Polypropylene Market Summary

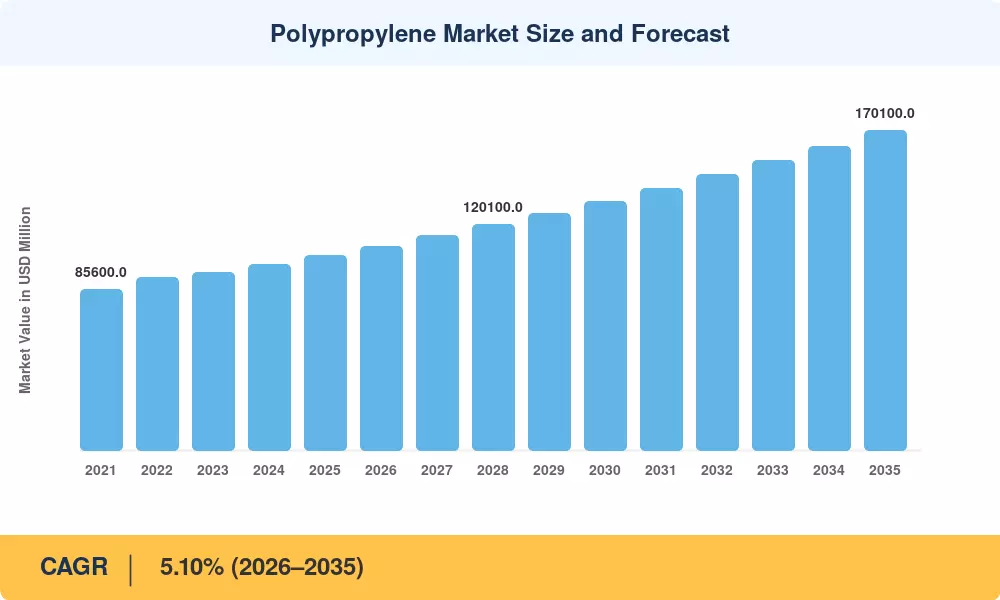

The Polypropylene Market reached an estimated USD 103,400 Million in 2025 and is projected to grow from USD 108,700 Million in 2026 to USD 170,100 Million by 2035, advancing at a 5.10% CAGR over the forecast window. Sustained capital investment in propane dehydrogenation (PDH) plants across North America and China—exceeding USD 14 billion in announced greenfield projects since 2022—continues to reshape the global polypropylene resin supply map [2]. Government-led circular-economy mandates, including the EU Single-Use Plastics Directive and India's Extended Producer Responsibility framework, are accelerating shifts toward mono-material plastic packaging materials and recyclable polypropylene structures that favor the Polypropylene Market over competing resins.

A generational technology shift is underway in the Polypropylene Market as legacy Ziegler-Natta catalyst platforms give way to advanced metallocene and post-metallocene systems. These next-generation catalysts unlock high-melt-strength polypropylene resin grades capable of foaming, thermoforming, and bi-axial stretching—applications historically dominated by polystyrene and polyethylene terephthalate [3]. Major producers have collectively committed more than USD 2.8 billion toward specialty catalyst R&D and commercial-scale reactor retrofits between 2024 and 2028, targeting lightweight polymer materials for automotive interiors, food-contact flexible plastic packaging, and medical non-wovens.

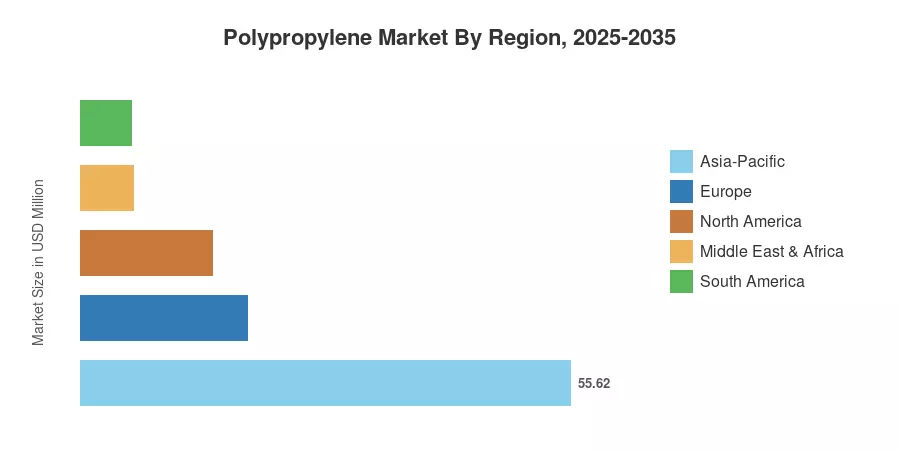

Asia-Pacific commands roughly 54.0% of the polypropylene market volume, driven by China's integrated refinery-petrochemical complexes and India's rising consumer goods demand The region simultaneously registers the fastest projected CAGR among all geographies. Europe holds the second-largest share at 18.4%, buoyed by stringent recycling targets that incentivize thermoplastic polymer materials over thermosets. North America, accounting for 15.2%, benefits from shale-derived propylene feedstock economics that keep production costs structurally competitive through 2035.

Key Report Takeaways

• By Type

- Homopolymer captured 64.0% of the polypropylene market share in 2025, driven by high stiffness-to-cost ratios in injection molding plastics and rigid containers

- Copolymer polypropylene resin is forecast to post a 5.48% CAGR through 2035, fueled by growing demand for impact-resistant automotive plastic components and cold-chain flexible plastic packaging

• By Processing Technology

- Injection molding accounted for 41.2% of the Polypropylene Market in 2025, reflecting broad uptake across consumer goods and industrial plastic products

- Extrusion molding is expected to generate USD 33,200 million by 2035, supported by rising film and sheet output for plastic packaging materials

• By End-User Industry

- Packaging led with a 46.8% revenue share in the Polypropylene Market in 2025, anchored by flexible plastic packaging and rigid container demand

- Automotive end use is projected to expand at a 6.53% CAGR through 2035, as OEMs intensify substitution of metal parts with lightweight polymer materials

• By Region

- Asia-Pacific dominated with 54.0% of the global Polypropylene Market volume in 2025

- North America accounted for 15.2% of volume, underpinned by cost-advantaged propane dehydrogenation capacity and polymer manufacturing materials investments

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s estimates integrate bottom-up plant-capacity modelling with top-down demand verification across 42 countries. Historical figures draw on customs trade data, producer shipment records, and industry association statistics. Forecast values reflect the 5.10% calibrated CAGR applied to the 2026 base, adjusted for announced capacity additions and anticipated demand shifts in thermoplastic polymer materials end markets.