Silica Sand Market Summary

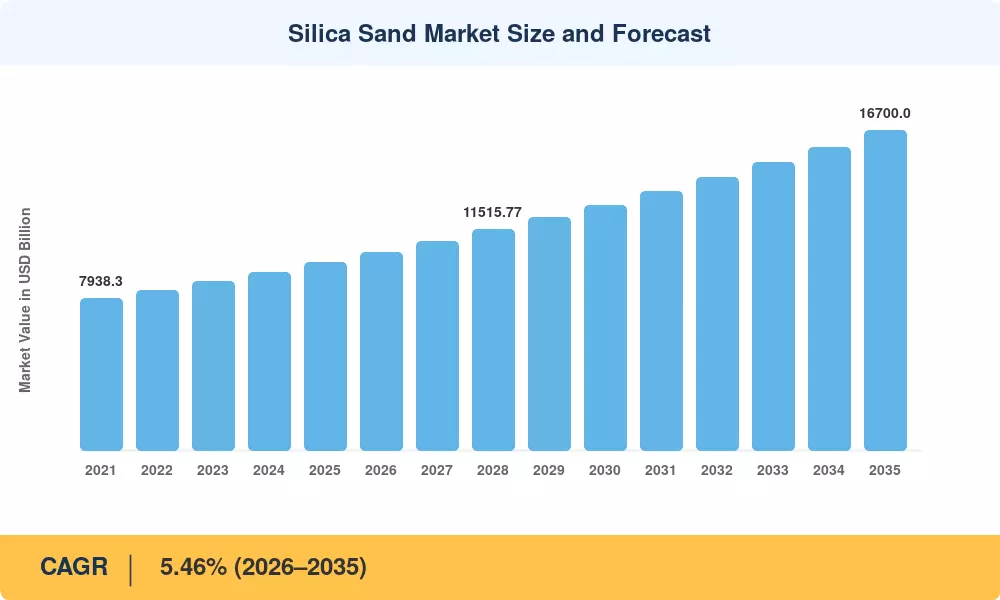

The Silica Sand Market reached an estimated USD 9,820 Million in 2025 and is projected to grow from USD 10,350 Million in 2026 to USD 16,700 Million by 2035, expanding at a CAGR of 5.46% during the forecast period. This sustained growth trajectory is anchored in surging demand for high-purity silica across solar photovoltaic glass production and the continued expansion of hydraulic fracturing operations in North American shale basins. Government-backed infrastructure investment programs — including the U.S. Bipartisan Infrastructure Law and China's 14th Five-Year Plan for construction materials — are channeling billions into projects that consume industrial silica at scale [1][2].

The supply chain of the Silica Sand Market is undergoing a modest but dramatic transition. Traditional open-pit extraction processes are being replaced by precision-processed quartz sand products that fulfill semiconductor-grade purity criteria. The worldwide semiconductor fabrication buildout, supported by more than USD 380 billion in announced fab investments through 2030 [3], is driving foundry sand materials and specialty sand products into all-new performance tiers. Dust-mitigation technology, automated sorting and real-time traceability systems are now baseline requirements for producers selling to electronics and solar glass buyers.

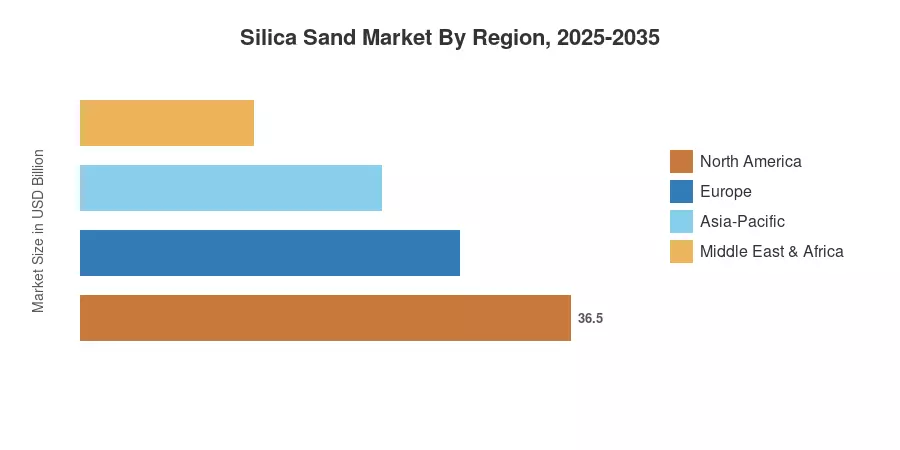

The Asia-Pacific holds the highest share of the Silica Sand Market at approximately 43.4% of 2025 revenue, due to the demand for sand in glass manufacture in China and the construction boom in India. The region also stands first in terms of fastest expanding geography with a predicted CAGR of 5.78% through 2035. North America is in the second position with around 28% share due to strong demand for frac sand materials in the Permian and Appalachian basins With decarbonization deadlines being drawn closer, silicon-intensive clean energy supply chains will keep the Silica Sand Market on a growth path well into the next decade.

Key Report Takeaways

• By Purity Level

- Standard-grade silica (95–99.5% SiO₂) accounted for approximately 51.3% of the Silica Sand Market share in 2025, reflecting broad use in construction silica sand and glass manufacturing sand applications

- High-purity grades (>99.5% SiO₂) are advancing at a 6.74% CAGR through 2035, driven by semiconductor wafer and solar glass specifications

• By End-User Industry

- Oil and gas represented roughly 38.8% of the Silica Sand Market in 2025, underscoring the importance of frac sand materials in unconventional well completions

- Chemical production is projected to expand at a 5.76% CAGR to 2035, fueled by rising demand for industrial silica in specialty chemicals and catalysts

- Glass manufacturing remains the second-largest end-user, consuming over 22% of total volume

• By Region

- Asia-Pacific captured 43.4% of the Silica Sand Market revenue in 2025 and leads all regions in growth velocity

- North America's share of roughly 28% is sustained by the shale oil ecosystem and in-basin mine expansions

- Europe holds an estimated 18% share, with growth centered on solar glass facilities in Germany and Spain

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) projections are based on a combination of bottom-up producer shipment data and customs-level trade flow analysis, with top-down demand modeling calibrated to macroeconomic factors. Historical statistics (2021-2024) are reported actuals. 2025 is the base-year estimate. 2026-2035 figures are anticipated using the calibrated 5.46% CAGR with modifications for cyclical demand trends.