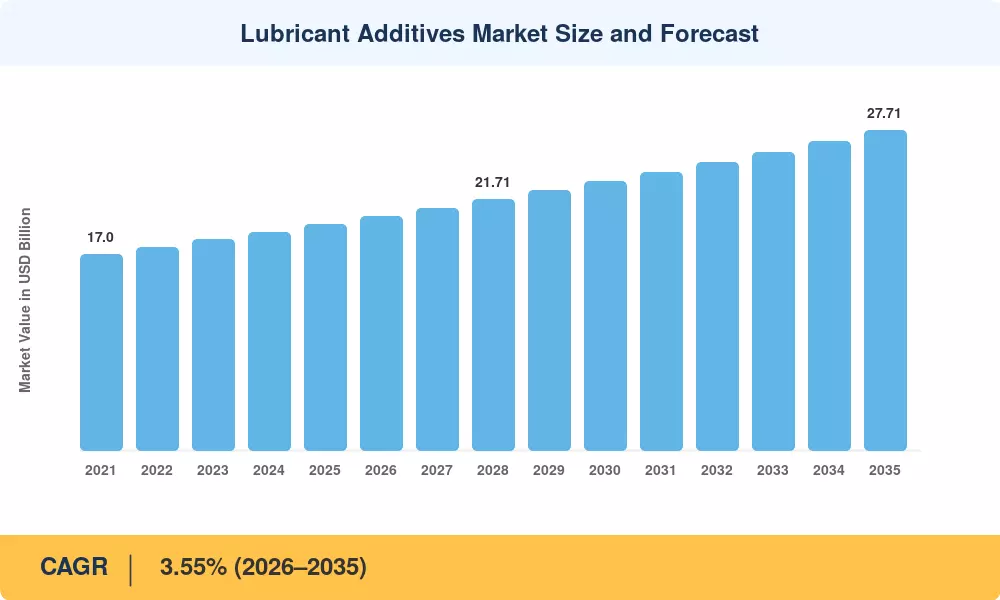

The Lubricant Additives Market reached USD 19.55 billion in 2025 and is projected to climb to USD 20.24 billion by 2026 before reaching USD 27.71 billion by 2035, advancing at a 3.55% CAGR over the 2026–2035 forecast window. Two catalysts anchor this trajectory: the March 2025 introduction of ILSAC GF-7 engine oil specifications — which mandate tighter emission controls and lower viscosity grades — and a global push by OEMs toward extended drain intervals that favor premium, multi-functional additive packages [2]. These regulatory and performance pressures are shifting the industry from volume-driven expansion toward value-focused innovation in engine oil additives and corrosion inhibitor additives.

The market for lubricant additives is changing, with modern multi-component packages taking the place of outdated single-function chemistries. Older zinc-heavy anti-wear compounds are being replaced in both passenger car and industrial uses by nano-scale additive technologies, low-SAPs formulations, and bio-based detergent additives. According to a latest report, the world invested more than USD 2.3 billion in next-generation lubricant chemistry in 2024 alone, with the biggest R&D expenditures going to dispersant and viscosity improvers [3].

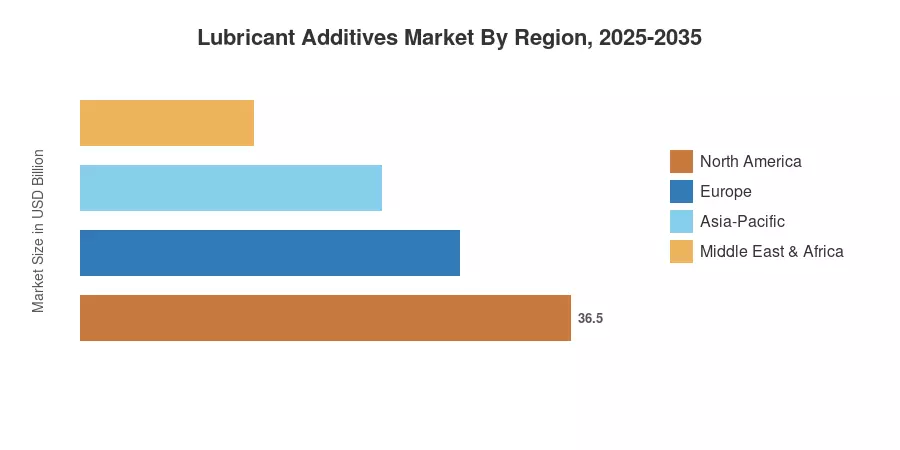

With roughly 48.2% of global revenue, Asia-Pacific holds the top spot thanks to rising automobile manufacturing in China and India, as well as rising industrial lubricant compound demand throughout ASEAN economies. Because of strict EPA and CARB regulations that hasten the adoption of performance lubricant compounds, North America has an estimated 22.0% share. Approximately 21.0% of income comes from Europe, the third-largest region. The market for high-value specialized oil additives will continue through 2035 due to electrification trends and tighter pollution regulations in every region.

Key Report Takeaways

• By Function Type

- Dispersants and Emulsifiers captured 31.2% of the Lubricant Additives Market revenue in 2025, reflecting their critical role in soot management and sludge prevention.

- Viscosity Index Improvers are expanding at a 3.92% CAGR through 2035, fueled by global demand for fuel-efficient, low-viscosity formulations.

• By Lubricant Type

- Engine Oil accounted for 58.2% of the Lubricant Additives Market share in 2025, driven by rising passenger vehicle parc globally.

- Metalworking Fluid additives are projected to reach the fastest segment CAGR of 4.15% through 2035, supported by industrial automation expansion.

• By End-User Industry

- Automotive and Other Transportation held a 66.3% share in 2025, underscoring the dominance of automotive lubricant chemicals demand.

- Power Generation is advancing at a 4.32% CAGR to 2035, driven by gas turbine fleet modernization and distributed energy systems.

• By Geography

- Asia-Pacific leads the Lubricant Additives Market with a 4.28% CAGR through 2035, the fastest among all regions.

- North America contributed USD 4.30 billion in 2025, anchored by the US market's regulatory-driven demand for advanced fuel additive chemicals.

Lubricant Additives Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s market sizing combines bottom-up revenue modeling from over 120 additive manufacturers, blenders, and distributors with top-down demand-side analysis benchmarked against API, ATIEL, and ILSAC specification adoption rates. Historical data (2021–2024) draws on verified company filings, trade body statistics, and customs data; the 2025 base year integrates primary survey responses from 85 procurement executives across five regions.

.webp?v=1783929032)