Whole Exome Sequencing Market Summary

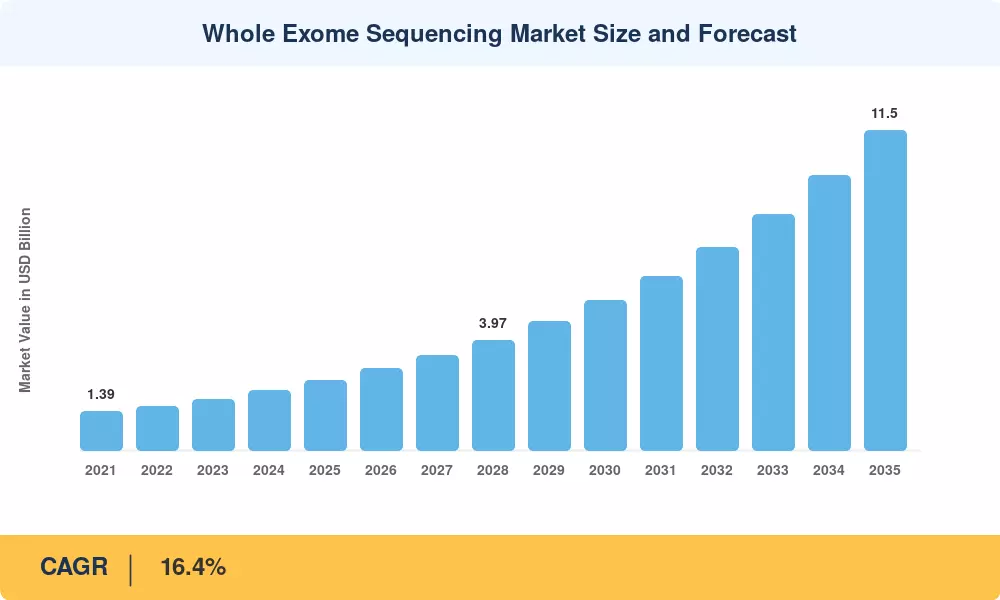

The Whole Exome Sequencing Market size was valued at USD 2.52 Billion in 2025, and the market is projected to grow from USD 2.93 Billion in 2026 to USD 11.50 Billion by 2035, registering a CAGR of 16.4% during the forecast period 2026–2035. This expansion is driven by accelerating adoption of genomic diagnostics in clinical settings and sustained government funding for population-scale genomic programs. The UK Biobank's completion of exome sequencing for over 470,000 participants and the U.S. National Institutes of Health's All of Us Research Program — which has committed over USD 3.1 Billion to precision medicine since inception — are catalyzing both supply-side innovation and demand-side integration [1][2].

A technology transition is reshaping the Whole Exome Sequencing Market as legacy Sanger-based workflows give way to high-throughput, cost-optimized platforms capable of processing thousands of samples weekly. Per-exome sequencing costs have declined from approximately USD 1,000 in 2018 to under USD 350 in 2025, broadening access in community hospitals and mid-tier reference laboratories that previously relied on single-gene panels [3]. Cloud-based bioinformatics pipelines now automate variant calling and clinical annotation, reducing turnaround from weeks to days.

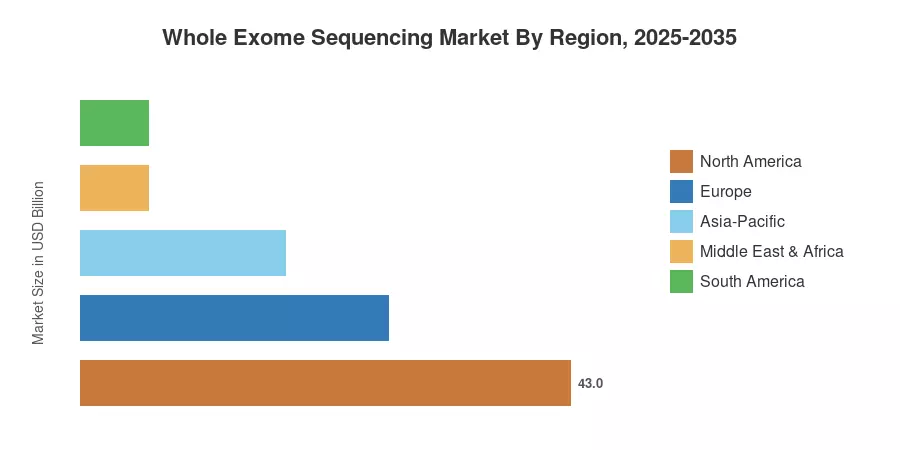

North America commands the largest share of the Whole Exome Sequencing Market at approximately 43%, underpinned by deep payer coverage, an established molecular diagnostics infrastructure, and concentrated R&D spending. Asia-Pacific is the fastest-growing region with a projected CAGR of 19.2%, fueled by China's national genomics strategy and India's expanding laboratory network. Europe holds the second-largest regional position at roughly 27%, anchored by cross-border initiatives such as the European 1+ Million Genomes Initiative [4]. As reimbursement pathways mature in emerging economies, the Whole Exome Sequencing Market is poised for sustained double-digit expansion through 2035.

Key Report Takeaways

• By Product Type

- Services represent the largest product segment in the Whole Exome Sequencing Market, capturing approximately 44% of revenue in 2025, driven by outsourced testing demand from hospitals lacking in-house sequencing capacity.

- Kits are projected to register a CAGR of 17.8% through 2035, reflecting the shift toward decentralized, in-house exome workflows at large academic medical centers.

- Systems account for an estimated USD 0.53 Billion in 2025 as capital equipment refresh cycles accelerate across North American and European reference laboratories.

• By Application

- Diagnostics dominates the Whole Exome Sequencing Market application mix, holding roughly 39% revenue share as clinical adoption expands across rare and undiagnosed disease programs.

- Drug Discovery and Development is growing at the fastest application-level CAGR of 18.3%, supported by pharma investments in target identification and companion diagnostic co-development.

• By Region

- North America generated approximately USD 1.08 Billion in 2025, reinforced by broad Medicare coverage for genomic tests and a dense network of CLIA-certified sequencing laboratories.

- Asia-Pacific is expected to surpass USD 3.10 Billion by 2035, reflecting aggressive government genomics programs in China, Japan, and South Korea.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on primary interviews with laboratory directors, sequencing platform vendors, and payer-side stakeholders, supplemented by analysis of public procurement databases, published clinical study budgets, and company financial disclosures. Historical figures (2021–2024) are triangulated against reagent shipment data and installed-base surveys; forecast projections (2026–2035) apply a validated bottom-up model anchored to test volume growth, average selling price trajectories, and regional reimbursement expansion timelines.