Application Release Automation Market Summary

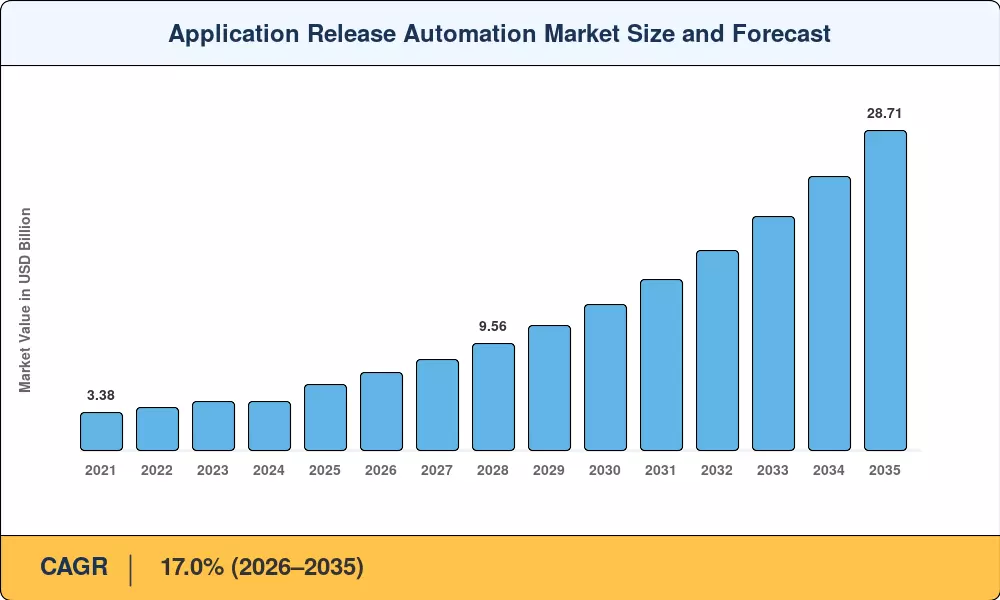

The Application Release Automation Market reached USD 5.92 billion in 2025 and is projected to climb from USD 6.98 billion in 2026 to USD 28.71 billion by 2035, expanding at a 17.0% CAGR during 2026–2035. CIO-level mandates across Fortune 500 companies now require pipeline-as-code governance as a compliance baseline, and over 78% of enterprises with more than 5,000 employees had active release automation budgets by year-end 2024 [1]. Federal cybersecurity executive orders in the United States and the EU Cyber Resilience Act both enforce software bill of materials (SBOM) traceability, channeling procurement dollars toward platforms that embed compliance into every deployment cycle [2].

A visible technology shift is underway inside the Application Release Automation Market as organizations retire script-heavy manual runbooks and point-solution toolchains in favor of AI-driven, policy-as-code platforms capable of orchestrating tens of thousands of releases annually. GenAI-enabled orchestration engines now cut average deployment windows by 40–60%, according to a 2024 Harness benchmark study in which United Airlines accelerated deployments by 75% after migrating to a unified release platform [3]. Enterprise spending on multi-cloud microservice coordination surpassed USD 2.1 billion globally in 2024, reflecting the demand for coordinated releases that span public, private, and on-premises estates [4].

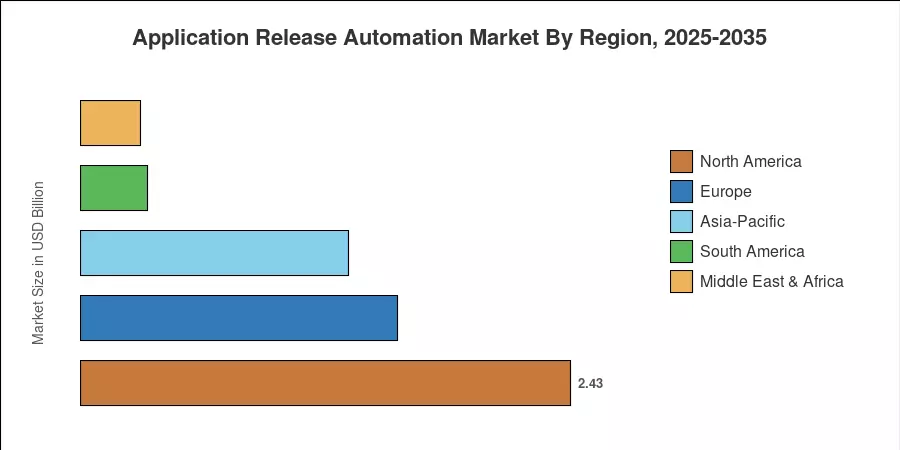

North America commands roughly 41.0% of the Application Release Automation Market, anchored by hyperscaler ecosystems and early DevSecOps adoption among U.S. financial institutions. Asia-Pacific leads growth at a 22.4% CAGR, powered by India's Digital India modernization wave and China's aggressive cloud-native mandates. Europe holds the second-largest share at 26.5%, where DORA (Digital Operational Resilience Act) compliance is pushing banks and insurers to adopt automated release pipelines at pace [5]. The decade ahead will see platform-as-a-product cultures and internal developer portals reshape how the Application Release Automation Market delivers value.

Key Report Takeaways

• By Component

- Tools captured 73.1% of the Application Release Automation Market share in 2025, driven by enterprise demand for integrated CI/CD pipeline management and policy engines.

- Services are projected to expand at a 22.8% CAGR through 2035, reflecting growing investment in implementation consulting, managed release operations, and training programs.

• By Deployment Mode

- Cloud deployments accounted for 63.0% of the Application Release Automation Market in 2025, as SaaS-based orchestration eliminated infrastructure overhead for mid-market buyers.

- Hybrid configurations are projected to grow at a 21.9% CAGR, catering to regulated industries that must keep sensitive workloads on-premises while leveraging cloud-native tooling.

• By Organization Size

- Large enterprises represented 74.2% of the Application Release Automation Market revenue in 2025, reflecting their complex multi-application estates and compliance mandates.

- SMEs are posting the fastest growth at a 23.0% CAGR to 2035 as low-code release platforms reduce adoption barriers.

• By End-User Industry

- IT and telecommunications contributed 30.0% of the Application Release Automation Market revenue in 2025, the largest vertical share.

- BFSI is set to outpace other verticals at a 21.6% CAGR through 2035, fueled by regulatory pressure and real-time digital banking requirements.

• By Region

- North America accounted for 41.0% of the Application Release Automation Market in 2025.

- Asia-Pacific leads growth at 22.4% CAGR, with India and China forming the twin engines of expansion.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary sizing framework combines top-down enterprise software spending analysis with bottom-up vendor revenue aggregation across 35 countries. Historical figures (2021–2024) draw on audited annual reports and IT spending surveys, while the forecast applies scenario-weighted modeling calibrated to macroeconomic and technology adoption trajectories for the Application Release Automation Market.

.webp?v=1784724293)