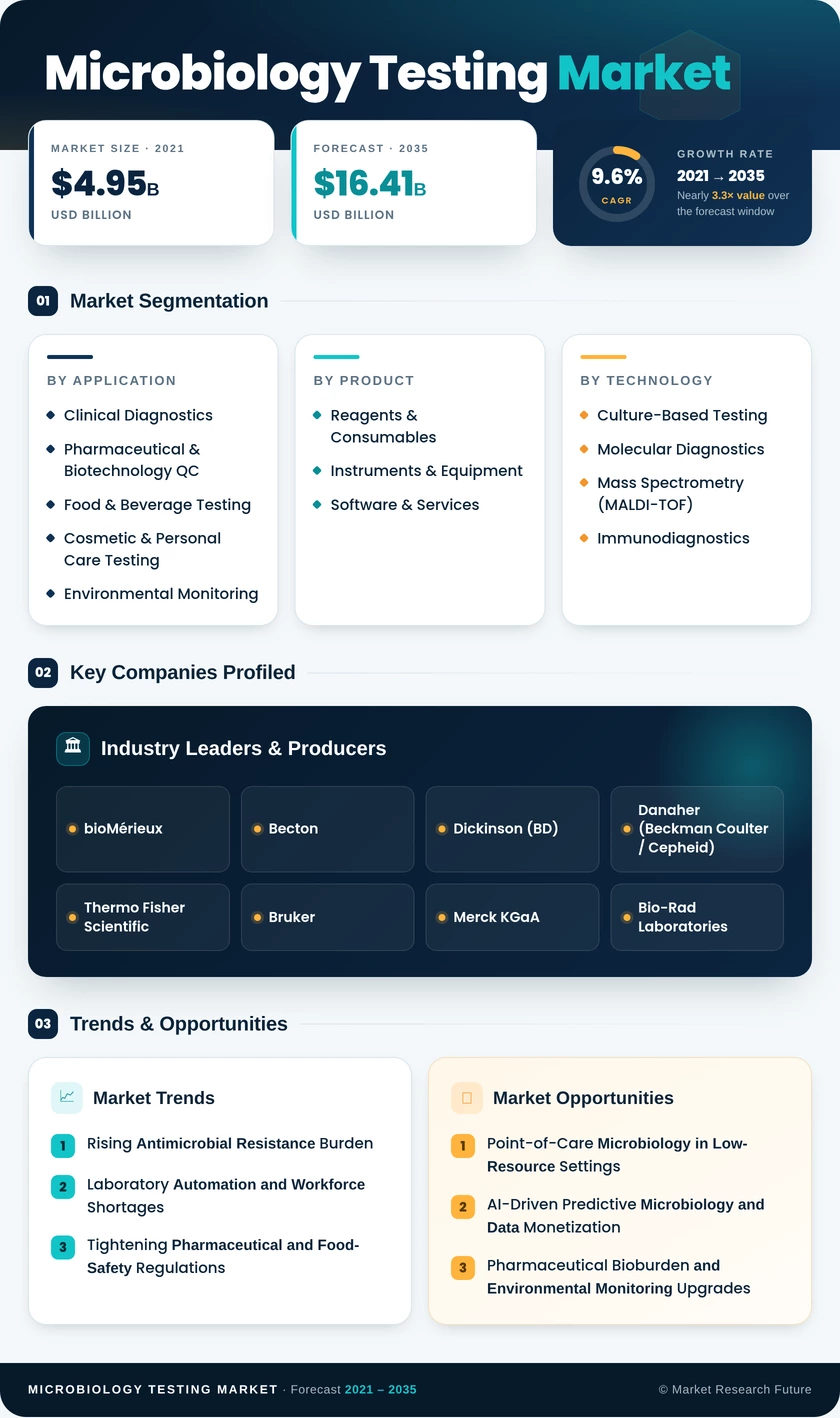

Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| By Application | Clinical Diagnostics; Pharmaceutical & Biotechnology QC; Food & Beverage Testing; Cosmetic & Personal Care Testing; Environmental Monitoring | Clinical Diagnostics | Cosmetic & Personal Care Testing |

| By Product | Reagents & Consumables; Instruments & Equipment; Software & Services | Reagents & Consumables | Instruments & Equipment |

| By Technology | Culture-Based Testing; Molecular Diagnostics; Mass Spectrometry (MALDI-TOF); Immunodiagnostics | Culture-Based Testing | Molecular Diagnostics |

| By End User | Hospitals & Diagnostic Laboratories; Pharmaceutical & Biotech Companies; Academic & Research Institutes; Food & Cosmetic Manufacturers | Hospitals & Diagnostic Laboratories | Academic & Research Institutes |

| By Region | North America; Europe; Asia-Pacific; South America; Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Application

| Sub-Segment | Key Trend |

| Clinical Diagnostics | Shift toward syndromic molecular panels for rapid sepsis and respiratory pathogen identification |

| Pharmaceutical & Biotechnology QC | EU Annex 1 mandates accelerating the adoption of rapid sterility and bioburden release methods |

| Food & Beverage Testing | FSMA Preventive Controls Rule driving pathogen-detection frequency across supply chains |

| Cosmetic & Personal Care Testing | EU Cosmetics Regulation expanding microbiological limits to new product categories |

| Environmental Monitoring | Clean-room and water-utility compliance creating steady, recurring testing demand |

Application segmentation reflects the diverse end-use environments driving microbiology testing volumes. Clinical diagnostics remains the revenue anchor, while cosmetic and personal-care testing is emerging as the highest-growth application as regulatory agencies broaden microbiological quality requirements to previously unregulated product categories.

By Product

| Sub-Segment | Key Trend |

| Reagents & Consumables | Proprietary closed-system cartridges increasing per-test revenue capture |

| Instruments & Equipment | Total laboratory automation and next-generation MALDI-TOF platforms driving capital-equipment refresh cycles |

| Software & Services | Cloud-based laboratory informatics and managed-service contracts gaining share |

Product segmentation highlights the dominance of reagents and consumables as a recurring-revenue engine. Instruments and equipment are experiencing the fastest growth as laboratories invest in automation to offset labor shortages and reduce turnaround times.

By Technology

| Sub-Segment | Key Trend |

| Culture-Based Testing | Remains the confirmatory gold standard; digital incubation imaging modernizes workflows |

| Molecular Diagnostics | Multiplex PCR and isothermal amplification platforms expanding target menus |

| Mass Spectrometry (MALDI-TOF) | AI-enhanced subspecies discrimination improves clinical utility |

| Immunodiagnostics | Lateral-flow and ELISA-based screening supporting rapid triage workflows |

Technology segmentation underscores the coexistence of legacy and advanced platforms. Culture-based testing retains the largest share due to regulatory requirements, while molecular diagnostics capture the fastest growth trajectory as syndromic panels become standard-of-care in critical settings.

By End User

| Sub-Segment | Key Trend |

| Hospitals & Diagnostic Laboratories | High-volume testing and automation adoption driving the largest share |

| Pharmaceutical & Biotech Companies | Regulatory QC mandates expanding the scope and frequency of microbial testing |

| Academic & Research Institutes | AMR research grants fueling the fastest end-user growth rate |

| Food & Cosmetic Manufacturers | Supply-chain QC compliance requirements broadening testing demand |

End-user segmentation reveals that hospitals and diagnostic laboratories generate over half of global revenue, reflecting their position as the primary operational hub for microbiology testing. Academic and research institutes are growing the fastest as government and philanthropic investments in antimicrobial-resistance research accelerate laboratory procurement.