Propylene Glycol Market Summary

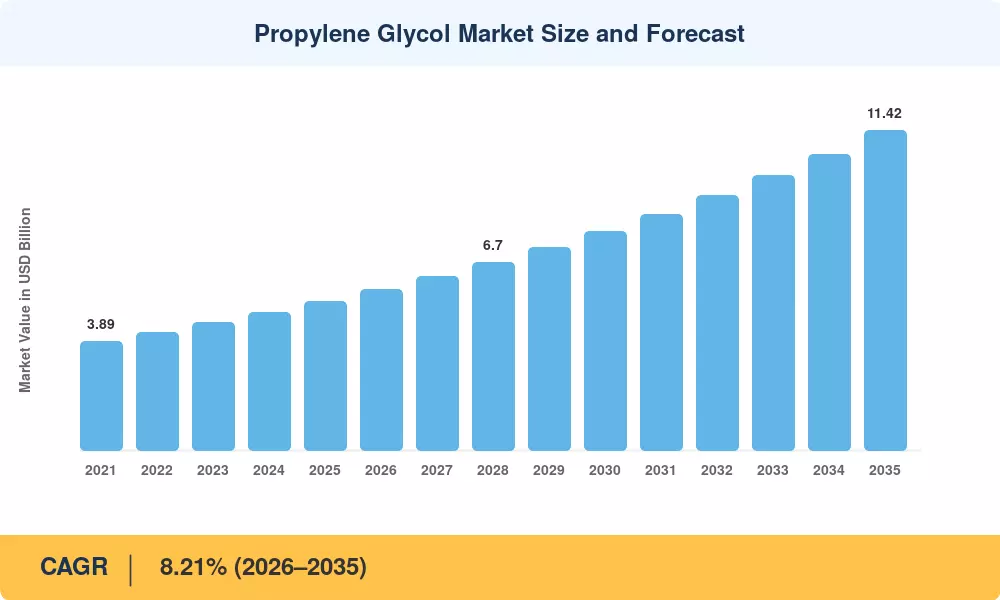

The Propylene Glycol Market reached an estimated 5.33 million tons in 2025 and is projected to expand from 5.72 million tons in 2026 to 11.42 million tons by 2035, reflecting an 8.21% CAGR across the forecast window. Two forces anchor this trajectory: the global wind-energy buildout—where unsaturated polyester resins consume large volumes of industrial glycol chemicals for turbine-blade composites—and tightening pharmacopeia standards that push drug manufacturers toward USP-grade pharmaceutical solvents in injectable formulations. The U.S. Inflation Reduction Act alone has catalyzed over USD 45 billion in clean-energy manufacturing commitments since 2023, many of which depend on composite materials fed by propylene glycol derivatives [2].

Direct catalytic conversion methods, which reduce unit costs by 12–18% and make the incorporation of bio-circular feedstocks easier, are replacing the traditional two-step propylene oxide hydration in production technology. In food-grade propylene glycol and personal care chemicals, companies with International Sustainability and Carbon Certification (ISCC) PLUS certifications now command a 6–9% price premium, dividing the market into commodity and sustainability-attributed tiers [3]. Near-term margins on commodity grades are being strained by significant capacity increases in China, which are projected to add 800,000 tons of new nameplate capacity between 2024 and 2027.

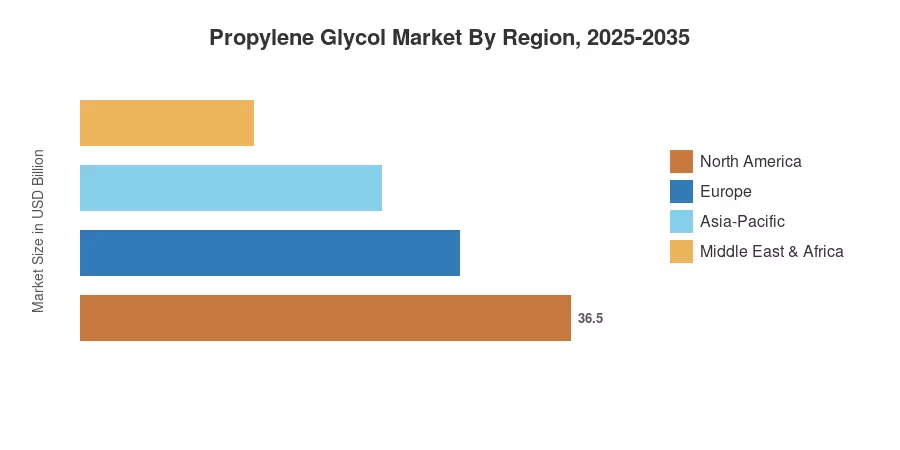

With around 49% of the world's volume, Asia-Pacific leads the propylene glycol market thanks to China's building boom and India's growing pharmaceutical exports. Due to petrochemical diversification in Saudi Arabia and the United Arab Emirates, the Middle East and Africa area is expected to have the greatest CAGR of 9.32% through 2035 North America has the second-largest share, at around 22%, thanks to the benefits of propylene oxide feedstock obtained from shale and the strong demand for antifreeze chemicals in the automobile aftermarket.

Key Report Takeaways

• By Application

- Unsaturated polyester resins commanded a 34.16% share of the Propylene Glycol Market in 2025, supported by wind-energy composite demand and infrastructure spending

- Personal-care intermediates and cosmetic ingredients are projected to expand at an 8.58% CAGR through 2035, reflecting consumer shifts toward low-toxicity formulations

- Antifreeze chemicals and heat transfer fluids together accounted for approximately 1.12 million tons in 2025, with electric-vehicle thermal management accelerating uptake

• By End-User Industry

- Food and beverages represented 30.14% of the Propylene Glycol Market demand in 2025, led by food-grade propylene glycol use as a humectant and flavoring carrier

- The pharmaceutical sector is forecast to post the fastest end-user growth at 8.72% CAGR, driven by demand for high-purity pharmaceutical solvents in parenteral drug delivery

• By Regional

- Asia-Pacific captured 49% of the global Propylene Glycol Market volume in 2025

- The Middle East & Africa region is expected to register the highest regional CAGR of 9.32% through 2035

- North America accounted for roughly 22% of global consumption, anchored by industrial solvent materials demand and shale-based feedstock cost advantages

Propylene Glycol Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework combines supply-side capacity tracking, trade-flow analysis, and demand-side consumption modeling across 28 countries. Historical figures (2021–2024) draw on customs data and producer disclosures; the 2025 base year blends Q1–Q3 actuals with Q4 estimates. Forecast values (2026–2035) apply segment-level growth drivers validated against macroeconomic indicators from the World Bank, IEA, and OECD.

.webp?v=1783671528)