Liquefied Petroleum Gas (LPG) Market Summary

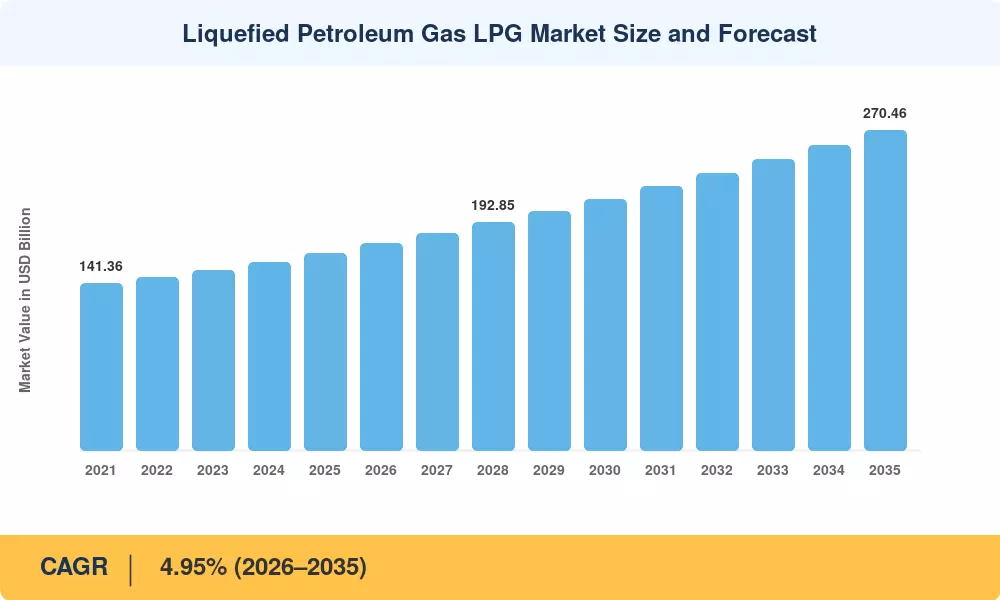

The Liquefied Petroleum Gas Market reached USD 166.82 billion in 2025 and is projected to grow from USD 175.08 billion in 2026 to USD 270.46 billion by 2035, expanding at a CAGR of 4.95% during the forecast period (2026–2035). Two structural catalysts anchor this trajectory: India's Pradhan Mantri Ujjwala Yojana (PMUY) program, which has connected over 104 million below-poverty-line households to clean cooking fuel since 2016 [1], and the rapid scaling of propane dehydrogenation (PDH) capacity across China's eastern seaboard, where cumulative installed capacity exceeded 24 million tonnes by late 2024 [2].

The Liquefied Petroleum Gas Market is undergoing a major change away from conventional refinery-based supply chains. Record shale production in the Permian Basin and improved fractionation infrastructure along the U.S. Gulf Coast [3] have taken natural gas liquids processing to the forefront of upstream production. Meanwhile, bio-LPG has been identified as a feasible decarbonization pathway under the European Union’s revised Renewable Energy Directive (RED III), with biopropane being categorized as an advanced biofuel that can be double-counted towards member state targets [4].

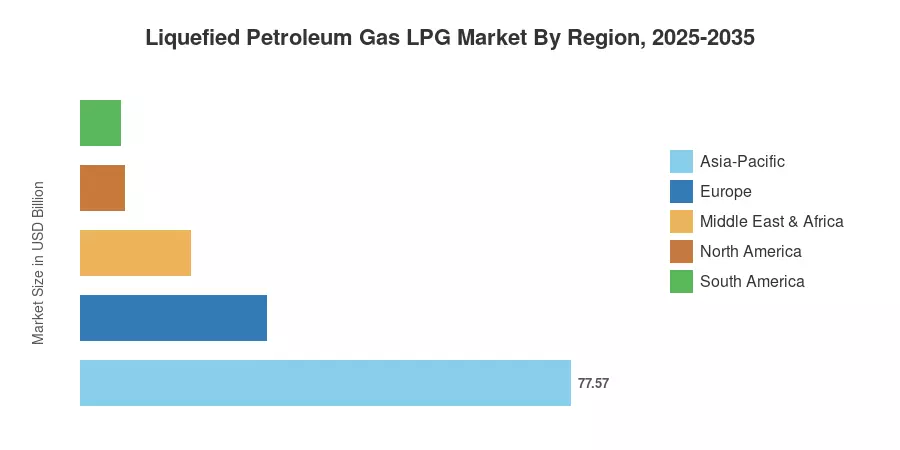

China’s petrochemical demand and India’s rural distribution expansion will drive the Asia-Pacific region to account for 46.5% of the liquefied petroleum gas market revenue in 2025. The primary export hub is North America, with shale volumes moving through Gulf Coast terminals. Europe, the No. 2 consumption region, is turning to renewable blends of propane to meet net-zero objectives. The projection period will see if the supply infrastructure can keep up with downstream demand across all three corridors.

Key Liquefied Petroleum Gas Market Takeaways

By Source of Production

- Natural Gas Liquids held a 55.6% share of the Liquefied Petroleum Gas Market in 2025, reflecting U.S. shale fractionation dominance and Middle Eastern gas-processing expansions.

- Bio-LPG/Renewable Propane is forecast to register the fastest CAGR of 15.8% through 2035, propelled by EU RED III mandates and biorefinery investment cycles.

By Distribution Channel

- Cylinder Gas accounted for 52.8% of the Liquefied Petroleum Gas Market in 2025, driven by decentralized consumption across rural Asia and Sub-Saharan Africa.

- Pipeline and Virtual Pipeline channels are projected to expand at a 9.0% CAGR to 2035 as India, Nigeria, and Brazil invest in last-mile connectivity.

By Application

- Residential and Commercial Cooking/Heating comprised 48.4% of the Liquefied Petroleum Gas Market in 2025, sustained by subsidy programs and urbanization.

- Petrochemical Feedstock is advancing at an 8.3% CAGR during 2026–2035, led by new PDH and steam cracker installations in East Asia.

By Geography

- Asia-Pacific commanded a 46.5% revenue share in 2025 and is expected to post the fastest regional CAGR of 5.8% through 2035.

- North America's export infrastructure expansions continue to shape global pricing benchmarks.

Liquefied Petroleum Gas Market Size and Forecast (2021–2035)

Market Research Future (MRFR) employs its own estimation methodology, which includes the use of national production data (IEA, EIA), customs-level trade information, downstream capacity databases, and primary interviews with terminal operators and distributors. Historical numbers are matched to reported volumes, and the forecast applies an econometric model calibrated to GDP growth, urbanization rates, petrochemical capex cycles and regulatory subsidy trajectories.