Shore Power Market Summary

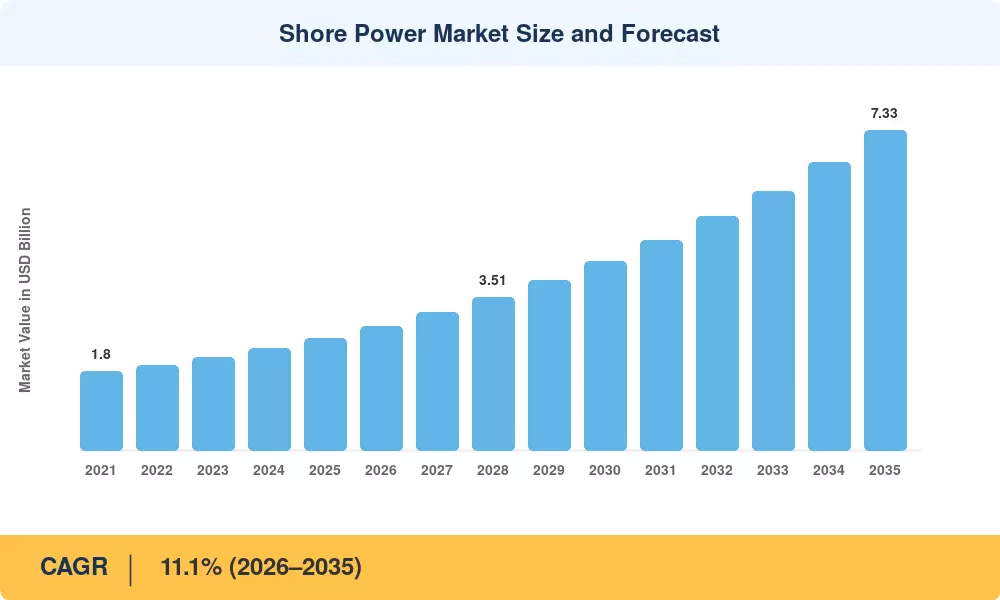

The Shore Power Market reached an estimated USD 2.56 Billion in 2025 and is projected to grow from USD 2.84 Billion in 2026 to USD 7.33 Billion by 2035, registering a CAGR of 11.1% during the forecast period (2026–2035). Tightening emission mandates from the International Maritime Organization (IMO) and regional bodies such as the European Union, which now require at-berth emission reductions of up to 90% for vessels calling at major ports, are the primary catalysts propelling the Shore Power Market forward [1]. National port-electrification funds—including the U.S. EPA's USD 3 billion Clean Ports Program and China's Green Port Action Plan—are accelerating capital deployment at an unprecedented pace [2].

A structural shift is underway as ports retire diesel-powered auxiliary engine operations in favor of grid-connected electrical supply systems. Frequency converters, high-voltage switchgear, and automated cable-management systems now form the backbone of modern berth electrification projects, replacing ad-hoc generator setups that dominated the previous decade. The European Commission's FuelEU Maritime regulation, effective 2025, obligates container and cruise terminals across TEN-T core ports to install power supply infrastructure, unlocking an estimated EUR 1.5 billion in planned capital expenditure through 2030 [3].

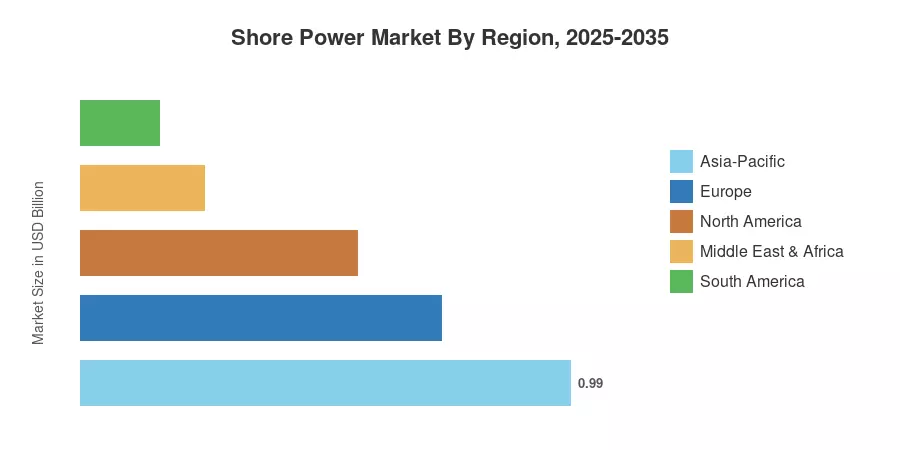

Asia-Pacific commands the largest share of the Shore Power Market at roughly 38.8% of global revenue in 2025, driven by China's aggressive port modernization program and South Korea's green shipping corridor investments. The region also records the fastest growth trajectory at approximately 11.9% CAGR through 2035. Europe holds the second-largest position with around 28.5% share, supported by mandatory cold ironing regulations across Scandinavian and Mediterranean ports. North America follows at 21.7%, with momentum building as federal incentive programs reach the disbursement phase. The Shore Power Market is poised for a decade of sustained double-digit expansion as regulatory tailwinds, renewable energy integration, and rising vessel electrification converge.

Key Report Takeaways

• By Type

- Shoreside installations dominated the Shore Power Market with approximately 72.0% revenue share in 2024, reflecting heavy port-side infrastructure investment globally.

- Ship-side installations are projected to expand at a 15.4% CAGR through 2035 as retrofit mandates compel vessel operators to equip onboard connection systems.

• By Component

- Frequency converters accounted for roughly 38.2% of the Shore Power Market in 2024, critical for bridging 50 Hz/60 Hz grid-to-ship frequency mismatches.

- Transformers are advancing at a 13.5% CAGR, driven by rising voltage requirements of mega-container vessels and cruise ships.

• By Application

- Container vessels captured approximately 38.5% of the Shore Power Market revenue in 2024, reflecting the high volume of container port calls globally.

- Cruise ships represent the fastest-growing application segment at a 14.6% CAGR, propelled by passenger-line sustainability commitments.

• By Region

- Asia-Pacific led the Shore Power Market with 38.8% share in 2025, anchored by port electrification mandates in China, Japan, and South Korea.

- Europe maintains steady momentum with 28.5% share, backed by binding EU at-berth emission rules across TEN-T ports.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model integrates bottom-up port-level installation data, vessel call frequency analysis, government procurement disclosures, and top-down macro energy transition benchmarks. Historical figures (2021–2024) are triangulated against customs data, utility connection permits, and OEM revenue disclosures. Forecast estimates (2026–2035) apply a calibrated compound growth model reflecting policy timelines, vessel fleet renewal cycles, and grid-readiness assessments.