Waterproofing Membrane Market Summary

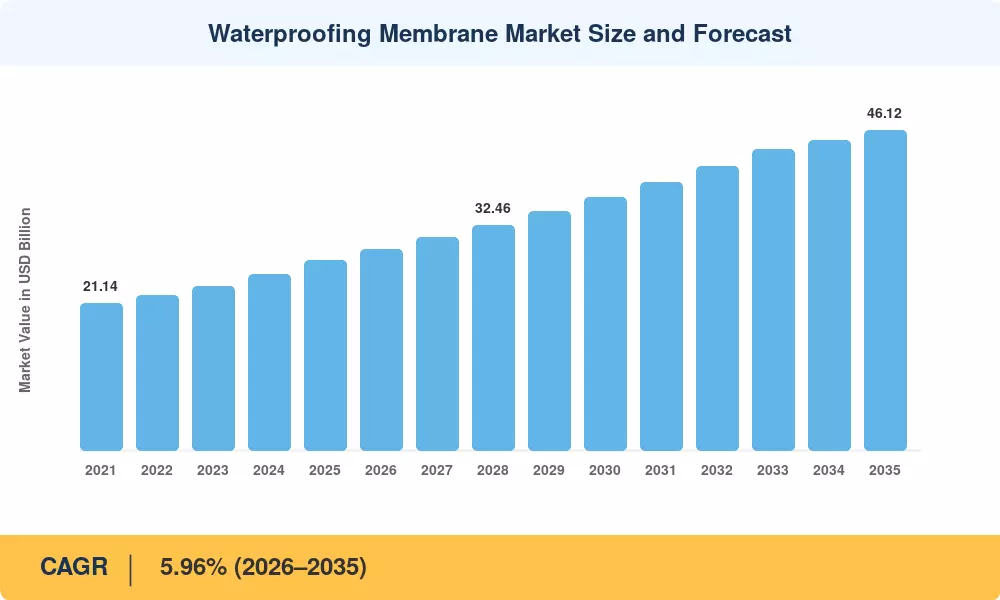

The Waterproofing Membrane Market reached an estimated USD 27.38 Billion in 2025 and is projected to climb from USD 28.91 Billion in 2026 to USD 46.12 Billion by 2035, reflecting a CAGR of 5.96% across the forecast window. This expansion is anchored in accelerating public infrastructure investment — governments worldwide committed over USD 1.2 trillion to transport and flood-mitigation projects between 2023 and 2025 — and in tightening building-envelope energy codes that now fold moisture barrier membranes into whole-building carbon performance calculations[2].

Technology is driving a generational shift within the Waterproofing Membrane Market. Legacy solvent-borne bituminous waterproofing systems are giving way to self-healing nano-composite sheets and 100%-solids liquid waterproofing systems that cure without volatile organic compound (VOC) off-gassing. The U.S. EPA's 50 g/L VOC ceiling and California's proposed 25 g/L threshold are forcing formulators to reformulate around water-based and reactive chemistries, pushing construction waterproofing solutions toward higher-performance, lower-emission profiles [3][4]. Data-center and pharmaceutical-cleanroom specifiers now treat waterproof coating materials as engineered performance components rather than commodity line items.

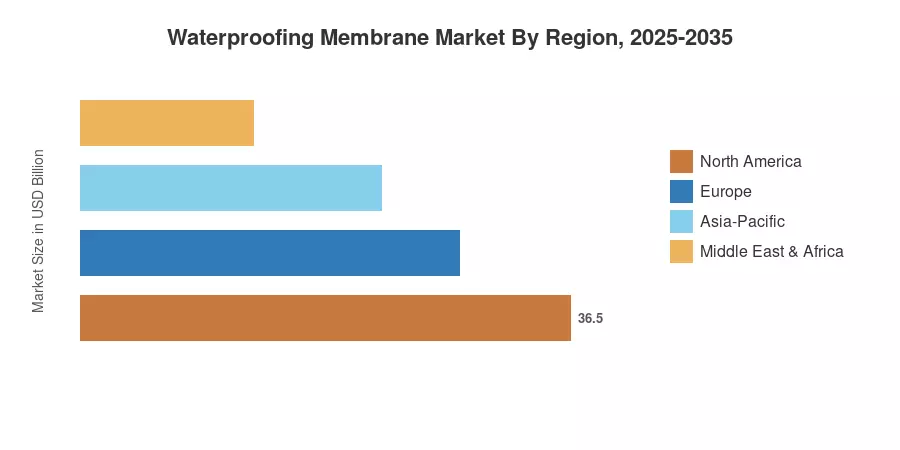

Asia-Pacific commands the largest share of the Waterproofing Membrane Market at roughly 38.9% of 2025 revenue, propelled by China's sponge-city mandates and India's urban-housing pipeline. South America is the fastest-growing region with a projected CAGR of 6.42% through 2035, driven by Brazilian metro and dam construction. Europe holds the second-largest share at approximately 24.5%, where EU renovation-wave directives continue to mandate foundation waterproofing upgrades across aging building stock

Key Report Takeaways

• By Product Type

- Cold liquid applied products captured the leading position in the Waterproofing Membrane Market in 2025, accounting for approximately 36.6% of global revenue, driven by fast-cure formulations suited to roofing waterproof membranes and retrofit projects

- Fully adhered sheet membranes are forecast to register the highest segment CAGR of 7.98% through 2035, as polymer waterproof membranes gain traction in high-wind roofing protection systems

- Hot liquid applied systems remain a critical niche for below-grade foundation waterproofing, particularly in infrastructure tunneling applications

• By End-Use Sector

- The residential sector led the Waterproofing Membrane Market with a 31.8% share in 2025, fueled by moisture barrier membranes adoption in suburban housing across North America and Asia-Pacific

- Infrastructure end-use is expected to expand at a CAGR of 6.64% through 2035 as metro, dam, and flood-control projects scale globally

• By Geography

- Asia-Pacific held the dominant revenue share of the Waterproofing Membrane Market in 2025, reflecting heavy urbanization spending in China and India

- South America is projected to be the fastest-growing region through 2035, advancing at a 6.42% CAGR as Brazilian and Argentine building waterproof materials demand accelerates

Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework triangulates primary interviews with manufacturers, distributors, and contractors against secondary trade data, customs records, and public procurement databases. Historical values (2021–2024) are validated against audited company filings; forecast values (2026–2035) apply a compound growth trajectory calibrated to macro construction spending, regulatory phase-in schedules, and raw-material cost indices.