Cider Market Summary

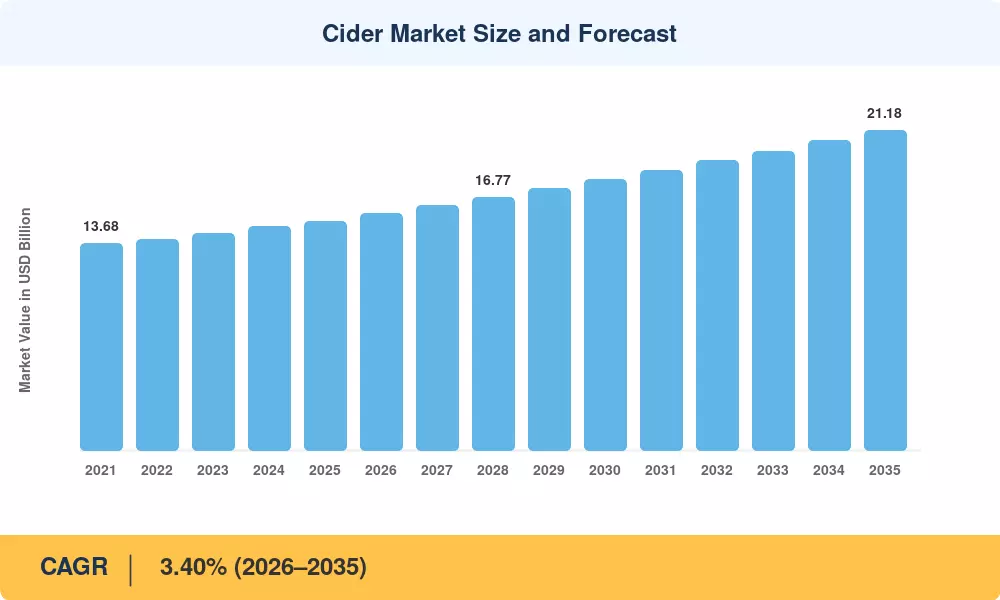

The global Cider Market was valued at USD 15.17 billion in 2025 and is projected to reach USD 15.69 billion in 2026, expanding to USD 21.18 billion by 2035 at a CAGR of 3.40% during the forecast period (2026–2035). This trajectory reflects a structural shift in adult beverage consumption toward lighter, fruit-based alternatives, reinforced by policy-backed moderation campaigns in the EU, Australia, and Canada. Health-awareness spending by public agencies across OECD nations exceeded USD 4.2 billion in combined alcohol-moderation programming between 2022 and 2024, channeling consumer preference toward lower-ABV options where cider holds a natural advantage [1].

The Cider Market is experiencing a category-level transformation. Legacy lager-dominant portfolios are being recalibrated as multinational brewers allocate increasing shelf space and marketing budgets to fruit-based fermented beverages. Heineken's Strongbow rebranding investment alone reached an estimated EUR 120 million across 2023–2025, while Carlsberg committed over EUR 80 million to Somersby line extensions [2]. Canned packaging innovation is displacing traditional glass bottle formats at a pace not seen in the broader beer segment, supported by aluminum sustainability credentials and single-serve convenience.

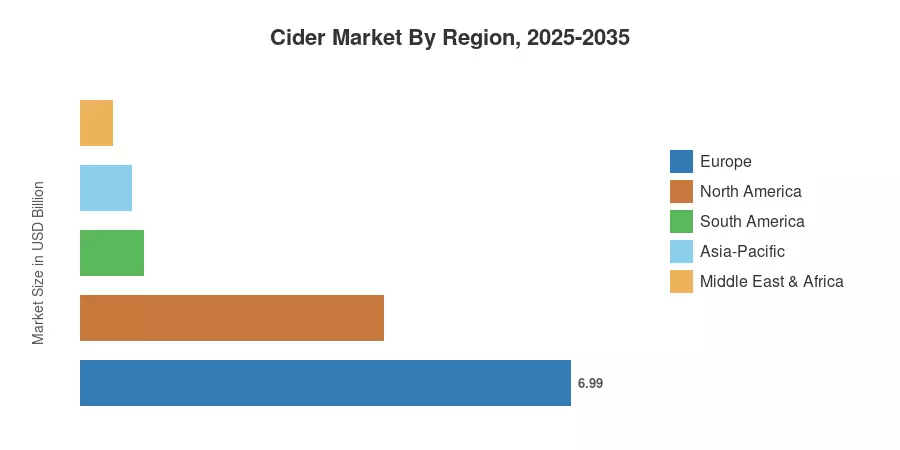

Europe dominates the Cider Market with roughly 46.1% of global revenue in 2025, anchored by deep-rooted consumption traditions in the United Kingdom, France, and Spain. Asia-Pacific is the fastest-growing region, forecast to register a 4.80% CAGR through 2035 as urbanizing middle-class populations in China and India adopt Western-style beverage occasions. North America holds the second-largest share at approximately 28.5%, driven by premiumization in the United States.

Key Report Takeaways

• By Ingredient

- Apple-based variants commanded 56.4% of the Cider Market in 2025, reflecting entrenched orchard supply chains and consumer familiarity.

- Mixed fruit variants are projected to grow at a 3.66% CAGR through 2035, gaining share among younger demographics seeking flavor diversity.

• By Category

- The mass-production segment accounted for a 66.9% share of the Cider Market in 2025.

- Premium offerings are advancing at a 4.37% CAGR.

• By Packaging

- Canned formats are forecast to expand at a 4.14% CAGR, outpacing bottles as single-serve and sustainability preferences converge.

• By Region

- Europe remained the largest regional Cider Market in 2025, generating approximately USD 6.99 billion in revenue.

- Asia-Pacific is projected to achieve the fastest growth with a 4.80% CAGR, driven by rising disposable incomes across China and Southeast Asia.

Cider Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology integrates bottom-up revenue models calibrated against distributor sell-through data, excise tax filings in 42 countries, and cross-validated trade association figures from the European Cider and Fruit Wine Association (AICV), the United States Association of Cider Makers (USACM), and Cider Australia.