Acute Coronary Syndrome Market Summary

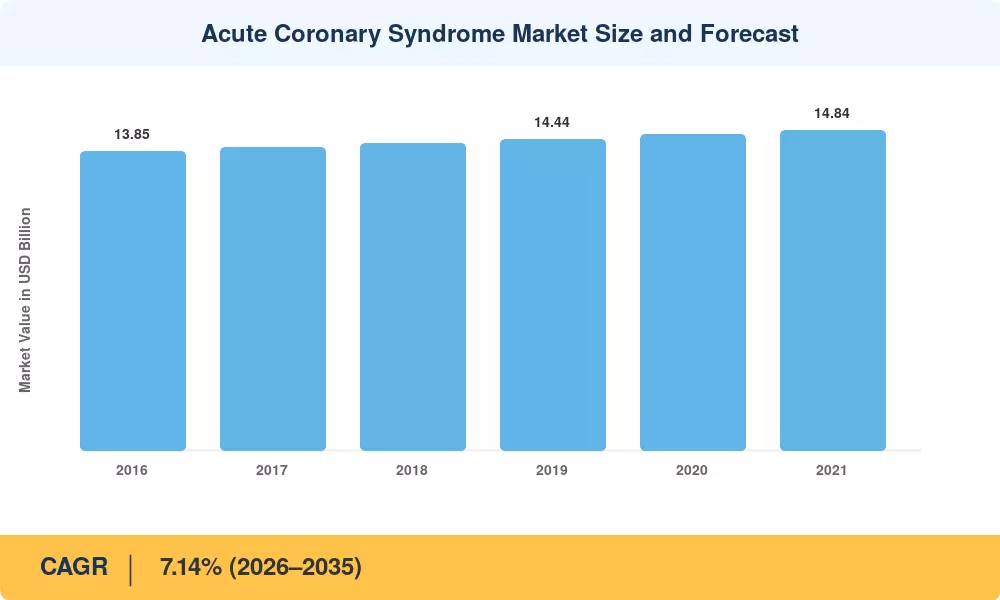

The Global Acute Coronary Syndrome Market size was valued at USD 13.85 Billion in 2025, and the market is projected to grow from USD 14.84 Billion in 2026 to USD 27.61 Billion by 2035, registering a CAGR of 7.14% during the forecast period 2026–2035. Two catalysts anchor that trajectory: the WHO Global Hearts Initiative, which has channeled over USD 1.2 Billion into cardiovascular care infrastructure since 2016 [2], and updated ACC/AHA chest-pain evaluation guidelines that mandate high-sensitivity troponin testing at first contact, broadening the treatment-eligible population [3]. Heart attack treatment drugs continue to absorb the largest share of therapeutic spending, and regulatory fast-tracks for next-generation P2Y12 inhibitors keep the pipeline commercially attractive.

Legacy thrombolytic-only protocols are giving way to integrated percutaneous coronary intervention (PCI) pathways paired with prolonged antiplatelet ACS treatment regimens. A 2024 Lancet analysis estimated that early invasive strategies reduce 12-month mortality by 22% compared with conservative management, reinforcing health-system willingness to invest in drug-eluting stents and catheterization lab expansion [4]. ACS cardiac medications — spanning ticagrelor, prasugrel, and emerging factor-XI inhibitors — now represent the fastest-evolving pharmacological category within cardiovascular therapeutics.

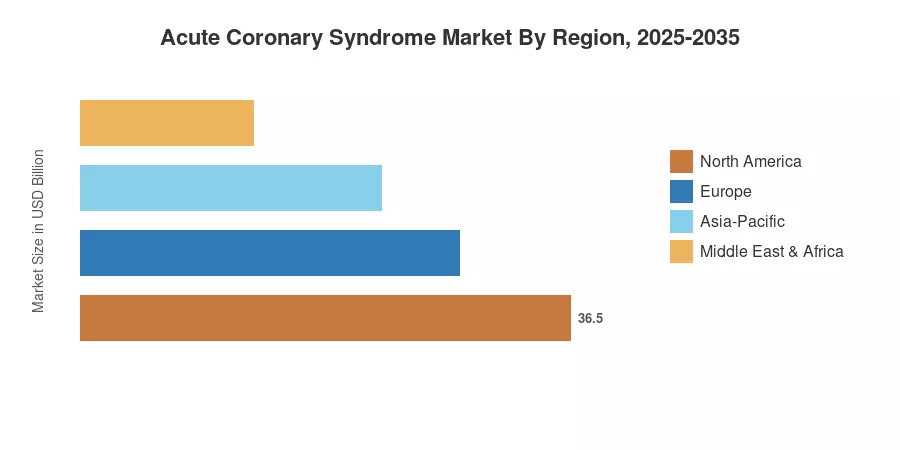

North America commands roughly 41.5% of the Acute Coronary Syndrome Market, underpinned by dense catheterization networks and premium reimbursement. Asia-Pacific is the fastest-growing region at an estimated 9.06% CAGR, driven by coronary artery syndrome management scale-up across China and India. Europe holds the second-largest share at approximately 27.3%, supported by ESC guideline harmonization and cross-border STEMI referral networks [5]. These dynamics position the Acute Coronary Syndrome Market for sustained double-digit absolute growth through 2035.

Key Report Takeaways

• By Condition Type

- Non-ST-elevation myocardial infarction (NSTEMI) captured an estimated 42.3% of the Acute Coronary Syndrome Market in 2024, reflecting widespread adoption of troponin-guided risk stratification

- ST-elevation myocardial infarction (STEMI) is forecast to advance at an 11.18% CAGR through 2035, propelled by hub-and-spoke reperfusion networks expanding across emerging economies

- Unstable angina therapy protocols continue to influence roughly a quarter of the addressable patient pool, though the segment grows at a moderate pace as diagnostic reclassification shifts borderline cases into NSTEMI

• By Treatment

- Medications — including antiplatelet ACS treatment and anticoagulants — held a 47.5% share of the Acute Coronary Syndrome Market in 2024

- Interventional modalities are expanding at an 11.49% CAGR, outpacing pharmacotherapy as PCI infrastructure proliferates globally

• By End User

- Hospitals accounted for 74.2% of revenue in the Acute Coronary Syndrome Market during 2024, reflecting emergency-department-driven diagnosis

- Ambulatory surgical centers are the fastest-growing end-user segment at a 9.13% CAGR, supported by outpatient PCI approvals in the US and EU

• By Region

- North America led the Acute Coronary Syndrome Market with 41.5% revenue share in 2024

- Asia-Pacific is forecast to register the highest regional CAGR at 9.06% through 2035

Market Size and Forecast (2021–2035)

MRFR derives historical values from audited company revenues, payer claims databases, and WHO cardiovascular expenditure reports. Forecast projections use a bottom-up model calibrated against epidemiological incidence rates, procedural volume trends, and anticipated regulatory milestones.

.webp?v=1782976095)