Software as a Service Market Summary

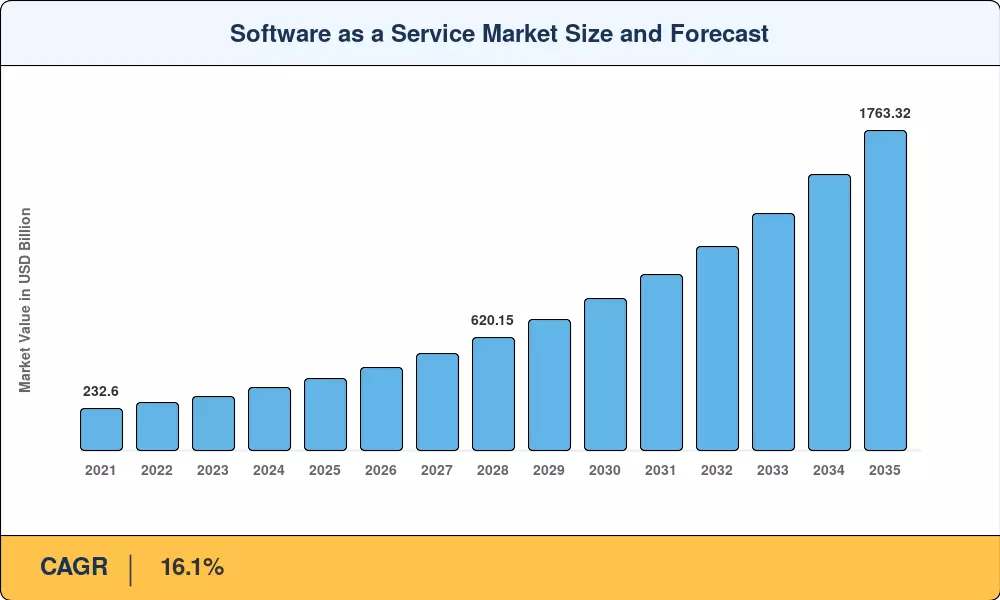

The Software as a Service Market was valued at USD 396.30 billion in 2025 and is projected to reach USD 460.08 billion in 2026, climbing to USD 1,763.32 billion by 2035 at a CAGR of 16.1% during the forecast period. Enterprise cloud migration strategies — accelerated by hybrid work mandates and AI-driven productivity demands — remain the primary catalysts. Government digital transformation spending across the EU's Digital Decade Program and the U.S. FedRAMP modernization initiative continues to channel billions into cloud-based software delivery adoption across public and private sectors[2].

Enterprise IT architecture is undergoing a generational transition. Cloud-hosted business apps that provide elastic scalability and ongoing feature updates are replacing legacy on-premises ERP, CRM, and HCM stacks. predicts that by 2027, over 85% of businesses would embrace the cloud-first concept, rerouting more than USD 680 billion in yearly IT spending toward on-demand software [3]. For mid-market buyers, the subscription software model reduces total cost of ownership by 25–40% by eliminating significant upfront license fees and shifting infrastructure management to the vendor [4].

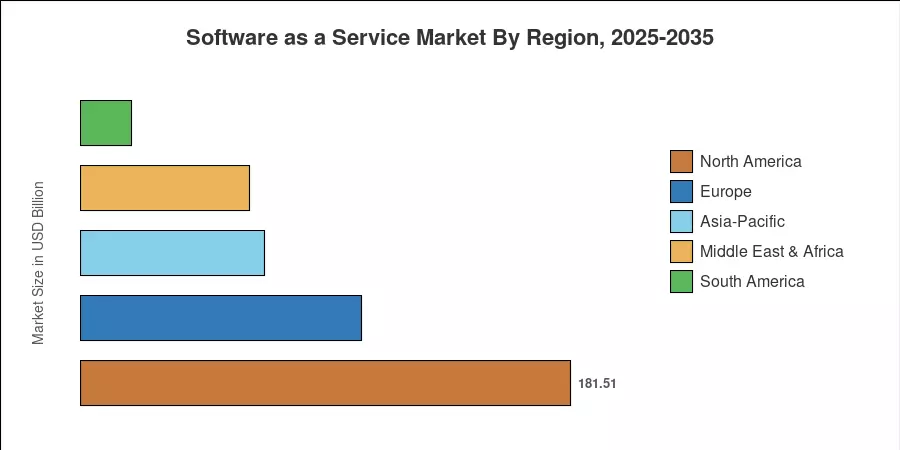

Due to the adoption of mature business SaaS application platforms and the concentrations of hyperscalers, North America held a 45.8% share of the software as a service market in 2025. With a 17.2% CAGR, Asia-Pacific is the fastest-growing area, driven by the expansion of digital-native SMEs in Southeast Asia and India. Localized cloud-based software delivery architectures are being shaped by GDPR's data sovereignty rules in Europe, which has the second-largest share (26.3%) [5]. AI-native SaaS, vertical-specific platforms, and consumption-based economics will define the next ten years.

Key Report Takeaways

• By Deployment Model

- Public cloud accounted for approximately 83% of the Software as a Service Market in 2025, reflecting enterprise preference for vendor-managed infrastructure.

- Hybrid cloud deployment is expanding at a 20.1% CAGR through 2035, driven by regulated industries requiring on-demand software solutions with data residency controls.

• By Enterprise Size

- Large enterprises represented 62.5% of the Software as a Service Market share in 2025, anchored by multi-suite platform consolidation.

• By Application

- Security and compliance SaaS application platforms are advancing at a 22.2% CAGR, the fastest among application categories.

- Pricing Model

- The subscription software model maintained a 63% revenue share in 2025, though usage-based pricing is growing at a 25.7% CAGR.

• By Region

- North America led the Software as a Service Market at 45.8% share in 2025.

- Asia-Pacific is projected to grow at a 17.2% CAGR through 2035, representing the fastest regional expansion for cloud-hosted business apps.

- Europe accounted for USD 104.23 billion in 2025 Software as a Service Market revenue.

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue modeling from vendor financial disclosures, top-down TAM validation against benchmarks, and primary interviews with 220+ enterprise IT procurement leaders across 14 countries. Historical figures reflect audited results; forecast values apply a constant CAGR of 16.1% from 2026 through 2035[6].