グローバルカウンターUAS市場の概要

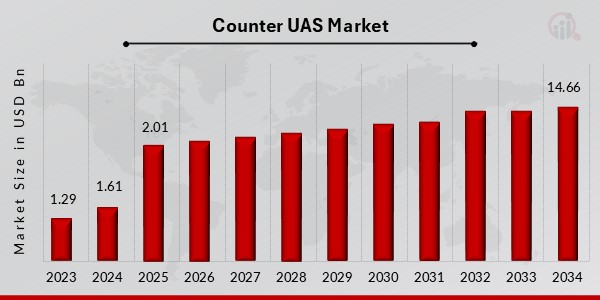

カウンターUAS市場規模は、2024年に16億1,02337582166億米ドルと評価されました。カウンターUAS市場業界は、2025年の21億米ドルから2034年までに146億6,000万米ドルに成長すると予測されており、予測期間(2025年から2034年)中に24.7%の年間複合成長率(CAGR)を示します。

出典: 二次調査、一次調査、MRFR データベースおよびアナリストレビュー

カウンター UAS システムは、許可されていない無人航空機 (UAV) やドローンを検出、追跡、無力化するように設計されています。これらのシステムは、商業、娯楽、軍事用途など、さまざまな目的でドローンの使用が増加しているため必要です。ただし、ドローンは密輸、スパイ活動、テロ攻撃などの悪意のある目的にも使用される可能性があります。

カウンター UAS システムは通常、センサー、レーダー、カメラ、その他のテクノロジーを組み合わせてドローンを検出および追跡します。これらのシステムは、ドローンを検出すると、通信信号を妨害したり、ネットやドローンキャッチャーで妨害したり、レーザーやその他の兵器で撃墜したりするなど、さまざまな方法でドローンを無力化します。ドローンの使用が増えるにつれ、カウンター UAS システムの開発は、空港、発電所、政府の建物などの重要なインフラ施設だけでなく、多くの軍や政府組織にとっても優先事項となっています。

目標は、無許可のドローンが機密領域に侵入し、危害や混乱を引き起こすことを防ぐことです。

UAS市場の動向に対抗する

テクノロジーの進歩

テクノロジーの発展により、カウンター UAS (無人航空機システム) 市場の革新が推進されており、無許可のドローンを検出、識別、無力化するための新しいソリューションが開発されています。レーダー、音響、電気光学/赤外線 (EO/IR) センサーなどの高度なセンサーにより、長距離やより困難な環境でのドローンのより効果的な検出と追跡が可能になります。人工知能AI と機械学習は、不正ドローンを迅速に特定して無力化できる、よりインテリジェントな Counter UAS システムの開発にも使用されています。これらのシステムの開発では、ドローンの不正アクセスや制御を防ぐためのサイバーセキュリティも考慮されています。

カウンター UAS システムは、包括的な防衛戦略を作成するために、レーダー、通信ネットワーク、監視システムなどの他の防衛およびセキュリティ システムとますます統合されています。これらのシステムの規制環境も急速に進化しており、さまざまな業界や用途でのドローンの使用を管理するための新しい規制が導入されています。これにより、これらの変化する規制要件を満たすことができる新しいカウンター UAS テクノロジーとソリューションの開発が推進されています。

カウンター UAS 市場セグメントの洞察

UAS Application Insights に対抗する

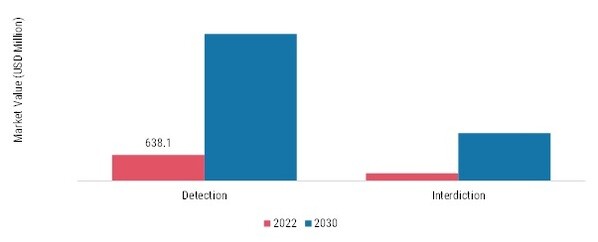

カウンターUAS市場のセグメンテーションは、アプリケーションに基づいて、(検出{レーダー、RFスキャナー、EO/IR、音響システム、複合センサー}、阻止{ジャマー、スプーフィング、レーザー、ネット})に分類されています。検出セグメントは、予測期間中に成長すると予想されます。カウンター UAS システムは、レーダー、通信ネットワーク、監視システムなどの他の防衛およびセキュリティ システムと統合され、包括的な防衛戦略を作成しています。これらのシステムの開発には、ドローンの不正アクセスや制御を防ぐためのサイバーセキュリティ対策も組み込まれています。

さらに、Counter UAS システムの規制環境は急速に変化しており、さまざまな業界や用途でのドローンの使用を管理するための新しい規制が導入されています。これにより、進化する規制要件を満たすことができる新しいカウンター UAS テクノロジーとソリューションの開発が促進されています。カウンター無人航空機システム (カウンター UAS) は、レーダー、音響、電気光学/赤外線 (EO/IR) センサーなどのさまざまなセンサーを使用して、ドローンを検出および追跡します。これらのセンサーは、長距離や都市部や悪天候などの困難な環境でもドローンを検出できます。

さらに、AI および機械学習テクノロジーは、無許可または不正なドローンを迅速に特定して無力化できる、より高度な Counter UAS システムの作成に利用されています。

図 1: 2022 年のアプリケーション別のカウンター UAS 市場シェア (%)

UAS に対抗するエンドユースの分析情報

最終用途に基づいて、カウンターUAS市場は軍事と防衛に分類されています

商業、国土安全保障。 2022 年には軍事・防衛部門が最大の市場シェアを占めました。対無人航空機システム (カウンター UAS) は、軍事および防衛部門にとって重要な注力分野となっています。これらのシステムは、軍人、重要なインフラ、その他の貴重な資産をドローンによってもたらされる潜在的な脅威から守るために特別に設計されています。軍用グレードのカウンター UAS システムには通常、レーダー、無線周波数 (RF) 検出器、ドローンを検出および追跡するカメラなどのさまざまなセンサーが組み込まれています。また、レーザー システムや電子的対抗策などのより高度な技術を統合して、無許可のドローンを無効化または無力化する可能性もあります。

さらに、軍事および防衛のカウンター UAS システムは、より大規模な指揮統制システムに統合され、ドローン関連の脅威が発生した場合の迅速な対応と調整が可能になる可能性があります。

UAS に対抗するテクノロジーに関する洞察

テクノロジーに基づいて、カウンターUAS市場はレーザーシステム、キネティックシステム、電子システムに分割されています。レーザー システム部門は 2022 年の市場シェアを占めました。対無人航空機システム (カウンター UAS) には、不正ドローンを無力化する手段としてレーザー システムがますます組み込まれています。これらのシステムは、高エネルギーレーザーを利用して、飛行中のドローンを物理的に無効化または破壊します。レーザーベースのカウンター UAS システムは通常、レーダーやカメラなどのセンサーでドローンを追跡し、レーザー ビームをターゲットに向けることによって動作します。

レーザー光線がドローンと接触すると、ドローンの電子機器が破壊されたり、ドローン自体が損傷したりして墜落する可能性があります。レーザーベースのカウンターUASシステムは、他のドローン無力化方法に比べて、より秘密の任務のための静かな操作や、爆発物と比較して巻き添え被害を引き起こす可能性が低いなど、いくつかの利点を提供します。それにもかかわらず、この分野で進行中の研究開発は、これらの制限に対処し、レーザーベースのカウンター UAS システムの有効性を高めることを目的としています。

カウンター UAS システム構成の洞察

システム構成に基づいて、カウンター UAS 市場はポータブル、車載、スタンドアロンに分類されています。ポータブルセグメントは、2022 年に最も高い市場シェアを占めました。本質的にポータブルなカウンター無人航空機システム (カウンター UAS) は、現場で無許可のドローンを検出して無力化するために迅速に導入できるように設計されています。これらのシステムは通常、迅速に組み立ておよび分解できるモジュール式コンポーネントで構成されており、さまざまな運用環境での使用に合わせて適応性と可搬性が高くなります。ポータブル カウンター UAS システムは、ドローンを識別して追跡するために、レーダー、カメラ、無線周波数 (RF) 検出器などのさまざまなセンサーを統合する場合があります。

また、妨害技術やなりすまし技術を統合して、ドローンの通信や GPS 信号を妨害する場合もあります。さらに、一部のポータブル システムには、ドローンを物理的に無力化するためのハンドヘルドまたは肩に取り付けられたレーザー システムが含まれている場合があります。ポータブル Counter UAS システムはコンパクトでモジュラー設計であるため、遠隔地や起伏の多い地形、または迅速な展開が必要な状況など、従来の Counter UAS システムが実用的ではない状況での使用に適しています。したがって、ポータブルの Counter UAS システムは通常、より大型でより包括的な Counter UAS システムと組み合わせて使用され、不正ドローンに対する多層防御を提供します。

カウンター UAS プラットフォームの洞察

プラットフォームに基づいて、カウンターUAS市場は空、陸、海軍に分割されています。航空セグメントは、2022 年に最も高い市場シェアを占めました。Counter UAS システムの航空コンポーネントには、不正ドローンを検出、追跡、無力化するための無人航空機 (UAV) の使用が含まれます。これらの UAV は遠隔操縦または自律走行が可能で、ドローンの位置を特定して追跡するためのレーダー、電気光学/赤外線 (EO/IR) センサー、またはその他のテクノロジーを含むさまざまなセンサーが装備されている場合があります。

不正なドローンが検出されると、Counter UAS UAV は、ドローンの通信や GPS 信号の妨害やスプーフィング、ドローンの物理的な傍受、ドローンを捕獲するためのネットやその他の物理的手段の展開など、さまざまな方法を使用して脅威を無力化します。 Counter UAS システムの航空コンポーネントには、広範囲にわたる脅威に迅速に展開して対応できる機能など、いくつかの利点があります。ただし、航空ベースの対向 UAS システムは気象条件や空域制限などの要因によって制限される場合があり、効果的に運用するには専門的な訓練と専門知識が必要な場合があります。

カウンター UAS の目的に関する洞察

目的に基づいて、対UAS市場は、基地保護、既存武器の補完、空港空域保護、VIP保護、および密輸対策に分類されています。基地防護セグメントは、2022 年に最高の市場シェアを占めました。基地防護は、対 UAS (無人航空機システム) 市場の重要な要素です。無許可のドローンは、軍事基地、政府の建物、その他の重要なインフラ施設に重大な安全上のリスクをもたらす可能性があります。基地保護カウンター UAS システムは通常、センサー、レーダー、カメラ、およびドローンを検出および追跡するその他のテクノロジーの組み合わせで構成されます。

これらのシステムは、通信信号を妨害したり、ネットやドローンキャッチャーで妨害したり、レーザーやその他の武器で撃墜したりするなど、さまざまな方法でドローンを無力化することができます。

UAS に対抗する地域の分析情報

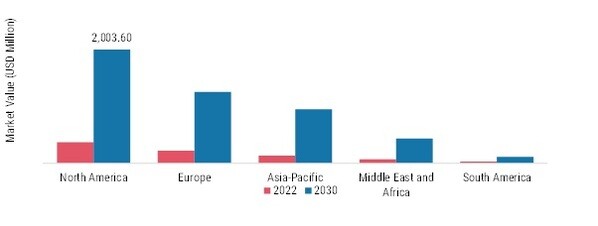

2022 年には北米が最大の市場シェアを占めました。北米は軍事支出と技術進歩でリードしており、そのため対 UAS (C-UAS) に対する需要が非常に高くなります。カナダは対抗UASの開発に投資しているが、市場は主に米国に依存している。 2021年度、国防総省(DOD)は対UASの研究開発に約4億400万ドル、C-UASの調達に約8300万ドルを支出する予定だ。

さらに、この地域は主にボーイング社、ロッキード・マーチン社、ノースロップ・グラマン社、レイセオン社などの大手メーカーの存在により、2020年の市場で最大のシェアを占めました。

2022 年にはヨーロッパが 2 番目に大きな市場シェアを占めました。ヨーロッパはカウンター UAS 技術開発の最前線にあり、多くの国がこれらのシステムの研究開発に投資しています。欧州連合はまた、ヨーロッパでのドローンの使用を管理するための規制の策定にも積極的に関与してきました。欧州委員会は、Counter UAS システムの使用を含む、ドローンの使用に関する多くのガイドラインを発表しました。

図 2: 2022 年の地域別カウンター UAS 市場シェア (%)

出典: 二次調査、一次調査、市場調査の将来データベースとアナリストのレビュー

UAS に対抗する主要な市場プレーヤーと競争力に関する洞察

カウンター UAS 市場は、多くのグローバル、地域、およびローカル ベンダーの存在によって特徴付けられます。市場は競争が激しく、すべてのプレーヤーが最大の市場シェアを獲得しようと競い合っています。激しい競争、政府の政策の頻繁な変更、航空サービス規制は市場の成長に影響を与える重要な要素です。ベンダーはコスト、製品品質、信頼性、アフターマーケット サービスに基づいて競争します。ベンダーは、競争の激しい市場環境で存在感を維持するために、コスト効率が高く高品質の対UASシステムとソリューションを商業および軍事用途に提供する必要があります。

カウンターUAS市場の主要企業には以下が含まれます。

COUNTER UAS 業界の発展

2023年2月:韓国トップの防衛企業ハンファ・エアロスペースは、米国の空域警備会社フォーテム・テクノロジーズへの投資を発表した。

2022年11月:ノースロップ・グラマンの短距離対ドローン指揮統制能力は、アリゾナ州ユマ試験場で米軍の実弾射撃試験を完了した。

カウンター UAS 市場セグメンテーション

カウンター UAS アプリケーションの見通し

カウンター UAS 最終用途の見通し

カウンター UAS テクノロジーの展望

Counter UAS システム構成の見通し

カウンターUASプラットフォームの展望

カウンター UAS の目的の見通し

カウンター UAS の地域別の見通し