Energy Storage Market Summary

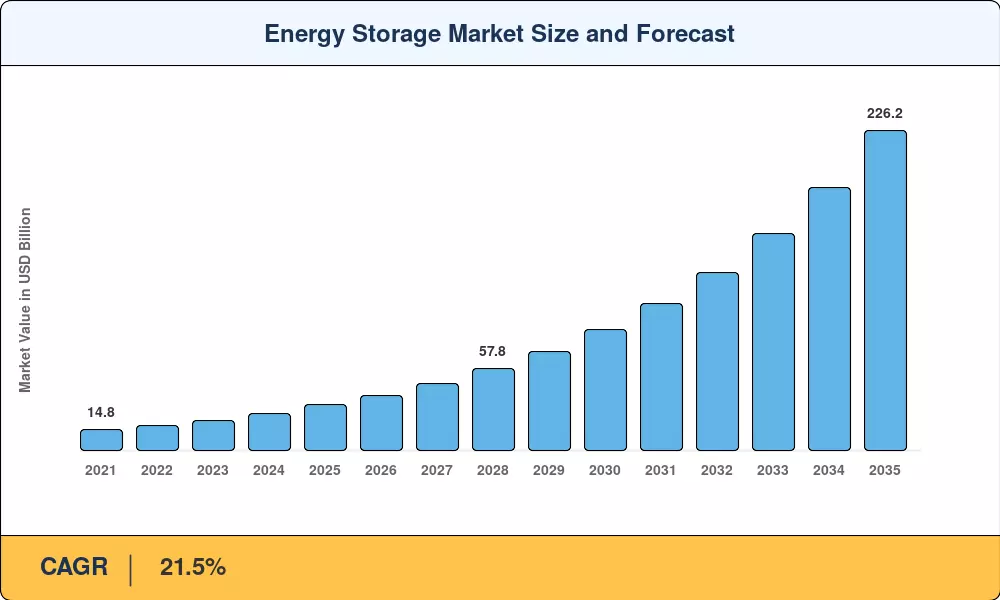

The Energy Storage Market reached an estimated USD 32.4 billion in 2025 and is projected to grow from USD 39.2 billion in 2026 to USD 226.2 billion by 2035, registering a CAGR of 21.5% over the forecast period. This acceleration stems directly from two structural catalysts: the U.S. Inflation Reduction Act's standalone storage investment tax credit — which unlocked roughly USD 7.5 billion in project financing within its first eighteen months — and China's 14th Five-Year Plan mandates requiring provinces to pair at least 10% of new renewable capacity with multi-hour storage [1][2]. Together, these policies have shifted storage economics from a cost-of-reliability calculation to a revenue-generating asset class.

The technology landscape is undergoing a decisive transformation. Lithium-iron-phosphate (LFP) cells have displaced nickel-manganese-cobalt chemistries in stationary applications, driving pack-level costs below USD 120/kWh by late 2024 [3]. Utilities across the U.S. and Europe are retiring natural-gas peaker plants and replacing them with four-to-six-hour battery systems that stack arbitrage revenue with ancillary service payments. Concurrently, hydrogen-based long-duration storage is attracting pilot-scale investment from governments betting on seasonal balancing needs beyond what batteries can economically address.

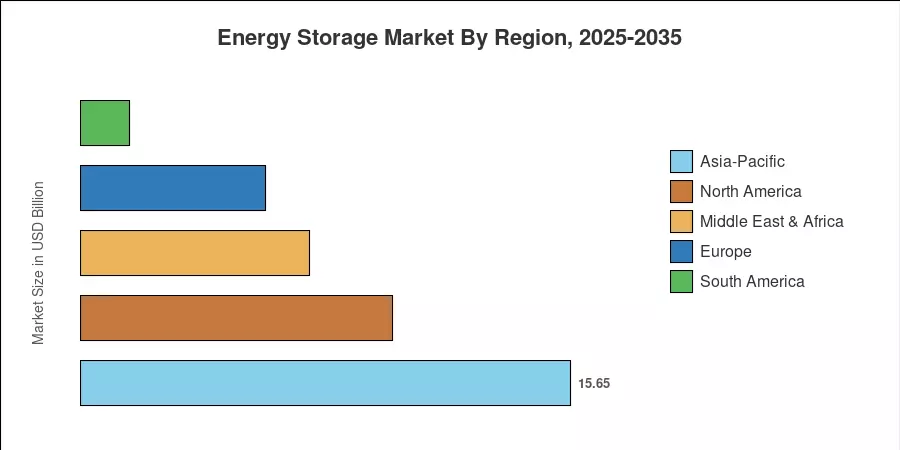

Asia-Pacific dominates the Energy Storage Market with approximately 48.3% of installed capacity, anchored by China's aggressive deployment mandates and domestic cell manufacturing cost advantages. North America is the fastest-growing region at a projected CAGR of 30.8%, propelled by federal incentives layered on top of state-level procurement targets in California, New York, and Texas. Europe holds the second-largest share at 18.2%, where the REPowerEU plan and grid-bottleneck challenges in Germany and the Nordics are accelerating storage adoption. The decade ahead promises a structural expansion cycle unlike anything the power sector has experienced since the build-out of combined-cycle gas turbines in the 1990s.

Key Report Takeaways

• By Technology

- Batteries commanded a 57.6% share of the Energy Storage Market in 2025, driven by LFP cell cost reductions and utility-scale procurement.

- Hydrogen-based storage is forecast to register the fastest segment CAGR of 35.4% through 2035, reflecting growing interest in seasonal and long-duration discharge profiles.

• By Application

- Grid-scale utility projects accounted for 75.4% of the Energy Storage Market in 2025, as transmission operators prioritize storage for congestion management and frequency regulation.

- EV-charging infrastructure storage is projected to grow at a 27.4% CAGR through 2035, propelled by corridor electrification programs.

• By Region

- Asia-Pacific captured 48.3% of installed capacity in 2025, with China alone responsible for more than half of regional deployments.

- North America leads regional growth at a 30.8% CAGR, underpinned by IRA incentives and state-level storage mandates.

Energy Storage Market Size and Forecast (2021–2035)

All figures below derive from Market Research Future's proprietary sizing framework, which triangulates bottom-up project-pipeline data, top-down industry shipment records, and validated policy-impact models across 42 countries. Historical values (2021–2024) are reconciled against publicly reported deployments; forecast values (2026–2035) assume currently enacted policies only, with no speculative legislation included.

.webp?v=1784802854)