Intraoral Scanner Market Summary

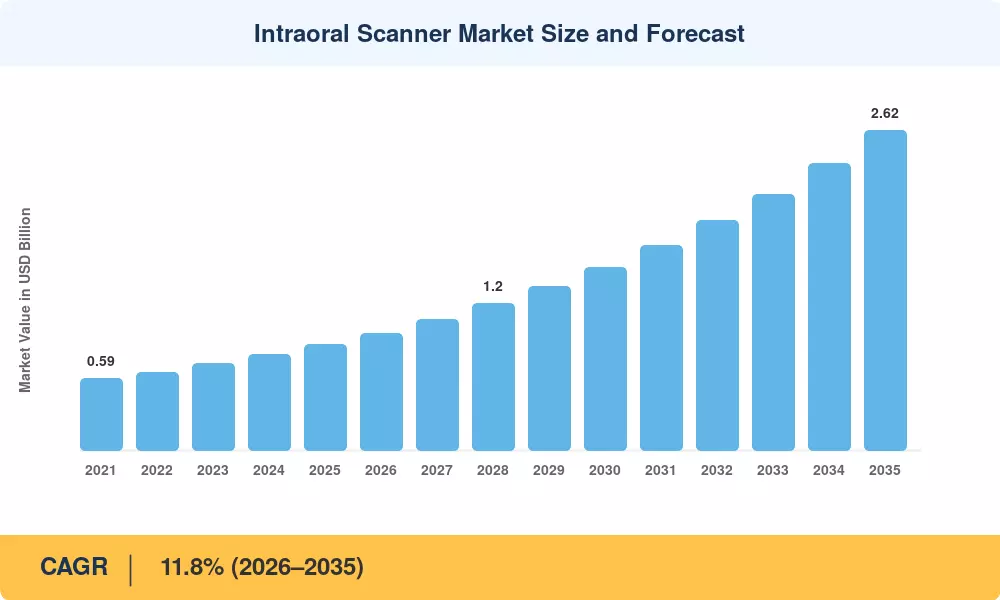

The Intraoral Scanner Market size was valued at USD 0.87 Billion in 2025, and the market is projected to grow from USD 0.96 Billion in 2026 to USD 2.62 Billion by 2035, registering a CAGR of 11.8% during the forecast period 2026–2035. Two catalysts are accelerating this trajectory: rising global expenditure on cosmetic and restorative dentistry — the American Dental Association estimates that U.S. dental spending crossed USD 185 Billion in 2024 [1] — and a wave of insurance-reimbursement reforms in North America and Western Europe that increasingly recognize digital impression codes as standard-of-care procedures [2].

A sweeping technology shift is reshaping how dental professionals capture patient data. Traditional alginate and polyvinyl siloxane impression trays, long criticized for patient discomfort and dimensional instability, are giving way to compact optical wands that generate real-time 3D meshes within seconds. Major device makers invested a combined USD 1.2 Billion in scanner R&D between 2022 and 2024, racing to integrate AI-driven stitching, shade matching, and caries detection directly into the scanning workflow. This convergence of hardware miniaturization and software intelligence is creating a category of chairside dental scanning devices that function as diagnostic hubs rather than simple impression substitutes.

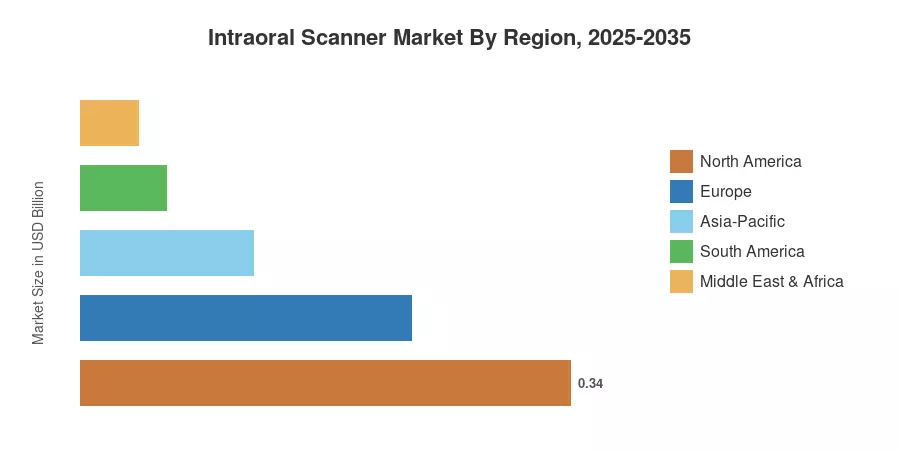

North America commands roughly 39% of the Intraoral Scanner Market, supported by high per-capita dental spending and favorable CDT code reimbursement. Asia-Pacific represents the fastest-growing region at a projected 13.6% CAGR, driven by government-backed digital-health mandates in China and India [4]. Europe holds the second-largest share at approximately 27%, anchored by Germany's strong dental-lab ecosystem. As tele-dentistry platforms expand and scanner price points drop below USD 20,000, adoption among solo practitioners and mobile clinics should intensify through the end of the decade.

Key Report Takeaways

• By Type

- Powder-free scanners captured approximately 80% of the intraoral scanner market revenue in 2025, reflecting clinician preference for streamlined, powder-free capture.

- Powder-based models with approximately 11.5% CAGR persist in budget-sensitive segments and dental-education settings where the lower hardware cost

• By Modality

- Portable handheld units are projected to expand at a 14.0% CAGR through 2035, outpacing cart-based systems as wireless connectivity matures.

- Cart-based scanners remain the workhorse 14.0% 2026-2035 of the Intraoral Scanner Market in hospital and large-practice settings, where a single unit serves multiple operatories via a mobile cart.

• By Application

- Orthodontics accounted for roughly 46% of the Intraoral Scanner Market by application in 2025, driven by direct-to-consumer aligner demand.

• By End User

- Dental clinics are expected to register the fastest end-user CAGR of 14.8% as mid-tier scanners become affordable.

• By Region

- North America retained a 39% share, supported by reimbursement clarity and early technology adoption.

- Asia-Pacific is forecast to grow at a 13.6% CAGR, led by China's Healthy China 2030 digital dentistry allocation.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary sizing framework combines bottom-up revenue tracking from scanner OEMs, dental distributor sell-through data, and top-down cross-referencing with national dental expenditure databases. Historical figures (2021–2024) reflect actual shipment volumes, while the forecast (2026–2035) incorporates regression-adjusted inputs for procedure volume growth, average selling price erosion, and regional adoption curves.