Ferric Chloride Market Summary

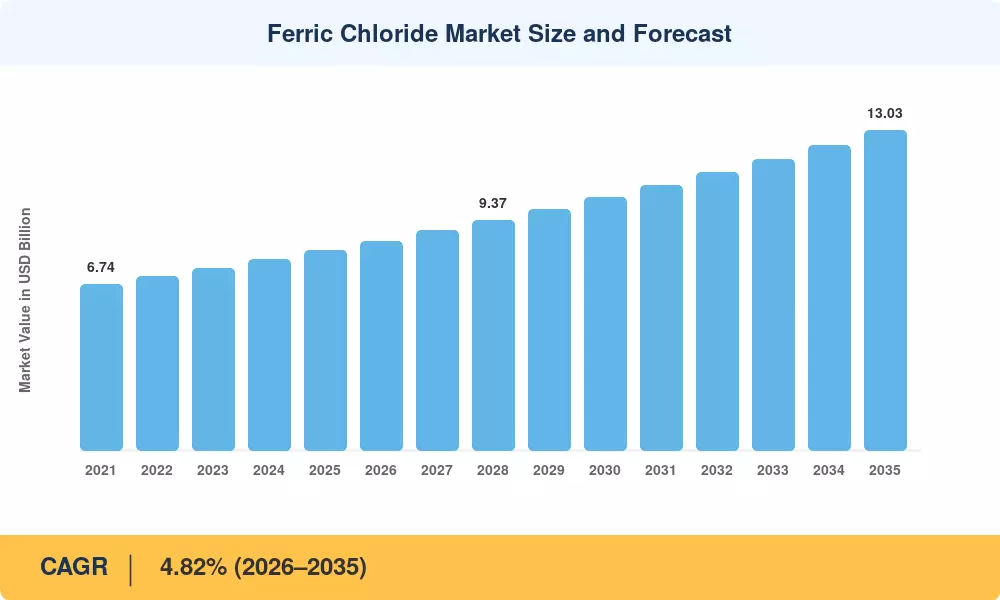

The Ferric Chloride Market reached a valuation of USD 8.14 Billion in 2025, with projections indicating growth from USD 8.53 Billion in 2026 to USD 13.03 Billion by 2035 at a CAGR of 4.82% during the forecast period (2026–2035). Tightening discharge limits under the EU Urban Wastewater Treatment Directive revision and the US EPA's updated Lead and Copper Rule are compelling municipalities to upgrade coagulation systems, directly boosting demand for iron chloride compounds and allied water treatment chemicals [2]. Capital expenditure on municipal sewage infrastructure alone surpassed USD 68 billion globally in 2024, channeling reliable procurement volumes toward established wastewater treatment agents [3].

A significant technology shift is redefining how the Ferric Chloride Market generates value. Legacy aluminum-sulfate-based coagulation is steadily giving way to iron-based industrial coagulants that deliver superior phosphorus removal and lower sludge volumes. China's 14th Five-Year Plan earmarked over USD 52 billion for urban sewage network upgrades, accelerating the substitution toward ferric-chloride-based sewage treatment additives across Tier-2 and Tier-3 cities [4]. Simultaneously, the semiconductor and electronics packaging boom is increasing the consumption of high-purity printed circuit board etchants, as global PCB output value crossed USD 82 billion in 2024 [5].

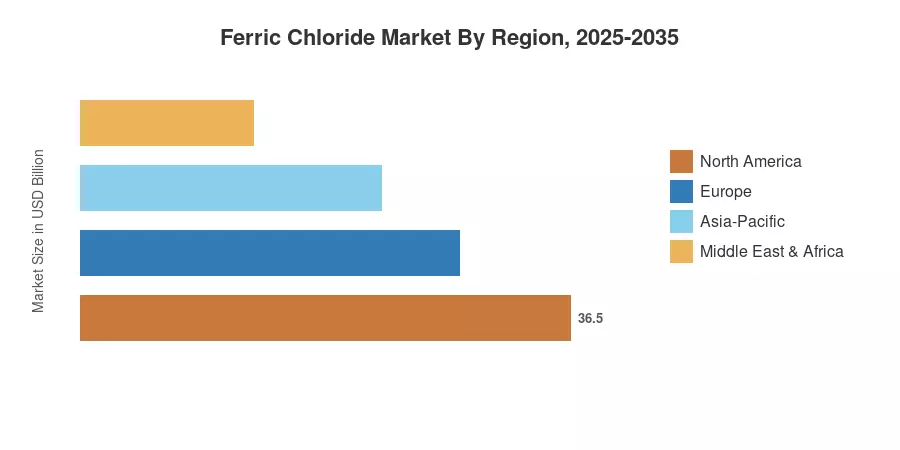

Asia-Pacific commands roughly 48.2% of global Ferric Chloride Market revenue, anchored by China and India's aggressive wastewater infrastructure build-outs. South America is the fastest-growing region at a 5.76% CAGR through 2035, powered by Brazil's Novo Marco do Saneamento mandates requiring universal sewage coverage by 2033 [6]. Europe holds the second-largest share at approximately 18.8%, where stringent nutrient-removal regulations sustain resilient baseline consumption of metal treatment chemicals. The decade ahead will reward suppliers who can straddle both commodity-scale and high-purity segments.

Key Report Takeaways

• By Grade

- Industrial/Technical Grade accounted for 68.0% of the Ferric Chloride Market share in 2025, driven by bulk procurement contracts for municipal water treatment chemicals.

- Electronic Grade is expanding at a 6.12% CAGR through 2035, the fastest pace among all grades, reflecting surging demand for ultra-pure printed circuit board etchants.

- Food and Pharma Grade is projected to reach USD 0.74 billion by 2035, propelled by specialty iron chloride compounds used in nutritional supplementation.

• By Application

- Water and Wastewater Treatment represented 58.5% of the Ferric Chloride Market size in 2025, underscoring the segment's role as the primary consumption channel for industrial coagulants.

- PCB Manufacturing is forecast to grow at a 6.06% CAGR between 2026 and 2035, supported by 5G rollout and advanced packaging demand.

• By Region

- Asia-Pacific contributed approximately 48.2% of the global Ferric Chloride Market revenue in 2025.

- South America leads regional growth at a 5.76% CAGR, with Brazil's sewage modernization serving as the primary catalyst.

Market Size and Forecast (2021–2035)

MRFR's estimates combine bottom-up production volume tracking across 42 countries with top-down cross-validation against trade flow databases, customs data, and manufacturer revenue disclosures.