Polyurethane Coatings Market Summary

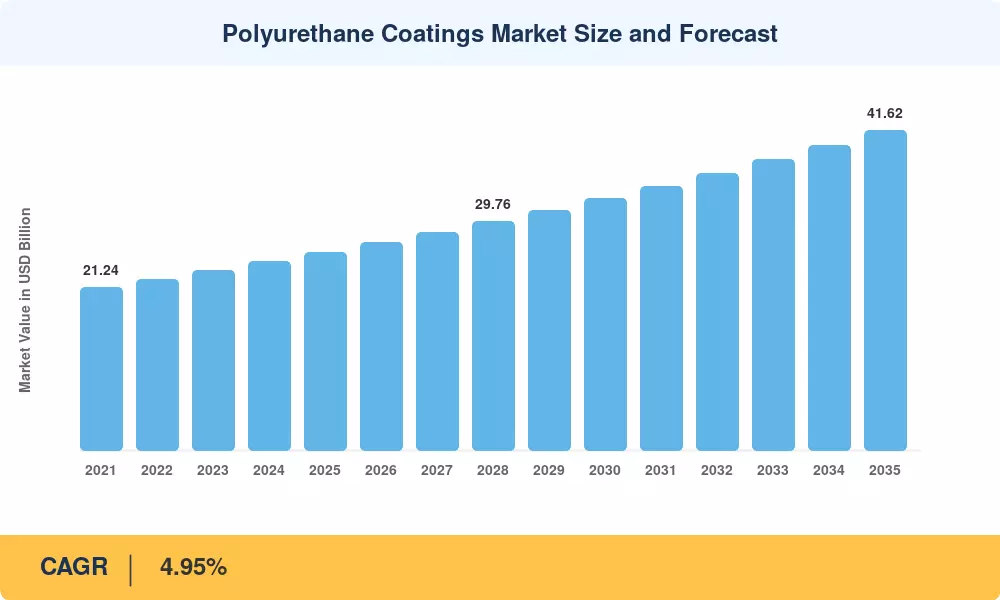

The Polyurethane Coatings Market stood at USD 25.77 Million in 2025 and is projected to reach USD 41.62 Million by 2035, expanding at a 4.95% CAGR over the 2026–2035 forecast window. From a 2026 starting value of USD 26.95 million, steady demand growth reflects tightening VOC emission regulations across the EU and North America, alongside accelerating construction activity in Asia-Pacific economies. The Polyurethane Coatings Market benefits directly from policy catalysts such as the European Green Deal's push toward low-emission building materials and the U.S. EPA's 2024 National Emission Standards update, both of which channel specifiers toward compliant polyurethane systems [1][2].

A technology transition is underway within the Polyurethane Coatings Market as traditional solvent-borne formulations face substitution pressure from waterborne dispersions and radiation-cured chemistries. Global investment in bio-based polyol feedstocks exceeded USD 1.2 billion between 2022 and 2024, driven by BASF, Covestro, and mid-tier formulators seeking isocyanate-free curing pathways [3]. Governments in China and India now mandate maximum solvent content thresholds for architectural and industrial applications, accelerating reformulation timelines.

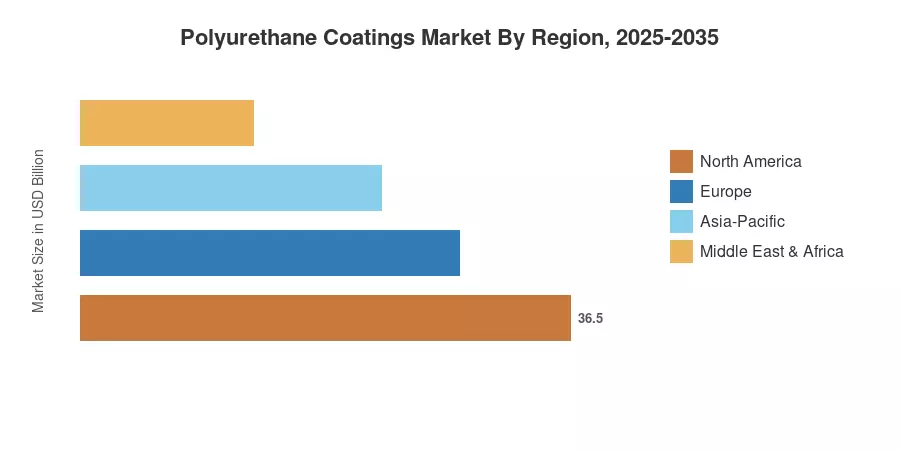

Asia-Pacific commands roughly 39.8% of the Polyurethane Coatings Market, underpinned by China's infrastructure pipeline and India's Smart Cities Mission. The region also registers the fastest CAGR at 5.79% through 2035. North America holds the second-largest position at 24.5% share, supported by automotive OEM refinish cycles and aerospace MRO spending. Europe follows closely, leveraging sustainability mandates to drive waterborne adoption. As circular-economy raw materials gain commercial scale, the Polyurethane Coatings Market is positioned for sustained medium-term expansion across all end-use verticals.

Key Report Takeaways

• By Technology

- Solvent-borne coatings held a 43.9% revenue share in 2025, retaining the largest technology segment position within the Polyurethane Coatings Market despite regulatory headwinds.

- Water-borne technology is the fastest-growing segment, projected to advance at a 7.20% CAGR through 2035 as OEMs and architectural specifiers shift toward low-VOC formulations.

• By End-User Industry

- Automotive applications captured 31.6% of the Polyurethane Coatings Market in 2025, driven by OEM primer and clearcoat demand cycles.

- Construction end-use is expanding at a 5.28% CAGR through 2035, propelled by green building certifications and waterproofing specifications.

• By Region

- Asia-Pacific contributed 39.8% of global revenue in 2025, the dominant regional market.

- South America is projected to register a 5.45% CAGR, the second-fastest regional growth rate, led by Brazilian infrastructure investment.

Market Size and Forecast (2021–2035)

Market Research Future derives market sizing through a triangulated methodology combining bottom-up supply audits of resin producers, top-down end-user demand modeling, and cross-validation against publicly reported revenues of the top 10 coatings companies. All figures are expressed in constant 2025 USD.