産業オートメーションサービス市場の概要

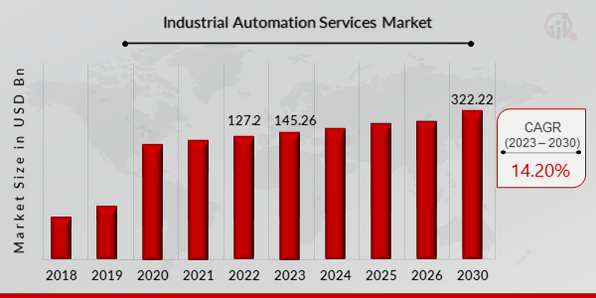

p産業オートメーションサービス市場規模は、2022年に1,272億米ドルと評価されました。産業オートメーションサービス市場業界は、2023年の1,452.6億米ドルから2030年には3,222.2億米ドルに成長すると予測されており、予測期間(2023~2030年)中に14.20%の複合年間成長率(CAGR)を示します。世界中の製造業における自動化とスマート製造の導入の増加、そして新しいビジネス戦略の開発と製造業のコアコンピテンシーの向上の必要性は、市場の成長を促進する産業オートメーションサービス市場の主要な推進力です。図1:産業オートメーションサービス市場、2018年 - 2030年(10億米ドル)

出典:二次調査、一次調査、MRFRデータベース、アナリストレビュー

産業オートメーションサービス市場の動向

p産業オートメーションに対する業界の需要が高まり、産業オートメーションサービス市場の成長を牽引しています。産業オートメーションサービス市場の市場CAGRは、製造業における産業オートメーションの需要の高まり。スループットの向上とコスト削減のニーズが高まるにつれ、メーカーは効率性を高めるためにオートメーションとインダストリー4.0ソリューションを導入するようになりました。オートメーションは、かつて人間が行っていた作業を機械が行うことと同義語となっています。この技術には、様々なプロセスを実行するようにプログラムされた電気機械システムが含まれます。オートメーションが進歩し、製造業に影響を与え続けるにつれて、メーカーは材料、サプライチェーン、生産、配送を追跡するデジタルシステムの構築を目指しています。精度と一貫性を確保し、業務効率を向上させるためにオートメーションを活用するメーカーが増えています。

さらに、世界中の多くの企業が産業分野でロボットを導入しています。今後10年間で、ロボット工学は人工知能やその他の技術革新(より優れたマシンビジョンやセンサーなど)の統合により、価格と性能が大幅に向上するでしょう。ロボットは様々な手作業を人間よりも効率的かつ正確に実行できるため、今日の生産性向上に不可欠なツールと考えられています。ロボットは製造業で最も多く導入されており、手作業をより効率的に実行しています。人工知能(AI)の導入により、ロボットはより安価で柔軟性が高く、自律的になっています。ロボットの中には人間の作業員に代わるものもあれば、人間を補完する協働ロボット(コボット)のように、人間と連携して使用されるものもあります。

例えば、テトラパックの倉庫は2019年7月、DHL International GmbHのデジタルツインに基づくサプライチェーンソリューションと統合されました。これは、サプライチェーン全体にわたって、拡張性、費用対効果、俊敏性に富んだオペレーションを促進するのに役立ちます。輸送車両には、デジタルツインを作成するためのモノのインターネット(IoT)技術が搭載されています。これにより、食品や飲料などの必需品の輸送中の安全が確保されます。今後数年間の自動化ソリューションの需要の高まりは、デジタルツイン技術の採用に貢献しています。したがって、産業オートメーションサービス市場の収益を押し上げます。

産業オートメーションサービス市場セグメントの洞察

h4産業オートメーションサービスソリューションの洞察 pソリューションに基づく産業オートメーションサービス市場のセグメンテーションには、プログラマブルロジックコントローラー(PLC)、監視制御およびデータ収集(SCADA)、分散制御システム、製造実行システム(MES)、製品ライフサイクル管理(PLM)、機能安全、およびプラント資産管理(PAM)が含まれます。分散制御システムセグメントは産業オートメーションサービス市場を支配し、産業オートメーションサービス市場の収益の34.4%を占めています。産業界による IIOT の採用が急速に進んでいるため、自動制御システムの人気が高まり、DCS 市場の成長を牽引しています。産業オートメーション サービスのサービス分析

pサービスに基づく産業オートメーション サービスの市場区分には、コンサルティング サービス、システム統合、専門サービス、技術トレーニングなどが含まれます。コンサルティング サービスのカテゴリは、治療、緩和ケア、リハビリテーション、治癒ケアなど、患者の健康問題の治療に関する相談やサービスの提供により、最も高い収益 (31.5%) を生み出しました。自動化と制御により、運用コストが削減され、サプライ チェーンのエラーが削減され、顧客サービスが向上し、結果として患者ケアの向上につながります。産業オートメーション サービスのアプリケーション分析

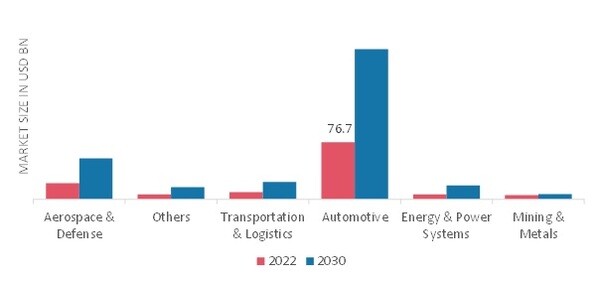

pアプリケーションに基づく産業オートメーション サービスの市場データには、航空宇宙および防衛、その他、輸送および物流の自動化、エネルギーおよび電力システム、鉱業および金属が含まれます。自動車セグメントは産業オートメーションサービス市場の大部分を占め、市場収益の35%(784.8億ドル)を占めました。従来型車両から代替燃料車への買い替えを選択する人が増えるにつれ、自動車業界はさらなる成長が見込まれています。多くの自動車メーカーの生産設備は、精度と効率性を維持するために自動化されています。さらに、従来型車両からEVへの買い替えのトレンドの高まりも、業界の需要をさらに押し上げるでしょう。図2:産業オートメーションサービス市場(アプリケーション別、2022年および2023年) 2030 年 (10 億米ドル)

出典: 二次調査、一次調査、MRFR データベースおよびアナリスト レビュー

産業オートメーション サービス地域別洞察

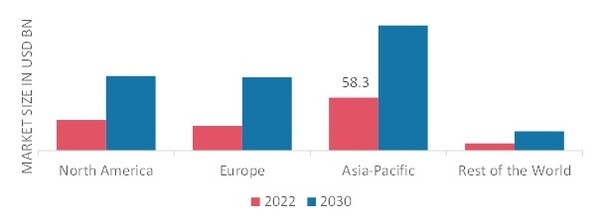

p地域別に、この調査では、北米、ヨーロッパ、アジア太平洋、その他の世界の市場洞察を提供しています。アジア太平洋地域の産業オートメーション サービス市場は、さまざまな産業分野でプロセス効率の向上と生産コストの削減への重点が高まっているため、産業オートメーション サービス市場の大部分を占めることになります。デジタル化に向けた政府の取り組みの数、職場の安全に対する要求の高まり、産業プロセスの効率性の向上など、いくつかの要因が地域経済に影響を与えています。アジア太平洋地域の産業オートメーションサービス市場における主要な収益源は中国です。さらに、産業オートメーションサービス市場レポートで調査された主要国は、米国、カナダ、ドイツ、フランス、英国、イタリア、スペイン、中国、日本、インド、オーストラリア、韓国、ブラジルです。

図3:産業オートメーションサービス市場シェア(地域別)2022年(%)

出典:二次調査、一次調査、 MRFRデータベースおよびアナリストレビュー

北米の産業オートメーションサービス市場は、競争の激化とエンドユーザーの期待により、2番目に大きな市場シェアを占めています。この地域の製造ユニットは、最新の技術革新とデジタルトランスフォーメーション機能を導入して、ビジネスプロセスをより効率的かつ効果的にしています。さらに、米国の産業オートメーションサービス市場は最大の市場シェアを占め、カナダの産業オートメーションサービス市場は北米地域で最も急速に成長している市場でした。

ヨーロッパの産業オートメーションサービス市場は、2023年から2030年にかけて最も高いCAGRで成長すると予想されています。国際ロボット連盟(IFR)によると、2021年1月時点で、西ヨーロッパと北欧諸国のロボット密度は世界で最も高かったとのことです。さらに、ドイツの産業オートメーションサービス市場は最大の市場シェアを占め、英国の産業オートメーションサービス市場はヨーロッパ地域で最も急速に成長している市場でした。

たとえば、新しいサービスおよび資産ライフサイクル管理ソリューションの一環として、シーメンスAGはSAP SEとのパートナーシップを拡大しました。このパートナーシップは、デジタルツインとリモート状態監視を通じて、工場現場の業務、製品開発、リモート状態監視を結び付けることで、資産ライフサイクル全体にわたるコラボレーションを促進することを目指しています。

産業オートメーションサービスの主要市場プレーヤーと競合分析

p主要な市場プレーヤーは、製品ラインの拡大を目指して研究開発に多額の投資を行っており、これが産業オートメーションサービス市場のさらなる成長に貢献するでしょう。市場参加者はまた、新製品の発売、契約上の合意、合併や買収、投資の増加、他の組織とのコラボレーションなど、重要な市場動向を踏まえ、世界的な展開を拡大するためのさまざまな戦略的活動を行っています。産業オートメーションサービス業界は、競争が激化し成長著しい市場環境で拡大し、生き残るために、費用対効果の高い製品を提供する必要があります。現地で製造を行い運用コストを最小限に抑えることは、世界の産業オートメーションサービス業界でメーカーが顧客に利益をもたらし、市場セクターを拡大するために使用する重要なビジネス戦術の1つです。近年、産業オートメーションサービス業界は、製造業に最も重要な利点のいくつかを提供してきました。産業オートメーションサービス市場の主要企業には、シーメンスAG(ドイツ)、ABB Ltd.(スイス)、ジョンソンコントロールズ(アイルランド)、ゼネラル・エレクトリック・カンパニー(米国)、シュナイダーエレクトリックSE(フランス)、ハネウェル・インターナショナル(米国)、三菱電機(日本)、横河電機(日本)、ロックウェル・オートメーション(米国)、アメテック(米国)などがあります。

ABBグループは、電力およびオートメーション技術を提供しています。電力製品に加えて、同社は電力システム、オートメーション製品、プロセスオートメーション、ロボット工学も製造しています。2021年3月、ABBはSCADAシステムの一部として、太陽光発電所の効率を向上させるオートメーション制御ソリューションを開発し、発電所のオペレーターが太陽光発電プロジェクトに関する関連データを容易に監視および分析できるようにしました。

ロックウェル・オートメーション・インド・プライベート・リミテッド社は2001年に設立されました。同社は、アンテナ、スイッチ、導波管など、さまざまな電子部品を製造しています。 2020年11月、ロックウェル・オートメーションはLifecycleIQサービスを通じて、デジタル技術の力と専門家の知識を融合させ、革新的なパートナーシップを締結しました。このサービスにより、企業はビジネスサイクルのあらゆる段階で、より迅速、スマート、そして俊敏に業務を遂行できるようになります。また、グリーンフィールド施設とブラウンフィールド施設の両方において、設計、運用、保守の各段階において、運用と保守を連携させることで、メリットを享受できます。

産業オートメーションサービス市場の主要企業

ul - Johnson Controls Inc. (アイルランド)

- Schneider Electric SE (フランス)

- General Electric Company (米国)

- Rockwell Automation Inc. (米国)

h3産業オートメーションサービス業界の動向 pシュナイダーエレクトリックと米国の水道サービス会社Suezは、水循環管理のための新たなデジタルソリューションを提供する合弁会社を設立しました。この合弁会社は、EcoStruxureとSUEZの水事業における技術的専門知識を組み合わせる予定です。さらに、業界のプレーヤーは、輸送、鉱業、金属、航空宇宙、防衛に適用できるように自動化制御システムを強化しています。2021年2月、ABBはGoFaおよびSWIFTIコボットの協働ロボットポートフォリオを発表しました。これらの協働ロボットは大容量で、ロボットの動きを容易にします。

2020年11月、ロックウェル・オートメーションは、資産管理ソフトウェアの新しいリリースであるFactory Talk Asset Centre Softwareをリリースしました。この新しく開発されたソフトウェアは、ワークフローと管理を容易にし、新しいデバイスの開発も容易にします。

2020年10月、横河電機は、ソフトウェアの開発バージョンであるPlant Resource Manager(PRM)を発表しました。プラントの状態基準保全は、データ管理に関与する製造装置と機器の両方を検出できるこれらのタイプのソフトウェアによってサポートされています。

ABBはScaniaと提携し、スウェーデンに拠点を置くScaniaの新しく自動化されたバッテリー組立工場に、幅広いロボット技術を提供しています。これは、スカニアの大型トラック電動化に向けた大きな一歩でもあります。ABBロボット、IRB 390、IRB 4600、IRB 6700は、組立工程における生産プロセスを容易にする他の補完機器と組み合わせて使用されます。ABBのIRB 390ロボットがバッテリー製造施設で使用されるのは今回が初めてです。

ロックウェル・オートメーションは、2021年7月にKezzler AS(クラウドベースの製品デジタル化およびトレーサビリティプラットフォーム)に加盟しました。この協業では、クラウドベースのサプライチェーン技術を活用し、メーカーが原材料サプライヤーから販売時点、あるいはそれ以降に至るまで、製品のエンドツーエンドの経路を追跡できるようにすることを目指しています。この統合ソリューションは、健康科学、食品・飲料、消費財などの業界において、製品の品質、安全性、持続可能性に関する規制要件や消費者の期待を満たすことに関心を持つお客様に最適です。

産業オートメーションサービス市場のセグメンテーション

h4産業オートメーションサービスソリューションの展望 ul h4産業オートメーションサービス:サービス展望 ul h4産業オートメーションサービス:アプリケーションの展望 ul h4産業オートメーション サービスの地域別見通し ul

産業オートメーションサービス市場は、2035年までに714.73 USDビリオンの評価に達すると予測されています。

2024年、産業オートメーションサービス市場の市場評価は165.89 USD億でした。

2025年から2035年の予測期間中の産業オートメーションサービス市場の期待CAGRは14.2%です。

産業オートメーションサービス市場の主要プレーヤーには、シーメンス、ロックウェル・オートメーション、シュナイダーエレクトリック、ハネウェル、ABB、エマーソン・エレクトリック、三菱電機、横河電機、ゼネラル・エレクトリックが含まれます。

産業オートメーションサービス市場の主なセグメントには、ソリューション、サービス、およびアプリケーションが含まれます。

2024年のプラント資産管理(PAM)セグメントの価値は488.9億USDでした。

製造実行システム(MES)セグメントは、2035年までに800億USDに成長すると予測されています。

著者

Ankit Gupta is a seasoned market intelligence and strategic research professional with over six plus years of experience in the ICT and Semiconductor industries. With academic roots in Telecom, Marketing, and Electronics, he blends technical insight with business strategy. Ankit has led 200+ projects, including work for Fortune 500 clients like Microsoft and Rio Tinto, covering market sizing, tech forecasting, and go-to-market strategies. Known for bridging engineering and enterprise decision-making, his insights support growth, innovation, and investment planning across diverse technology markets.

read more