Protein Sequencing Market Summary

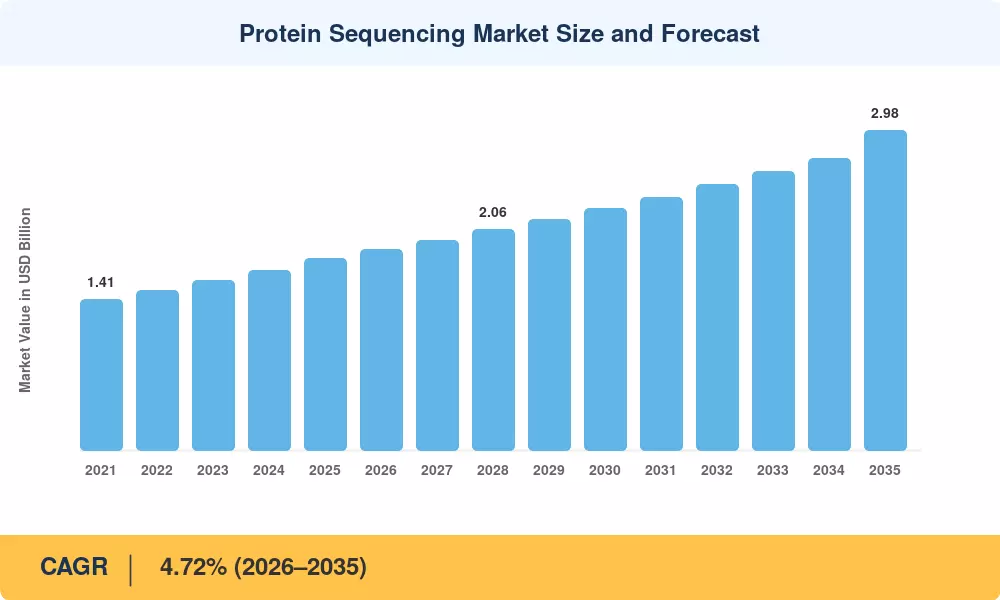

The Protein Sequencing Market reached an estimated USD 1.79 billion in 2025 and is projected to grow from USD 1.87 billion in 2026 to USD 2.98 billion by 2035, registering a CAGR of 4.72% during the forecast period. Rising global spending on precision medicine and the U.S. National Institutes of Health's USD 51 billion annual research budget continue to anchor demand for amino acid sequence analysis across drug discovery pipelines. Pharmaceutical firms increasingly treat peptide sequence determination as a non-negotiable step in biologics development, pushing procurement budgets higher each year.

A technology transformation is reshaping the Protein Sequencing Market as legacy Edman degradation method workflows give way to single-molecule platforms capable of reading proteoforms in real time. Mass spectrometry proteomics remains the workhorse for high-throughput labs, yet next-gen protein identification technologies — including nanopore-based and fluorosequencing systems — attracted over USD 600 million in venture capital between 2022 and 2024 [2]. These platforms bundle instruments with consumable kits and cloud-based analytics, converting one-time hardware sales into recurring revenue.

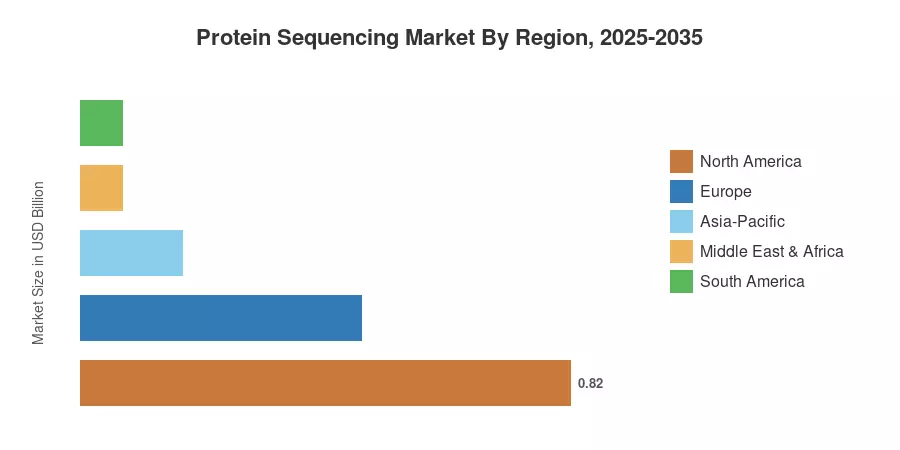

North America commands roughly 46% of the global Protein Sequencing Market revenue, backed by entrenched R&D infrastructure and robust NIH funding cycles Asia-Pacific is the fastest-growing region, advancing at an estimated 9.4% CAGR as Chinese and Indian biopharma investment accelerates. Europe holds the second-largest share at approximately 26%, driven by EMA biosimilar approvals that require rigorous amino acid sequence analysis. The decade ahead will reward vendors who balance instrument innovation with accessible pricing for emerging-market laboratories.

Key Report Takeaways

• By Products & Services

- Software & services held a 41% revenue share of the Protein Sequencing Market in 2025, reflecting the shift toward cloud-based peptide sequence determination platforms

- Reagents & consumables are expanding at a 6.9% CAGR through 2035, fueled by recurring purchase cycles tied to mass spectrometry proteomics workflows

- Instruments generated approximately USD 0.62 billion in 2025 revenue as labs modernize aging Edman degradation method hardware

• By Application

- Biotherapeutics quality control & discovery captured 39% of the Protein Sequencing Market share in 2025

- Synthetic biology & cell-free systems are projected to climb at a 13.1% CAGR to 2035, the fastest among all application segments

• By End User

- Pharmaceutical companies commanded 57% share of the Protein Sequencing Market in 2025

- Contract Research Organizations (CROs) record the fastest end-user CAGR at 9.2% during the forecast period

• By Region

- North America led with a 46% share of the Protein Sequencing Market in 2025

- Asia-Pacific is set to advance at a 9.4% CAGR to 2035, driven by next-gen protein identification adoption in China and India

Protein Sequencing Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework combines bottom-up revenue modeling from instrument, consumable, and service line-items with top-down cross-validation against publicly reported financial data from major vendors. Historical figures (2021–2024) draw on company filings and trade association databases; forecast values (2026–2035) apply segment-level growth assumptions anchored to clinical trial activity, regulatory approvals, and capital expenditure surveys.