CRM Analytics Market Summary

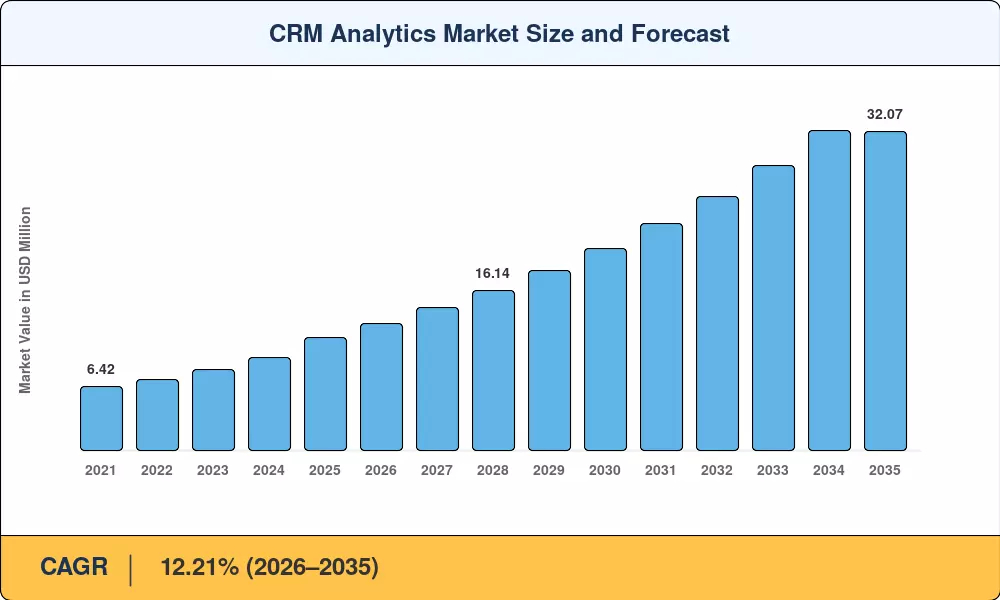

The CRM Analytics Market reached an estimated USD 11.38 billion in 2025 and is projected to expand from USD 12.82 billion in 2026 to USD 32.07 billion by 2035, registering a CAGR of 12.21% across the forecast period. Enterprise investment in AI-driven lead scoring analytics accelerated sharply after the European Commission allocated EUR 4.5 billion to digital transformation programs in 2024, while the U.S. CHIPS and Science Act indirectly boosted analytics infrastructure by expanding domestic cloud capacity [1]. The CRM Analytics Market benefits from a structural shift: organizations no longer treat customer data as a passive archive but as a real-time decisioning asset.

Legacy on-premises CRM deployments — rigid, batch-oriented, and expensive to scale — are giving way to cloud-native platforms embedding customer lifetime value prediction models directly into sales and service workflows. Gartner estimated that 72% of new CRM deployments in 2025 were cloud-first, a figure that reflects both economic logic and the computational demands of large language models powering sales pipeline analytics and forecasting. CRM data visualization dashboards now synthesize voice, text, and clickstream signals in sub-second latency windows, replacing overnight ETL jobs that once delayed insights by 24 hours.

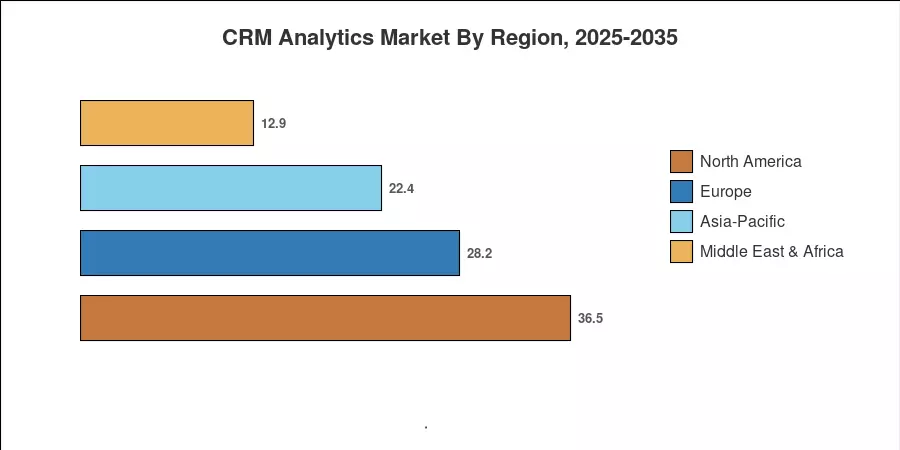

North America commands roughly 34% of CRM Analytics Market revenue, anchored by Salesforce's home-market dominance and deep enterprise budgets. Asia-Pacific is the fastest-growing region at a 14.12% CAGR, propelled by India's Digital India initiative and China's expanding SaaS ecosystem. Europe holds the second-largest share at approximately 27%, where GDPR compliance costs paradoxically stimulate demand for privacy-preserving customer retention analytics for CRM. The convergence of regulatory pressure, AI maturity, and cloud economics positions the CRM Analytics Market for sustained double-digit growth through 2035.

Key Report Takeaways

• By Type

- Sales and marketing analytics represented the dominant type segment in 2025, capturing approximately 44% of CRM Analytics Market revenue, driven by attribution modeling and sales pipeline analytics and forecasting capabilities

- Social media and web analytics is the fastest growing market, advancing at roughly 13.7% CAGR through 2035 as brands embed social listening into customer lifetime value prediction models

• By Deployment

- Cloud deployment represents the dominant deployment segment, accounted for about 68% of CRM Analytics Market share in 2025, reflecting elastic compute needs for AI-driven lead scoring analytics

- SMEs are forecast to grow at approximately 13.1% CAGR as serverless inference and pre-built CRM data visualization dashboards democratize advanced analytics

• By Organization Size

- SMEs are forecast to grow fastest at approximately 13.1% CAGR as serverless inference and pre-built CRM data visualization dashboards democratize advanced analytics

• By End User

- Retail and e-commerce has the largest share, captured roughly USD 3.47 billion in 2025, leveraging customer retention analytics for CRM to reduce cart abandonment

- The CRM Analytics Market in Asia-Pacific is projected to grow at 14.12% CAGR, while North America retained the largest regional share

• By Region

- The CRM Analytics Market in Asia-Pacific is projected to grow fastest at 14.12% CAGR, while North America retains the largest regional share

MRFR's estimates blend top-down macroeconomic modeling with bottom-up vendor-revenue triangulation, validated against disclosed CRM platform revenues and third-party IT spending surveys.