Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

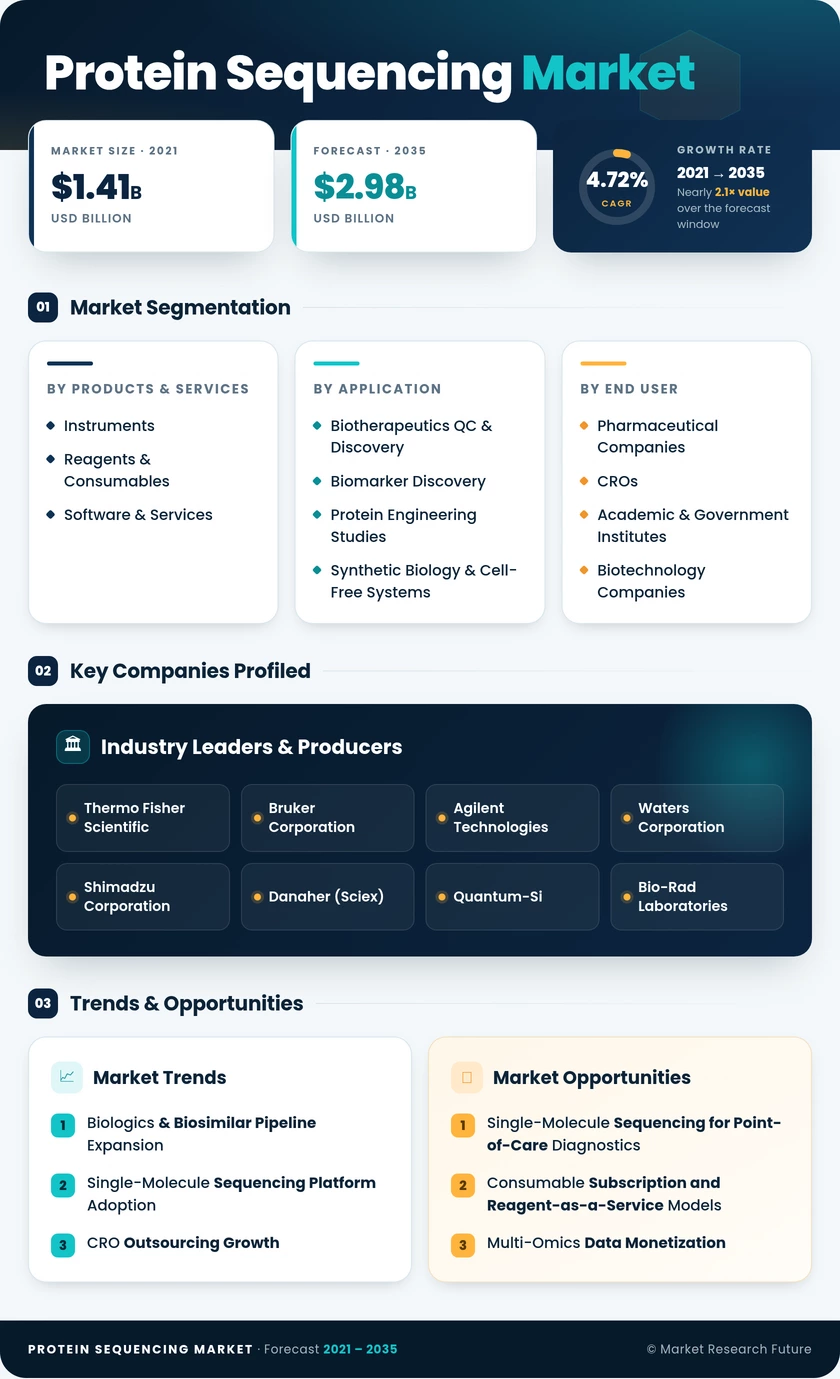

| Products & Services | Instruments; Reagents & Consumables; Software & Services | Software & Services (41% share, 2025) | Reagents & Consumables (6.9% CAGR) |

| Application | Biotherapeutics QC & Discovery; Biomarker Discovery; Protein Engineering Studies; Synthetic Biology & Cell-Free Systems | Biotherapeutics QC & Discovery (39% share, 2025) | Synthetic Biology & Cell-Free Systems (13.1% CAGR) |

| End User | Pharmaceutical Companies; CROs; Academic & Government Institutes; Biotechnology Companies | Pharmaceutical Companies (57% share, 2025) | CROs (9.2% CAGR) |

| Geography | North America; Europe; Asia-Pacific; South America; Middle East & Africa | North America (46% share, 2025) | Asia-Pacific (9.4% CAGR) |

Market Segmentation Overview

By Products & Services

| Sub-Segment | Key Trend |

| Instruments | Platform refresh toward single-molecule and high-resolution mass spectrometry systems |

| Reagents & Consumables | Recurring revenue from proprietary enzyme kits, columns, and solvent packs |

| Software & Services | Cloud migration and AI-integrated bioinformatics analytics |

The products & services dimension reflects the industry's transition from capital-intensive hardware sales toward a model that emphasizes software subscriptions and consumable annuity streams, mirroring trends seen across the broader life-science instrumentation landscape.

By Application

| Sub-Segment | Key Trend |

| Biotherapeutics Quality Control & Discovery | Mandatory sequence confirmation for biologic and biosimilar regulatory filings |

| Biomarker Discovery | Growing clinical trial demand for proteomic companion diagnostics |

| Protein Engineering Studies | Directed evolution and computational enzyme design are driving new workflows |

| Synthetic Biology & Cell-Free Systems | Rapid prototyping through cell-free expression coupled with real-time sequencing validation |

Application segmentation highlights the dominant role of biotherapeutics quality control, which creates non-discretionary demand, alongside the rapid emergence of synthetic biology workflows that require fast-turnaround sequence verification.

By End User

| Sub-Segment | Key Trend |

| Pharmaceutical Companies | Expanding in-house biologics R&D and quality-control infrastructure |

| Contract Research Organizations (CROs) | Outsourcing-driven throughput growth and per-sample pricing models |

| Academic & Government Institutes | Grant-funded proteomics core facilities upgrading aging equipment |

| Biotechnology Companies | Early-pipeline sequence analysis for novel modalities |

End-user segmentation underscores the Protein Sequencing Market's reliance on pharmaceutical companies as the primary revenue source, with CROs emerging as the growth engine driven by the broader outsourcing wave in drug development.

By Geography

| Sub-Segment | Key Trend |

| North America | NIH funding, dense pharma HQ clusters, startup innovation hubs |

| Europe | EMA biosimilar mandates, Horizon Europe research grants |

| Asia-Pacific | Government biotech initiatives in China and India, CRO hub expansion |

| South America | FAPESP-led proteomics investment in Brazil |

| Middle East & Africa | Vision 2030 life-science zones, early-stage market development |

Geographic segmentation confirms North America's leadership position, driven by institutional R&D spending, while Asia-Pacific's outsized growth trajectory reflects government-led biotech investment and the rise of India and China as major CRO hubs.