Synthetic Lubricant Market Summary

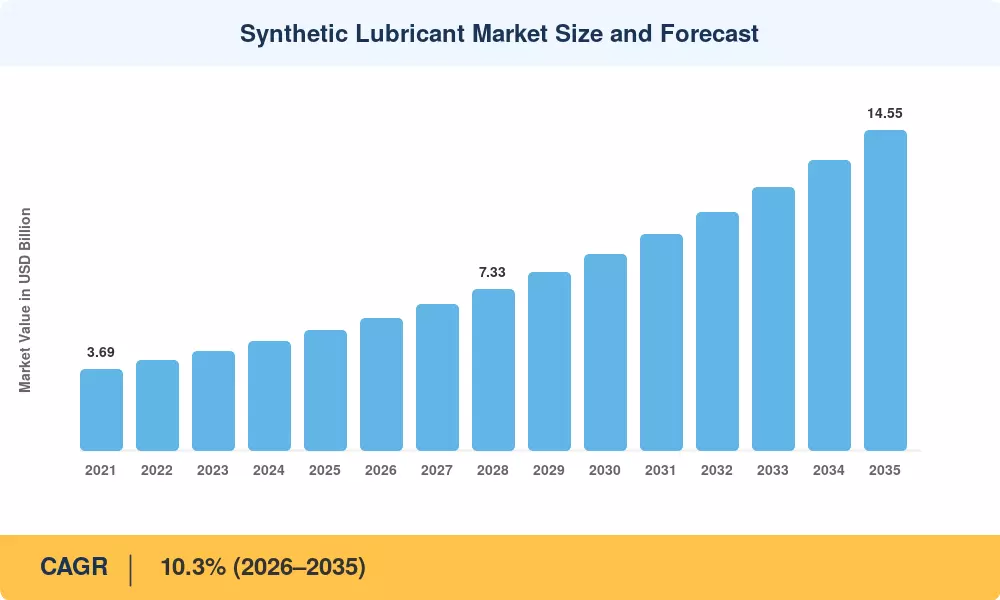

The Synthetic Lubricant Market reached a valuation of USD 5.46 billion in 2025 and is projected to climb from USD 6.02 billion in 2026 to USD 14.55 billion by 2035, registering a CAGR of 10.3% across the forecast window. Two forces are propelling this acceleration: tightening fuel-economy mandates — led by the U.S. EPA's Phase 3 greenhouse-gas standards and Euro 7 emission limits — and expanding factory automation that demands lubricants capable of operating under extreme thermal envelopes [1][2]. Capital commitments in this space have intensified, with combined capacity expansions exceeding USD 2.8 billion globally between 2023 and 2025.

A generational technology shift is rewriting formulation playbooks. Conventional mineral-oil blends, long the workhorse of engine and industrial applications, are steadily losing ground to Polyalpha-Olefin (PAO) and Polyalkylene Glycol (PAG) chemistries engineered for tighter tolerances and longer drain intervals. The introduction of the ILSAC GF-7 specification in March 2025 codified this transition, compelling automakers and aftermarket service networks to adopt next-generation formulations [3]. Metallocene-catalyst PAO plants commissioned in South Korea, Saudi Arabia, and the U.S. Gulf Coast are adding more than 400 kilotonnes of annual capacity to address this reformulation wave [4].

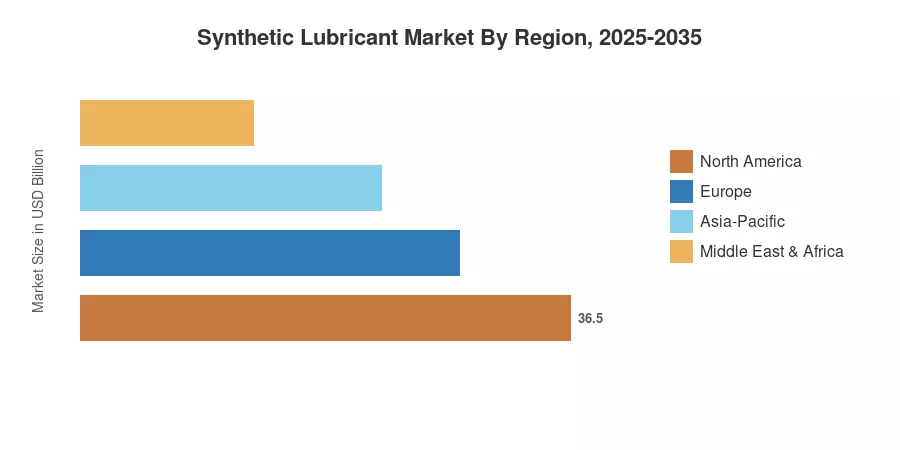

Asia-Pacific commands roughly 43% of the Synthetic Lubricant Market, anchored by China's sprawling manufacturing base and India's recovering vehicle fleet. The region is also the fastest-growing, tracking an 11.4% CAGR through 2035. North America holds the second-largest share at approximately 24%, driven by stringent OEM specifications and the shale sector's demand for high-temperature drilling fluids. Europe follows closely at 22%, where carbon-neutrality targets are accelerating the substitution of petroleum-derived lubricants [5]. The decade ahead will be shaped by the convergence of electrification, sustainability mandates, and predictive-maintenance technologies.

Key Report Takeaways

• By Product Type

- Engine oils captured an estimated 36.5% of the Synthetic Lubricant Market in 2025, reflecting widespread OEM factory-fill adoption across passenger and commercial vehicles.

- Metalworking fluids are on track to be the fastest-growing product category at an 11.6% CAGR through 2035, fueled by precision CNC machining and automated manufacturing lines.

• By Base Oil

- PAO-based formulations held roughly 49% share of the Synthetic Lubricant Market in 2025, preferred for their oxidative stability and low-temperature fluidity.

- PAG-based lubricants are forecast to expand at an 11.7% CAGR to 2035, gaining traction in refrigeration compressors and food-grade applications.

• By End User

- Automotive applications represented approximately 38% of the Synthetic Lubricant Market in 2025.

- Heavy equipment is poised to register an 11.1% CAGR to 2035, lifted by infrastructure spending in emerging economies.

• By Region

- Asia-Pacific led with a 43% share of the Synthetic Lubricant Market in 2025 and is advancing at an 11.4% CAGR.

Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from customs-trade data, manufacturer disclosures, and downstream consumption surveys, cross-validated against independent benchmarks. Forecast projections apply a compound annual growth model anchored to the 2025 base year and adjusted for regulatory phase-in schedules, capacity additions, and macroeconomic indicators published by the IMF and World Bank [6].