Probiotics Market Summary

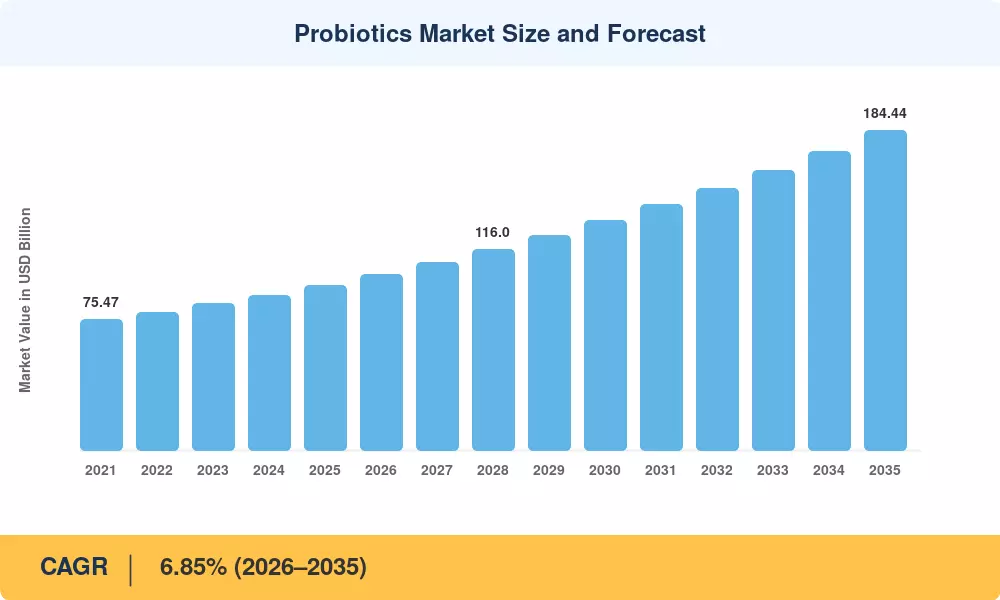

The Probiotics Market reached a valuation of USD 95.10 Billion in 2025 and is projected to grow from USD 101.61 Billion in 2026 to USD 184.44 Billion by 2035, registering a CAGR of 6.85% during the forecast period (2026–2035). Heightened consumer prioritization of preventive wellness, combined with the FDA's 2024 qualified health claim for yogurt and accelerating clinical research into strain-specific benefits, has pushed the Probiotics Market into a sustained expansion phase. Manufacturers are channeling capital toward precision formulation, direct-to-consumer e-commerce models, and supply-chain automation to protect premium margins as mainstream adoption deepens[2].

A structural transformation is underway across the industry. Legacy commodity-grade cultures are giving way to clinically validated, strain-specific formulations backed by randomized controlled trials. The Chr. Hansen–Novozymes merger — creating Novonesis with an estimated annual R&D budget exceeding USD 450 Million — exemplifies how consolidation is accelerating technology diffusion and raising barriers for smaller producers [3][4]. AI-enabled personalization platforms now allow brands to tailor strain combinations to individual gut-microbiome profiles, a capability that barely existed five years ago.

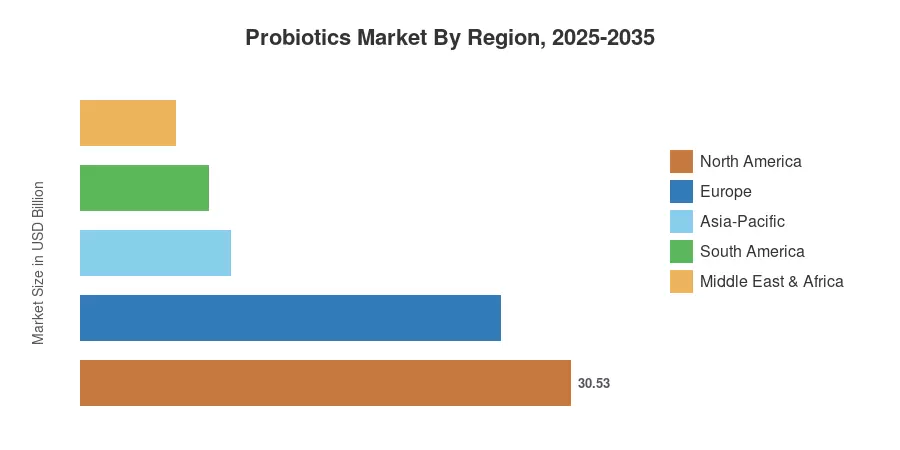

North America commands 32.10% of the Probiotics Market, anchored by progressive regulatory signals and high supplement penetration. Asia-Pacific represents the fastest-growing region at a 9.85% CAGR, driven by rising middle-class health spending across China, India, and Southeast Asia. Europe holds roughly 27.50% share, with regulatory harmonization under EFSA accelerating new product approvals. As clinical evidence mounts and distribution infrastructure matures in emerging economies, the Probiotics Market is positioned for broad-based global expansion through 2035.

Key Report Takeaways

• By Product Type

- Probiotic Foods accounted for 49.60% of the Probiotics Market in 2025, reflecting entrenched consumer preference for functional yogurts, kefir, and cultured dairy.

- Dietary Supplements are projected to expand at an 8.59% CAGR through 2035, propelled by capsule, gummy, and powder innovations targeting specific health outcomes.

• By Function

- Digestive and Gut Health captured 39.82% of revenue share in the Probiotics Market during 2025, underscoring its foundational role in consumer purchasing decisions.

- Immunity Enhancement is advancing at a 7.72% CAGR to 2035, with post-pandemic awareness sustaining demand.

• By Distribution Channel

- Pharmacies and Drug Stores commanded 37.52% of the Probiotics Market in 2025, benefiting from pharmacist-led consumer education.

- Online Stores are expanding at a 9.59% CAGR, as subscription models and digital health ecosystems reshape purchasing behavior.

• By Region

- North America led the Probiotics Market with 32.10% share in 2025, supported by FDA regulatory tailwinds.

- Asia-Pacific is forecast to accelerate at a 9.85% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated approach combining top-down revenue estimation, bottom-up product-level tracking, and validation against trade-association shipment data and company filings. Historical figures (2021–2024) reflect audited industry data, while the forecast period (2026–2035) applies econometric modeling calibrated to macroeconomic health-spending indicators.

.webp?v=1783077051)