Warehouse Robotics Market Summary

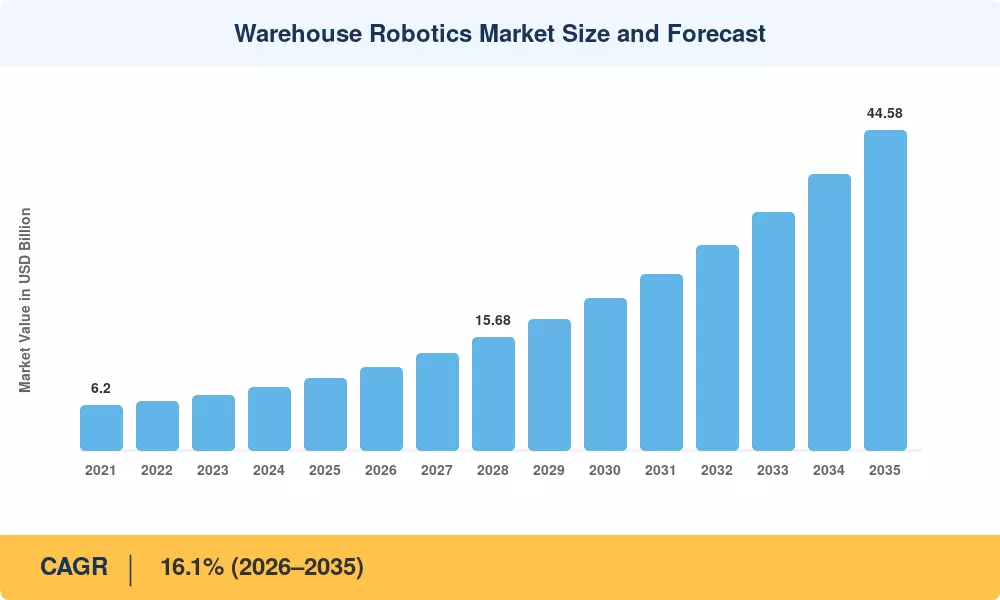

The Warehouse Robotics Market reached USD 10.02 billion in 2025, and Market Research Future (MRFR) projects it will grow from USD 11.63 billion in 2026 to USD 44.58 billion by 2035, registering a compound annual growth rate of 16.1% across the forecast window. Two forces are compressing fulfillment timelines simultaneously: tightening labor availability across OECD economies and same-day-delivery commitments that retailers can no longer walk back. Those pressures have pushed capital budgets toward autonomous mobile robots, automated storage and retrieval systems, and robotic picking cells at a pace that would have been unimaginable five years ago [1][2].

The technical narrative in the Warehouse Robotics Market is about fast displacement. Traditional fixed conveyor layouts geared for dependable pallet-in-pallet-out operations are giving way to flexible, software-orchestrated fleets that can be altered overnight. With new developments in computer vision, robotic arms can now pick up irregular and deformable materials, opening up use cases that were only possible manually before 2022. In December 2024, Zebra Technologies highlighted the rate of change with the acquisition of Photoneo for $350 million to bring 3-D vision IP in-house [3].

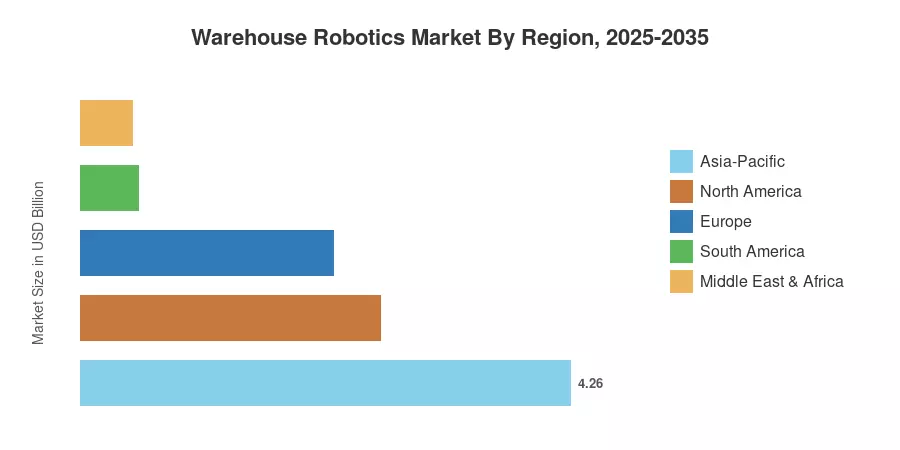

The Asia-Pacific region contributes to over 42.5% of the worldwide Warehouse Robotics Market, with China seeing a 44% jump in new warehouse robot installations in 2024 alone [1]. In North America, the second position is around 26% share, supported by investments in retailer and third-party logistics automation. In Europe, the pace is slower, at roughly 22%, with labour shortages in Germany, the UK and the Nordics driving faster adoption. By 2035, fleet orchestration, based on edge-AI and energy-efficient robotic architectures, will progressively set the course of the warehouse robotics market.

Key Report Takeaways

• By Product Type

- Industrial robots held a 36.3% revenue share of the Warehouse Robotics Market in 2025, reflecting entrenched adoption in palletizing and heavy-goods handling.

- Mobile robots are projected to expand at a 19.4% CAGR through 2035, outpacing every other product category as flexible navigation gains ground.

• By Function

- Storage commanded a 41.0% share of the Warehouse Robotics Market in 2025, anchored by automated storage and retrieval system deployments.

- Picking and sorting is the fastest-growing function at a projected 19.5% CAGR, driven by SKU proliferation in e-commerce.

• By Component

- Hardware captured 75.0% of the Warehouse Robotics Market in 2025, covering robotic arms, autonomous vehicles, and sensor arrays.

- Software is forecast to register a 16.9% CAGR as fleet-orchestration and warehouse-execution platforms gain traction.

• By End-User Industry

- Retail and e-commerce accounted for 30.4% of the Warehouse Robotics Market revenue in 2025.

- Automotive shows the highest projected CAGR at 19.2% through 2035, linked to just-in-time parts-kitting robotics.

• By Geography

- Asia-Pacific held 42.5% share of the Warehouse Robotics Market in 2025 and continues to lead shipment volumes.

- North America remains the second-largest region, with approximately USD 2.61 billion in 2025 revenue.

Warehouse Robotics Market Size and Forecast (2021–2035)

Market sizing approach includes a bottom-up revenue study of robot OEMs, integrators and software platform providers, cross-referenced with top-down industry shipment data from the International Federation of Robotics and proprietary primary interviews. Historical statistics (2021-2024) are checked using company filings and customs trade databases. Forecast numbers (2026-2035) are based on the calibrated 16.1% CAGR and adjusted for the maturation of adoption curves after 2031.